IADS Exclusive Articles

IADS Exclusive – Macy’s: from the world’s largest store to a leaner future

IADS Exclusive – Macy’s: from the world’s largest store to a leaner future

Macy’s story is that of an American institution. From a single store in 1858 to a nationwide banner, it became not only a retail powerhouse but a cultural symbol woven into American life. Unique in terms of national coverage and multi-banner operations, the scale that once secured its dominance is now put to the test.

In FY2024, Macy’s Inc. spanned 680 stores, including Macy’s, Macy’s Backstage off-price outlets, Market by Macy’s small-format stores, but also Bloomingdale’s, Bloomingdale’s The Outlet, Bloomie’s (Bloomingdale’s small-format stores), its international stores in Dubai (UAE) and Kuwait under license, and beauty specialist Bluemercury. FY2024 closed with net sales of $22.293 billion (down 3.5% YoY). The company reported a 38.4% gross margin (flat YoY). Digital sales accounted for 33% of net sales (unchanged from 2022), indicating a stabilised omnichannel mix after pandemic-era gains.

Despite a glorious past, today’s Macy’s financial picture seems gloomy for a department store as tightly intertwined in the country’s commercial and cultural landscape as it is. Macy’s mirrors the evolution of retail itself in the 20th century: a story of pioneering and relentless innovation. The fight for relevance is the question it needs to address to fully belong in the 21st century.

The making of an American star

From 14th Street to Herald Square

In 1843, Rowland Hussey Macy opened several dry goods stores in Massachusetts. All failed. Learning from its mistakes, he opened R.H. Macy & Company on NYC’s 14th Street and Sixth Avenue in 1858. He adorned it with a star, which has remained Macy’s logo to this day. Innovative from its inception, the store changed the retail industry. It was the first to institute the one-price system, advertise its prices in newspapers, and promote a woman to an executive position. Margaret Getchell started as a cashier and rose to become a leader in the company. She developed many ideas, including using illuminated window displays to attract customers. Macy’s also pioneered the use of an in-store Santa Claus as early as 1861, embedding retail into cultural rituals.

Macy died in 1877. The company remained in the family until it was acquired in 1895 by Isidor and Nathan Straus, who had previously held a license to sell china at Macy’s. The decisive step came in 1902, when the store relocated to Herald Square. Initially a single building, the store expanded through new construction, eventually occupying almost the entire block bounded by Seventh Avenue, Broadway, 34th Street and 35th Street, creating what was then the world’s largest store. The store seemed so far away from its original ground that the company had to offer a steam wagonette service to transport customers from 14th Street to 34th Street. Macy’s became a publicly listed company in 1922. Two years later, Macy’s inaugurated the Thanksgiving Day Parade, which soon became a cultural event and a form of brand equity independent of its stores.

Macy’s goes national: growth and the making of a middle-class brand

The company opened their second location in the Bronx in 1941. The interwar period was marked by expansion beyond Manhattan, acquiring local department store chains across the country, including Lasalle & Koch (Toledo), Davison-Paxon-Stokes (Atlanta) and L. Bamberger & Co. (Newark). Post-World War II, acquisitions resumed with O’Connor Moffat & Company (San Francisco) and John Taylor Dry Goods Co. (Kansas City).

Then, Macy’s opened mall branches in Miami’s suburbs, Houston, New Orleans, Dallas, Atlanta, the Midwest, New Jersey, Philadelphia and Baltimore. From 1976 onwards, Macy’s cultural pull also included the 4th of July Fireworks over NYC’s East River and Hudson River.

Macy’s became an authority in bringing accessible style to the growing middle-class consumers, positioning itself between discount chains and luxury stores. It was neither elitist nor mass-market, but rather a “mass premium” brand long before the term existed. Soon enough, the flagship store functioned as both a commercial hub and a symbolic space for aspirational middle-class consumption.

From bankruptcy to a coast-to-coast powerhouse

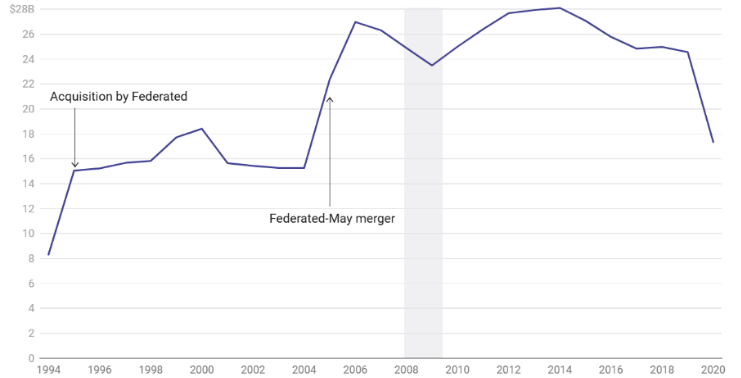

By the 1970s and 1980s, Macy’s continued acquiring regional department stores. However, aggressive expansion financed by debt led to instability, a pattern Saks Global is currently experiencing. In 1992, Macy’s filed for Chapter 11 bankruptcy, underscoring the fragility of even the most iconic retail institutions and challenging the ‘too big to fail’ economic assumption. The company emerged from bankruptcy in 1994, merging with Federated Department Stores, the owner of Bloomingdale’s, among other banners. This merger created the largest department store group in the U.S., providing Macy’s with capital, management expertise, and scale. In 1995, the group operated 355 department stores across 35 states, achieving $8.29 billion in sales.

Federated Department Stores’ strategy culminated in the $11 billion acquisition of May Department Stores in 2005 and the conversion of approximately 400 stores to the Macy’s nameplate in 2006. Indeed, Federated rebranded most of its regional banners, such as Marshall Field’s, under the Macy’s name. This controversial move erased long-standing local identities in favour of the Macy’s brand, totalling 853 stores, creating a truly coast-to-coast flag and a universal name recognition. The consolidation positioned the department store as the anchor in hundreds of malls nationwide. In practical terms, that nationalisation gave the company a distribution canvas that neither luxury-led peers nor remaining mid-market rivals match to this day.

Federated Department Stores re-named itself Macy’s, Inc. in 2007. Standing out among other U.S. department stores, Macy’s diversified its portfolio across price tiers and categories, including Bloomingdale’s in the upscale fashion segment and the 2015 acquisition of beauty retailer Bluemercury.

Reinventing the store: Macy’s between culture, localisation, and experience

When a store becomes a stage: Macy’s as a cultural institution

Macy’s emerged as a reference in American and global retail by pairing scale with cultural brand-building. The company treated the department store as a public theatre and then institutionalised spectacle through the Macy’s Thanksgiving Day Parade. The first Disney Mickey Mouse balloon entered the parade in 1934, paving the way for subsequent cultural collaborations with Sonic the Hedgehog, Barney the Dinosaur, Snoopy, the Pink Panther, and brands like M&M’s. The parade became known nationwide after WWII, as it was heavily featured in the 1947 film Miracle on 34th Street, which included footage of the 1946 festivities.

Also, Macy’s began the annual Independence Day show with the U.S. Bicentennial in 1976, the start of the modern Macy’s 4th of July Fireworks tradition. That event, broadcast nationally on WPIX and later by NBC (which also broadcasts the Macy’s Thanksgiving Day Parade), solidified the company as a household name and transformed a retail banner into an annual cultural tradition, reinforcing Macy’s “owned media” advantage at a national scale. This blend of retail and ritual helps differentiate Macy’s from peers whose brands are influential in their cities but may lack a countrywide cultural amplifier.

My Macy’s: central power, local touch

My Macy’s strategy was launched in 2008 under the leadership of CEO Terry Lundgren as a much-needed localisation programme, aiming to bring a more personalised flair to stores by moving day-to-day assortment and presentation decisions closer to the store. Macy’s expanded it nationwide in 2009 with a new structure of regional merchants and planners who tailored buys, sizes and presentations to local tastes, creating 1,200 new roles. Parallel to that, Macy’s consolidated regional divisions into a single national organisation for core functions (buying, marketing, finance, and HR) to reduce duplication, increase efficiency, and streamline decision-making.

The operating model consisted of 69 districts that could adjust roughly 10-15% of a store’s inventory mix to local demand, with national categories and seasonal statements still determined by central buying. Also, to make My Macy’s work, they automated customer tracking and segmentation, allowing for a clearer view of the consumer. Early results were positive as most of the top-performing markets in 2009 were My Macy’s districts.

By late 2011, Macy’s introduced “My Macy’s 2.0”, additional targeted, cross-functional initiatives designed to sharpen local relevance and tie it more tightly to the company’s emerging omnichannel model. Macy’s pushed more decision-making to district teams to fine-tune “by store,” not just by region. My Macy’s 2.0 was deployed alongside a ship-from-store/BOPIS scale-up strategy, with localised inventory serving digital orders nationwide. Tablets, tap-to-pay pilots and QR codes were rolled out to improve discovery and conversion. Finally, the “MAGIC Selling” training (Meet-Ask-Give-Inspire-Celebrate) was expanded to raise conversion and NPS.

My Macy’s improved sell-through and relevance while protecting scale. However, it fell short due to uneven, complex execution. Building and maintaining district-level merchant teams added organisational complexity, with outcomes varying by market and leadership depth. Localisation was necessary but insufficient to deliver the digital growth achieved by other platforms. Macy’s digital mix eventually stabilised around one-third of sales in the 2020s, requiring additional strategies beyond localisation.

That said, as a case of “localisation at scale,” My Macy’s was a smart hybrid of central scale and local empowerment. Its limits became apparent later: it could raise relevance, but it couldn’t fully overcome macro headwinds (mall traffic erosion, off-price, and online pressure) without broader reinvention in experience, merchandising authority, and digital. In Macy’s transformation arc, My Macy’s appears as the operational foundation that allowed subsequent strategies such as off-mall small formats, marketplace and fleet upgrades.

Moreover, My Macy’s illustrates a typical pattern: companies pursue centralisation and scale, then decentralisation in the name of localisation and personalisation, as neither strategy is 100% satisfactory. For example, Walmart, a champion of centralisation and standardisation, emphasised local tailoring via “Store of the Community” in 2001 with assortments adapted to local demographics, moving from a one-size-fits-all playbook toward more local customisation.

Turning stores into stories

In 2018, as retail was becoming less transactional, Macy’s invested in experiences to capture younger consumers, establishing a pop-up enterprise, dubbed The Market @ Macy’s, designed to emphasise in-store discovery of emerging brands and niche products. The ten pop-up stores were designed to offer customers a rotating selection of apparel, accessories, beauty, entertainment, experiences, decoration, stationery, technology, and gifts. The retail-as-a-service concept was described as a solution for brands looking to break into brick-and-mortar retail. Unlike traditional concessions, Macy’s staff ran the pop-ups. Offering more flexible lease terms, brands were paying a fixed fee but pocketing all sales. Ultimately, Macy’s evaluated sales and traffic. The duration was flexible, although a one-month minimum commitment was required.

Later in 2018, Macy’s acquired Story, a quirky New York City retail store that has partnered with big and small retailers and brands. Story defined itself as a storytelling retail model, adopting a magazine’s perspective, evolving like a gallery, and selling items like a store. Macy’s even hired Story founder Rachel Shechtman as brand experience officer. Finally, that same year, Macy’s partnered with b8ta, a company providing the technology engine to enhance and scale The Market @ Macy’s. With b8ta’s software platform and business model, product makers could go from solely selling online to launching their products with Macy’s in a few clicks. However, execution was uneven, and Macy’s struggled to balance its vast legacy footprint with the agility needed for such formats. When COVID hit and Macy’s closed stores in March 2020, the pop-up programme was effectively discontinued and did not return thereafter.

In transition: the state of Macy’s today

Why Macy’s lost its shine

In 2015, roughly 10 years after its massive expansion that led to a network of 853 stores, Macy’s told investors it would close 35 to 40 underperforming stores in 2016. In the meantime, analysts expressed confidence that Amazon would overtake Macy’s in apparel sales (even though Macy’s entered e-commerce early). In the years that followed, as Amazon grew its fashion business, Macy’s turnover decreased.

However, Amazon is not solely responsible for Macy’s downfall. The mid-century department store mall era’s promise to combine the best of the fashion world with the best of the discount world hardly works in the 21st century. As a mid-tier banner, Macy’s business was eroded by low-price retailers (as early as 1962 with the start of mass-market retailers such as Target) and discounters serving a shrinking middle class. By comparison, in 2006, Macy’s operated 853 department stores and a website, reaching $27 billion in sales, while Target operated nearly 1,500 stores and a website, notching $59.5 billion in sales.

In parallel, the department stores’ love story with malls came to an end. Macy’s, as a suburban mall anchor nationwide, didn’t react quickly enough as suburbanites grew pessimistic and anxious about the future, increasingly buying cheaper products at off-price stores outside traditional malls. Malls and their department store anchors were stuck together, but were no longer hangout locations for kids and teens. Meanwhile, speciality retailers such as Sephora in beauty or Best Buy in electronics took market share from department stores. In turn, unable to compete with these speciality retailers, Macy’s (and others) closed or reduced store sections, filling them only with apparel (in free fall anyway) and making the stores less and less relevant and attractive. Finally, as the U.S. middle class shrinks, the mid-price market is disappearing, leading Macy’s to compete with off-price retailers.

From Polaris to A Bold New Chapter: Macy’s strategic reset

Learning from the My Macy’s and Market @ Macy’s initiatives, the company launched the three-year turnaround Polaris strategy, announced in February 2020 by CEO Jeff Gennette. Meant to stabilise profitability and position the company for growth, it was primarily built around:

- Optimising the fleet by closing roughly 125 lower-tier-mall stores while giving “growth treatment” to 100 stores and testing off-mall small formats, Market by Macy’s.

- Accelerating digital/omnichannel (ship-from-store, BOPIS, marketplace).

- Simplifying the organisation with a net 9% reduction in its corporate function headcount (approximately 2,000 positions) and one corporate HQ.

In practice, parts of Polaris worked. Macy’s built a balanced omnichannel mix, resulting in digital stabilising at ~33% of net sales by FY2024, while the marketplace expanded. However, some elements of the strategy stalled: the original 125-store closure cadence was disrupted by the pandemic and later re-scoped. Several pre-Polaris experiments (The Market @ Macy’s and the Story shop-in-shop) were wound down and not scaled post-2020.

Announced four years after the Polaris strategy, A Bold New Chapter plan, led by new CEO Tony Spring, builds on and accelerates Macy’s Polaris portfolio reset. The plan includes closing ~150 underproductive Macy’s locations by 2026 and investing in ~350 “go-forward” stores via remodels, service and presentation upgrades, while scaling small-format/off-mall concepts. In January 2025, Macy’s confirmed the first 66 closures as an initial wave, consistent with the multi-year target. Also part of A Bold New Chapter, Macy’s created the “First 50” cohort, the first wave of upgraded stores. 2024 third-quarter results highlighted that these locations delivered their third consecutive quarter of comparable sales growth, up 1.9%. However, Macy’s First 50 locations, Bloomingdale’s and Bluemercury’s posted growth is more or less offset by softness in non-first-50 Macy’s doors. In the coming semesters, the plan’s credibility will rely on the pace of closures and the performance of upgraded doors. Overall, the plan acknowledges and builds on Macy’s reality: its strongest stores still outperform, but the weakest ones drag down the brand.

Macy’s next moves

So far, structural headwinds have outpaced wins. As a result, Macy’s has many challenges ahead to secure its future as a mid-tier department store:

- Rebuild its fashion authority despite the sector squeeze. With the U.S. mid-market pressured by off-price, fast fashion, and platforms, Macy’s needs clearer category leadership (especially in women’s categories, its most prominent family) and a sharper brand image, less reliance on promotions, and more on curation and experience so that the remaining fleet feels “worth the trip.” This is still a question mark, as previous attempts have failed.

- Grow e-commerce beyond 33% of the business without eroding contribution margins.

- Finish the store fleet reset at pace and with proof, as the strategy only delivers if the upgraded doors consistently outperform the fleet.

- While Macy’s credit card is an additional revenue stream, it fell to $537m in FY2024 as card income is sensitive to credit cycles.

- In 2019, “retail prophet” Doug Stephens defined the company’s struggle: “Macy’s has two things, space and audience, and they’re not leveraging that space and that audience to find new ways of making money beyond selling apparel and linens, ways to monetise experiences within that space that are richer for the consumer.” It’s not entirely true anymore, as Macy’s has built Macy’s Media Network to monetise Macy’s audience and data through brand advertising on owned and partner surfaces. This additional source of revenue generated $176 million in FY2024 (+13.5% YoY).

- Accelerate Bloomingdale’s and Bluemercury growth, the best way to de-risk Macy’s overexposure to the mid-tier.

- Keep control of the real-estate narrative. Macy’s must show that its own plan has more value than aggressive sale-leasebacks would, as suggested by activist investor pressure from Arkhouse Management and Brigade Capital, which launched an unsolicited acquisition bid in 2023 to take the company private. They would have used every means to extract cash from stores while keeping them open under leases. They likely would have done a portfolio-by-portfolio review, selling some stores and leasing them back, placing secured debt on flagship or high-quality sites and pursuing mixed-use redevelopments on under-utilised parcels. Macy’s board ended talks in July 2024, saying the proposal lacked value and financing certainty.

Macy’s today is a scaled mass-premium platform with owned media assets, a coast-to-coast store network and diversified banners that many U.S. peers cannot replicate. The fleet reset, store closures and investments are designed to concentrate capital and talent where the unit economics justify it. The primary risks remain the mid-tier squeeze from off-price, fast fashion and e-commerce platforms, and the credit income risk. Conversely, the 33% digital mix, the traction at First 50 locations and the ongoing strength at Bloomingdale’s and Bluemercury point to levers Macy’s can scale as the transformation progresses.

Macy’s future relies on turning a smaller, better fleet and a balanced profit mix, with merchandise from its various banners, credit and retail media revenue, into sustained growth and margin, while advancing the digital business to make the company less exposed to the structural headwinds of the legacy mall model. The company itself sets the targets: the next 6-18 months are about proving them in the numbers. A question remains: what to do with Macy’s most significant symbol —the Herald Square flagship store, which increasingly seems irrelevant at the light of today’s consumer habits.

Credits: IADS (Christine Montard)

IADS Exclusive: Department stores Holiday windows 2025

IADS Exclusive: Department stores Holiday windows 2025

IADS presents the consolidated 2025 Holiday Window Displays from around the world in this year’s Holiday Window Report. Discover how IADS members and other leading department stores are welcoming the new festive season through their imaginative, artistic, and forward-looking visual interpretations.

CLICK HERE TO SEE THE 2025 HOLIDAY WINDOWS REPORT

Credits: IADS Team

IADS Exclusive – The age of relevance

IADS Exclusive – The age of relevance

It is almost inevitable that the human population will decline. Birth rates are falling at much higher rates than initially projected, across rich, poor, and middle-income countries alike1. A reduction in childhood mortality, better contraception and healthcare, as well as women’s increasing financial independence in many parts of the world are among the reasons contributing to this phenomenon. A decrease in the world’s population, unseen since the Black Death during the 14th century2, is now an imminent reality. Naturally, this leads to the discussion of ideas that once seemed farfetched, with world leaders Xi Jinping and Vladimir Putin caught discussing immortality through organ transplants, the notion that an aged population will lead to fewer wars, and broad implications for the labour force especially with the hurtling pace of technological developments including artificial intelligence.

With the peak of human population expected to be in 20843, a much closer reality is that an increasingly larger proportion of the human population will be elderly. As healthcare improves, people will be “older for longer”, thereby changing the demographic structure of the human population. The average department store consumer is middle-aged; however, the narrative surrounding serving these consumers has often skirted around or relied on subverting age stereotypes. The age-old (pun-intended) question has been: how do we serve elderly customers without calling them old? However, some retailers and brands are in the process of rebranding being old and leaning into combatting ageism by beginning mainstream discussions. With generations typically increasing their spending power as they age, currently concentrated in Gen X and beyond, department stores have a unique advantage in addressing consumption for ageing populations.

Ageism, beauty standards and the cost of exclusion

The stigma of being labelled ‘old’ reflects deeply rooted attitudes in which ageing is equated with diminished worth, relevance and incompetence. Ageism manifests across various domains, from workplace discrimination, dismissal of health symptoms, to social interactions patronising or ignoring older adults. In the retail industry, this presents as the exclusion of workers over forty, glorifying ‘youthful’ energy and excluding age diversity in inclusivity strategies4 . Ageist attitudes are particularly pronounced on gender lines, creating an imbalance where women encounter these much earlier and more markedly than men, compounding the effects of sexism. Women in their forties and fifties are perceived as being ‘old’ or having past their reproductive or conventional beauty standards while men of this age are often seen as still being in their prime.

The beauty industry offers the clearest illustration, where anti‑ageing has long been a foundational theme, with products marketed to women starting as early as their twenties, and sometimes even before. According to the latest Vogue Business beauty standards survey, ageing is a primary beauty concern according to 97% of respondents. Recently, the beauty industry has seen the onset of a ‘pro-ageing’ movement which ‘advocates for self-care and wellness at every stage in life’. Several beauty brands have transitioned from using words such as ‘anti-ageing’ to ‘rejuvenation’, ‘revitalisation’ and ‘ageless’, in advertising, promoting linguistic inclusivity while still idealising youth.

On one hand, beauty brands are rewording narratives to performatively tackle these pervasive beauty standards while on the other hand, increasingly medicalising beauty products to enhance claims of ageing reversal—La Prairie Pure Gold Revitalising Essence claims ‘maximum cellular renewal for skin with visible signs of ageing especially those linked with hormonal disequilibrium’. Beauty products are increasingly medicalised to create a stronger backing for products claiming to reverse natural processes such as ageing. This follows the larger trend of increased consumption of medicalised beauty products and procedures including the rise of Ozempic and other GLP-1 agonist drugs.

In recent years, the inclusion of older supermodels and actresses in advertising and fashion campaigns has often functioned as a form of token representation rather than genuine inclusivity. While figures like Maye Musk, Isabella Rossellini, and Helen Mirren are celebrated for defying age norms, their visibility tends to reinforce selective ideals of “ageing gracefully” rather than embracing age diversity in all its forms. Pamela Anderson’s makeup-less appearance at Paris Fashion Week and El Palacio de Hierro’s campaign featuring Carmen Dell’Orifice are examples of inclusivity without challenging the underlying narrative yet. This controlled visibility serves commercial motives, targeting older consumers with spending power without truly challenging entrenched ageist beauty standards.

Beauty standards and hyper perfectionism are reaching unprecedented levels in the age of AI. AI-generated content is known to lack diversity and introduce bias as a result of training data; this is further demonstrated by the exclusion and replacement of elderly models and consumers by generated versions. Diesel’s usage of AI-generated elderly models that are conspicuously muscular shows the distortion of beauty standards that is fuelling the engagement of all generations with ageing trends in differing manners. Ageist ideals in society are reflected in the retail industry, not just in beauty but in fashion, luxury and other sectors.

Altogether, such practices highlight the persistent commodification of inclusivity in the beauty and fashion industries, where ageing becomes a marketable narrative rather than authentic inclusion. The normalisation of ageing is the first step to addressing the biggest consumer group of the future.

The rebranding of ageing: Longevity and nostalgia

Longevity’s emergence as a defining wellness paradigm in 2025 reframes ageing from an unavoidable decline into an optimisation programme. A significant share of younger consumers is prioritising healthy ageing by adopting preventive practices such as cellular supplements, wearables, and epigenetic testing to extend health span rather than merely lifespan. Within this context, Khloé Kardashian’s KHLOUD protein popcorn exemplifies youth-oriented and health‑conscious positioning that capitalises on recent widespread appeal for accessible nutrition. Concurrently, the mainstreaming of menopause care, accelerated by social media communities and emergent brands such as Respin serving women in their forties and fifties, exposes a historically underserved category for life-stage solutions in the beauty and health industry. In developing markets, younger generations’ early adoption of wellness and longevity products is reinforced by sustainability considerations, further integrating health optimisation with sustainable consumption.

Parallelly, nostalgia marketing from legacy brands such as Levi’s and Polaroid taps into younger consumers’ yearning for eras they have never experienced, reflecting deeper anxieties about uncertain futures and a desire for perceived authenticity and stability from the past. This convergence creates a unique opportunity where older adults become valuable cultural transmitters rather than obsolete demographics - their lived experiences of nostalgic eras gain currency with younger generations seeking connection to ‘simpler times’, while their embodiment of successful ageing aligns with longevity wellness aspirations.

The result is a reframing where age becomes a bridge rather than a barrier, with older consumers positioned as pioneers and cultural custodians rather than declining market segments, fundamentally reshaping retail’s approach to intergenerational marketing and product development. Rather than recasting ageing for younger consumers, embedding older adults in product, content, and experience design so that communication embodies participation, not proxy representation is key.

Department stores bridging generations

Recently, Le Bon Marché hosted a cultural exposition entitled Rock’n’Drôle curated by renowned French television presenter Antoine de Caunes. Transforming the store and windows into a comprehensive celebration of rock and roll heritage, it encompassed a selection of vintage clothes and accessories reminiscent of the genre’s golden era, limited edition souvenirs and rare concert merchandise, as well as a space dedicated entirely to music complete with jukeboxes and vinyl records in collaboration with brands such as Kiloshop and Gibson, and collaborations with artists and animators including a surprise performance by Patti Smith.

The most notable feature, however, was the Rock Motel on the second floor which had ten themed rooms, each one paying tribute to ten icons of the genre including Elvis Presley, The Beatles, David Bowie and Patti Smith among others. The experience was enhanced by sensor-driven technology that triggered contextual narration throughout different areas of each room, with commentary provided by de Caunes’ cult persona Didier L’Embrouille from the French channel Canal+.

Perhaps unintentionally but significantly, the exhibition created meaningful intergenerational connections. Grandparents and parents were observed guiding younger family members through the installations, sharing anecdotes and contextualising the cultural significance of these musical icons for younger audiences. This organic knowledge transfer, as part of a technological showcase, exemplified how curated experiences can serve as a bridge between generations, demonstrating the growing trend of cultural programming to foster deeper customer engagement. John Lewis’ Christmas advertisement for the new ‘Where Love Lives’ campaign, showcases a similar sense of connection and nostalgia, taking viewers on a journey between a father and son, transported by music back to the 1990s.

During the same period, Galeries Lafayette presented a fashion and accessories curation by Sophie Fontanel, a French fashion critic, writer and influencer. She has been an avid commentator on ageing and deciding to go grey, having released a book on this topic, and stating that ‘the real anti-wrinkle is not caring’. Her curation was displayed across the ground floor and womenswear section at Galeries Lafayette Haussmann, however at the time of visit, there was negligible customer interaction. She is featured on the cover of the fall catalogue, and the photograph and her choice of products subvert age stereotypes by owning markers such as greying hair and wrinkles, despite the ironic advertisement for La Prairie’s Revitalising Essence promising ‘eternal youth’ in the catalogue. In an interview, she also discussed the impact of filters on younger generations and how wrinkles go beyond shaping one’s face to include every experience in one’s life.

Beyond youth targeting: the intergenerational dividend

The silver generation, comprising many grandparents, frequently assumes responsibility for the care of their grandchildren. This demographic generally enjoys financial stability and tends to indulge their grandchildren, prioritising expenditures on them over personal spending (in France, it is estimated that assets exceeding EUR 9 trillion will be transferred to the next generation by 2040 as the baby boomer cohort ages). Grandparents shop for their grandchildren and look for entertaining activities when they look after them, representing business opportunities for retailers. Department stores, in particular, should reflect on how shared experiences between grandparents and grandchildren might cultivate enduring customer relationships among younger generations. Furthermore, a fair part of Generation X remains financially prosperous and spends a significant portion of their resources on personal consumption, which is another business opportunity. Despite this, most visible marketing efforts among retailers usually focus on attracting younger generations. It is notable that two department stores simultaneously introduced substantial campaigns addressing ageing through distinct approaches. These examples show that retailers may begin to mainstream age inclusion as an engagement driver, with iterations likely to deepen intergenerational relevance by delivering participatory experiences across customer segments. By recognising the emotional and financial influence of older generations alongside the aspirational pull of younger consumers, programming that transcends age categories can strengthen intergenerational brand affinity if sustained strategically.

For the retail industry, this shift also represents a strategic imperative. As the majority of disposable income consolidates among older generations and wellness becomes a universal aspiration, retailers that prioritise healthy ageing and intergenerational engagement will be best positioned for long-term growth. Younger generations remain essential to sustained relevance; however, their engagement is most effective when embedded within intergenerational strategies that elevate the service, accessibility, and trust valued by older shoppers while integrating the discovery, wellness, and omnichannel expectations set by Gen Z and Millennials. Department stores have often served as settings for intergenerational traditions such as shared visits and gifting rituals between grandparents and grandchildren. These can be complemented by designing services that intentionally translate elder advocacy into younger loyalty, thus creating a continuum of influence across life stages. Department stores, in particular, have the spatial and experiential capacity to curate environments combining culture with commerce, strengthening brand loyalty beyond transactional relationships. By framing ageing not as an obstacle but as an opportunity for innovation, the retail industry can connect, include, and create enduring relevance in a world where longevity defines the future of consumption.

Conclusion: the next strategic mandate?

A future shaped by longer lifespans and shifting demographics demands a deeper commitment to normalising healthy ageing as part of everyday life, not just as a market trend. Rather than positioning older consumers as an isolated segment, department stores can serve as cultural and commercial hubs that integrate ageing into their narratives by highlighting wellness, vitality, and lived experience across all age groups. Embracing intergenerational programming, experiential retail, and nostalgic storytelling, these spaces can connect generations through shared cultural touchpoints, knowledge exchange, and collaborative participation. Such approaches move beyond the narrow ambition of attracting youth toward cultivating environments where the presence and participation of older adults are seen as enriching for everyone. In doing so, department stores retain their relevance as inclusive institutions capable of bridging generational divides, fostering community, and reframing ageing as a valued stage of life.

Credits: IADS (Anchita Ranka)

IADS Exclusive – From merchants to landlords: how mixed-use projects can future-proof retailers

IADS Exclusive – From merchants to landlords: how mixed-use projects can future-proof retailers

Retail’s “location, location, location” mantra is being rewritten for a post-e-commerce world. Facing online competition, rising occupancy costs and shifting consumer habits, leading retailers are turning their real estate into multi-purpose neighbourhoods rather than single-purpose stores. The article explores this strategic pivot through four emblematic case studies: Ingka Centres opening Meeting Places that weave shopping, offices, hotels and playgrounds in 37 countries to date, Breuninger, whose Dorotheen Quartier opened in 2017 shows how a regional department store can anchor retail, apartments and offices to rejuvenate a city, Walmart, developer of a mall acquired early 2025, aiming to fuse shopping, last-mile logistics, housing and community space into a modern neighbourhood and, finally, John Lewis Partnership, venturing into build-to-rent programmes across the UK that turns surplus car parks into homes above a Waitrose or department-store anchor.

The strategic imperative: why retailers are pivoting to mixed-use projects

Traditional brick-and-mortar retailers face mounting pressure from e-commerce, changing consumer behaviours, and the need to optimise valuable real estate assets. In response, some brands are reimagining their physical presence by developing mixed-use projects that combine retail with residential, office, hospitality, and entertainment. This pivot represents more than just diversification. It’s a strategic response to several critical market forces:

- Real estate monetisation: retailers sitting on prime real estate assets are generating multiple revenue streams from the same footprint. With the rise of e-commerce, some properties can become underutilised, generating costs. Mixed-use development allows retailers to become landlords.

- Revenue stability: by incorporating residential units, office spaces, hotels, and entertainment venues, retailers reduce their dependence on product sales alone, creating more stable and predictable income sources.

- Creating destination experiences: in an era where consumers can buy almost anything online, physical retail spaces must offer something digital cannot. Lifestyle experiences are gaining traction: mixed-use developments can transform shopping from a transactional activity into a social and cultural experience.

- Community integration: mixed-use projects allow retailers to embed themselves deeper into local communities, fostering brand loyalty and ensuring long-term relevance in consumers’ daily lives.

From blue boxes to city hubs: how Ingka’s Meeting Places are re-imagining urban life

Ingka Centres, the real estate arm of IKEA, has pivoted from suburban big-box retail to their Meeting Place strategy, acquiring or building large mixed-use sites anchored by an IKEA store. Combining different functions in one place, these projects want to raise the bar regarding integrated living, working, and leisure experiences and provide an example of how these integral features of modern life can coexist. In 2025, 37 Meeting Places are already open globally, from Poland to China, from Portugal to Sweden. While they are adapting to local specificities, they are either called Avion, Livat or Lykli. Most of them bear a stylised yellow Smiley face, reminiscent of IKEA’s yellow.

One of the most significant examples is the €1 billion Livat complex in Shanghai, China. Opened in September 2024, it delivers a 430,000 square metres programme comprising a multi-functional mix of shopping, dining, entertainment, culture, wellness, children’s activities, and outdoor leisure spaces, aiming to create an all-ages-friendly, one-stop destination for lifestyle and social gatherings. It includes:

- A 200,000 square metres commercial space with more than 312 third-party stores, with approximately 71% being domestic.

- A 21,600 square metres IKEA store.

- Five Grade-A office towers.

- Deliberately non-retail amenities such as a tree-house playground and a Scandi Village, all designed to pull locals in for leisure as much as for shopping.

- Sustainability and community engagement are prioritised: the scheme incorporates an Innovation Hub that showcases circular living ideas and aligns with Ingka’s group-wide People and Planet Positive strategy.

South Asia’s counterpart, Lykli in Noida (in Delhi’s Sector 51 in the National Capital Region, 15 km from Delhi city centre) is scheduled for a 2028 handover. The project is set to attract 25 million visitors and will span 396,000 square metres and combine an IKEA store with 240 retail and F&B partners, two 37-storey office towers and Ingka’s first 267-room hotel. The transit-oriented site has its own two-line metro connection in addition to 4,500 parking lots.

Together, these investments show IKEA’s wider ambition: by owning and curating entire mixed-use districts it can lock in daily footfall for its core store, harvest long-term real-estate income, and run large-scale pilots—from rooftop biodiversity zones to circular-economy retail labs—that reinforce the group’s brand promise of affordable, sustainable living.

From single store to city quarter: Breuninger’s Stuttgart’s Dorotheen Quartier

Department store companies also venture in mixed-use projects in their own ways. As a company, Breuninger imagined and built Stuttgart’s Dorotheen Quartier in 2007, with the department store as its anchor. After 10 years in the making and a €200 million investment, the company opened this 62,000 sqm mixed-use project in 2017 to revive the area located between Stuttgart’s gourmet Market Hall, the historic Karlsplatz and the Breuninger store. Complementing it and consisting of three 6-storey buildings, the area offers a mix of luxury-oriented retailers (including Louis Vuitton, a Porsche dealership and a Tiffany store), restaurants, apartments, offices and a 350-slot underground parking lot. The project involved transforming a street into a retail space, known as the Karlspassage, which is now a small mall connected to the Breuninger store. Overall, the Dorotheen Quartier feels very lively and offers an alternative to Stuttgart’s high-street shopping area, the Königstrasse, which feels outdated (home to Peek & Cloppenburg and Galleria mid-range department stores).

The Dorotheen Quartier exemplifies how Breuninger leveraged a real estate project to create new sources of revenue. The thoughtfully designed mixed-use project has invigorated the area, seamlessly blending luxury shopping, dining, residential, and office spaces to create a lively urban ecosystem, showing Breuninger’s deep understanding of local consumer needs.

From dead mall to neighbourhood hub: Walmart’s Pittsburgh makeover

In February 2025, investing $34 million, Walmart acquired the 112,000 square metres Monroeville Mall in The Pittsburgh area in Pennsylvania, the first time the retailer has ever bought an operating regional mall outright. The company immediately confirmed that the ageing 1969 centre will be re-purposed as a mixed-use district layering new retail, restaurants, residential, hospitality, office space and public realm around (or in place of) the existing anchors. Walmart will also take advantage of the site’s location at the junction of major highways to create a last-mile fulfilment node as well as a community hub.

The project traces its DNA to the retailer’s 2018 Walmart Town Center pilot, which proposed filling the surplus Supercenter parking lots in Loveland store in Colorado, with third-party restaurants, gyms, urgent-care clinics and even apartments, to turn the big-box into the high-street of a walkable neighbourhood. Although the Loveland build never broke ground, the concept now serves as the programmatic blueprint for Monroeville and for future acquisitions the company is reportedly scouting in Texas and Florida. Monroeville will provide the scale test, positioning Walmart not just as the anchor tenant but as a developer of neighbourhoods that can capture retail sales, lease income and e-commerce efficiencies on the same parcel.

From checkouts to check-ins: John Lewis’ push into service-led rental homes

Few legacy retailers have committed to residential at the scale of the employee-owned John Lewis Partnership (JLP). Moving beyond department stores and groceries, the group has pledged to develop and operate 10,000 build-to-rent homes within a decade and has seeded the programme with a £500 million joint venture with asset-manager abrdn. JLP’s ambition is to put excellent service at the core of the UK’s private rental homes sector, with residents treated as customers, not just tenants. The scheme involves:

- Sites and scale: under-used plots such as supermarket car parks and surplus store land will be redeveloped into mixed-use complexes containing apartments and a refurbished or replacement Waitrose or John Lewis unit.

- Homes on offer: one-, two- and three-bedroom flats will come fully furnished with John Lewis products and be supported by 24/7 on-site staff. Planned amenities include shared workspaces, fitness areas and social spaces.

- Management model: rather than selling the homes, JLP will retain ownership and manage them itself, aiming to offer longer leases and a service-led experience more typical of hotels than of traditional private rentals.

This new venture will add a new income stream to bolster its core retail business and make better use of its property portfolio, much of which sits in densely populated areas with good transport links. Converting brownfield sites into housing aligns with the company’s goal of reducing urban sprawl while utilising existing infrastructure.

Entering housing is part of a wider plan to build complementary businesses. If successful, the build-to-rent arm would give the company a foothold in a growing sector while providing a hedge against the volatility of retail income. By recycling underutilised parking lots and back-of-house land into long-hold rental assets, without losing the grocery anchors that guarantee daily footfall, John Lewis is demonstrating how a department-store landlord can turn its real estate footprint into a diversified, inflation-linked income stream while deepening community presence.

Whether they sell flat-packs, fashion or groceries, each of the retailers profiled has reached the same conclusion: single-use retail boxes underperform in an omnichannel era, whereas mixed-use districts can unlock new income streams. The transition from pure retail to mixed-use development represents a fundamental evolution in how retailers can create value. Ingka, Breuninger, Walmart, and John Lewis all start with a strong anchor (an IKEA, a flagship store, a supermarket) and then layer complementary uses, including housing, offices, hospitality, and entertainment, on land they already own. The shared outcomes can be significant with diversified revenues from rents and third-party tenants, reducing the pressure on product sales. Enhancing local communities, live-work-play ecosystems give consumers more reasons to visit and stay, defending traffic against pure-play e-commerce. For retailers evaluating the same path, mixed-use development is no longer a speculative side bet but a strategic shield and a growth engine. By becoming more than merchants, retailers can monetise dormant assets, de-risk volatile sales, and secure a permanent, value-adding role in the urban fabric their customers call home.

Credits: IADS (Christine Montard)

IADS Exclusive –Survival first: how department stores tackle acute crises

IADS Exclusive –Survival first: how department stores tackle acute crises

In the era of multiple systemic challenges affecting the world, the term ‘polycrisis’ has been repopularised by former European Commission president Jean-Claude Juncker and historian Adam Tooze. The utility of the term lies in mapping disparate shocks, that cannot be reduced to a single common denominator, interacting to create a shock more overwhelming than the sum of all individual shocks. In the wake of the COVID-19 pandemic and its long-lasting impacts, economic shocks around the world, Russia’s full-scale invasion of Ukraine, and the spiralling consequences of climate change, the diversity of problems is compounded by insufficient economic and social development for policy, business and individual decision-makers.

Given this context, the IADS undertook internal research to understand how department stores most severely affected by economic and geopolitical crises manage their operations. This exclusive combines the learnings of our exchanges with strategic teams responsible for guiding company activities. Despite the varying natures of crises, the IADS found that the priorities and critical goals for these department stores remain similar in contextually relevant manners. In one line, cash is king and the priority order is people, assets and operations.

Crisis management models: iterative vs. protocol-driven

Crises are rarely identical. While uncertainty permeates all kinds of crises, the source and evolution dictate how stakeholders respond. Department stores have faced a range of crises including full-scale invasions and currency crises, some at the periphery with others at the epicentre, and developed unique crisis models. According to research conducted by the IADS, the types of strategies used can be broadly divided into iterative models, where recovery plans use continuous cycles of evaluation and improvement as situations evolve, and protocol-driven models, that use predefined procedures and clear roles to guide organisations in managing crisis situations.

While adaptability is key in any crisis, iterative models are used by department store companies in volatile situations with little preparation, however, without widespread imminent physical danger. Especially evident in situations where they operate in turbulent political environments, strategic guidelines prove more useful than protocols to respond to new developments flexibly. The level of crisis management experience of decision-makers plays a factor as well.

Protocol-driven models are more common in situations where physical danger to people and assets looms. In the face of airborne incursions and national defence efforts, comprehensive and efficient evacuation protocols for staff, tenants and visitors are foundational for physical safety. Protocols designed to secure the store, inventory and other assets are next. Facing constant uncertainty for extended periods of time gives rise to a new operational status quo that requires updated operating mechanisms. The key necessities in such situations are to identify warning signs that signal the onset of larger crises and focus on recording organisational responses that can be refined over time to develop thorough standard operating procedures.

Liquidity equals lifeblood

The unanimous principal lesson is that managing the company’s cash ensures that the business survives daily. Steep currency devaluation and subsequent inflation are almost always a consequence of considerable crises and need to be managed by every economic actor in the nation. Monetary erosion is normally managed at the government level and percolates down to businesses and individuals. During times of crisis, regulations around currency arbitrage and investment are stricter to meet political goals. Provided banks continue to exist, companies can manage currency devaluation by converting domestic currency to a more stable currency in line with other regulations.

Department stores have employed innovative measures to keep themselves afloat. Heavily indebting a company in the extremely devalued local currency to eventually convert into a more stable currency to repay banks and suppliers, thus transitioning into a financial business, was one of the techniques used. Additionally, collaborating with providers from other, more restricted industries (in one case, the insurance industry) to buy and sell financial bonds was another method to maintain liquidity. Fundamentally, cash is a bargaining chip to find other manners of funding through loans, bonds and financial securities within exceptionally stringent legal limits.

People during crisis: Staff, partners and leaders

There is a consensus about people being the most important resource to address at the onset of a crisis. However, depending on the nature of the crisis and stakeholders, priorities for human resources can range from talent retention, physical safety, and adapted management techniques to the business’ transition to a social unit, among others.

During a crisis, businesses often pivot from pure profit-seeking to a more socially cohesive role, uniting employees, customers, and communities around shared resilience because collaboration and mutual support become essential for survival. Some retailers undertook initiatives such as distributing cash bonuses and paying advance salaries for employees to manage their personal situations. Staff measures depended on urgent imperatives: when retaining employees was the need, companies offered financial, non-financial (such as cars and houses) and personal (such as admission to schools for their children) incentives in individual compensation packages. In other cases, retailers helped employees relocate to safer parts of the country at no expense, as well as provided power banks, headsets, and other operational tools necessary for remote operations. For employees involved in national security operations, companies continued to pay full salaries for three years in some cases.

Continued communication within teams during a crisis is crucial. Some department stores purchased satellite phones for senior executives to combat power outages and maintain connectivity. Keeping employee motivation up in times of crisis is important for their mental health and performance. Advocacy initiatives and collaborations with civil society can rally employees around a unifying purpose, turning uncertainty into renewed motivation and collective resilience.

Another aspect of people management is the relationship with partners, tenants and suppliers. Extensive negotiations are a given to arrive at universally acceptable decisions. Complications arise when partners have different policies than the department store in crisis situations requiring relocation of inventory. Specific store teams coordinate with partners, suppliers, brands, and tenants to access their inventory during crises. Emphasising transparent communication and commitment to cooperation, some retailers have managed to preserve all their longstanding collaborations while adding new partners. However, despite the best efforts, others have lost partners and suppliers who quit the market due to the larger political and economic instability.

Finally, all teams emphasised the importance of strong leaders’ over preparedness and decisiveness. All leaders require a combination of mental resilience, clarity, and strategic foresight. They should focus on issues they can impact while recognising factors beyond their control. Making tough choices is an inherent part of leadership and should be guided by the long-term well-being of the company and its stakeholders. Both the leader and the team must remain agile and ready to adapt swiftly when plans no longer align with changing circumstances. Trust within the team is paramount for strong collaboration, and transparent communication is essential to foster alignment, minimise misunderstandings, and strengthen overall cohesion.

Shielding stores and inventory during disruptions

Department stores’ management of their key assets, buildings and owned stock, is the second-most important priority after people’s safety. In times of acute crisis, physical protection of assets encompasses securing the façade, internal maintenance systems such as heating, water, and electricity, as well as entrances and windows. Compounded by widespread chaos, the risk of thievery, rioting and squatting increases. Some retailers have dedicated, protocol-driven teams that work to secure the building and even live onsite on a rotational basis to counter hostile activity.

In other situations, the threat to assets may not be physical but economic. In cases of currency crisis and hyperinflation, the devaluation of inventory can make stock almost worthless, with government-imposed price cuts having the same effect. A large divergence between the market exchange rate and a government-fixed one further complicates the situation. While the price cuts briefly increased sales, cash flow fell, resulting in unpaid suppliers and exhausted stock. While the product mix remained similar to the pre-crisis situation, this drove a shift in the brand mix. A basic strategy to ensure that products would be sold was mapping key product features to ensure that they were affordable and necessary for customers. For instance, for fashion products, the criteria necessary for their customer base were: under USD 30, exclusive brands, quality, and differentiated from the market. Meeting these requirements reflected a great sell-through rate for this category.

In countries experiencing political instability, there is a risk that government actions may lead to capital expropriation. Remaining politically neutral can keep a company out of the limelight and at a distance from the threat of state takeover.

Pertinent operational continuity: Handling energy and supply chain shocks

Operational continuity depends on the specific nature, scale, and timing of a crisis, requiring adaptable plans that may range from protecting supply chains during a pandemic to reinstating critical systems after an energy outage. A variety of strategies to continue operations can be used. In some cases, department stores reduced the number of stores operated, maintaining only profitable stores. Even during challenging times, department stores continued to make small investments that could have big payoffs when the situation improves, notably in enhancing online operations via marketplaces.

Energy crises are one of the primary challenges during pervasive emergencies. Some dealt with this by implementing a series of operational protocols to optimise electricity consumption during power disruptions. These included reducing energy usage in sales areas by managing lighting, turning off façade lighting during non-peak hours, installation of a diesel generator to maintain operations during emergency power outages, and introduction of start/stop systems on escalators to reduce energy consumption. Installing solar panels on the rooftop enabled clean energy generation, resulting in a 10% reduction in overall electricity consumption, driving long-term operational efficiency sustainably. Mapping the citywide electric network allowed the department store to switch between electricity lines when necessary.

Shocks such as the war in Ukraine impacted companies’ supply chains worldwide, requiring realigned sourcing and logistics strategies, not only around the conflict’s immediate theatre but across entire global networks. To overcome disrupted global sea and air logistics, some retailers shifted to freight transportation for their international supply chains. This has resulted in increased logistics costs and a rise in fuel prices, but a more diverse mix of goods to meet growing demand. The loss of suppliers is almost inevitable, especially when driven by volume reduction due to currency collapse. Department stores coped by simulating purchases from brand headquarters to balance smaller quantities, a larger mix and affordability for customers.

Advertising and customer communication shifted as well. In some cases, all marketing initiatives were stopped to avoid being very visible in the public eye due to the risk of political targeting. Slowly restarting with in-store and social media advertising, the messaging focuses on being quality-oriented to regain customers’ top-of-mind space. Credit initiatives and promotions were also stopped in countries facing extreme currency collapses and high exchange rates. Selling merchandise each day is indispensable since cash flow keeps the business going.

Forward watch and the impact of Trump

Global geopolitical developments, especially the election of US President Donald Trump, are being watched apprehensively by entire populations as his policies have introduced a new wave of changes. Impending tariffs and potential sanctions can upend several business continuity operations during ongoing crises.

Amid multiple systemic crises, intensified by global upheavals and an overarching polycrisis, these insights have been distilled from retailers operating at the epicentre of these events. The IADS aims to lead members into strategic thinking avenues that may not have been addressed before in the face of growing geopolitical and economic uncertainty. While members surely have their own crisis management strategies and teams, learnings from department stores already confronted with profound and overlapping political, economic and security shocks can provide incomparable insight to sharpen and solidify their own playbooks. The commendable resilience and ingenuity shown by those already navigating crises offers a valuable benchmark, prompting others to reflect on and strengthen their own crisis management practices.

Credits: IADS (Anchita Ranka)

IADS Exclusive – Territory expansion: The new playbook for cultural relevance in retail

IADS Exclusive – Territory expansion: The new playbook for cultural relevance in retail

Brands are no longer confined to their original product categories. Instead, they are increasingly expanding their reach into new brand territories, ranging from additional product categories to sports, culture, and entertainment, redefining not just what they sell, but what they represent. This diversification is not about opportunistic line extensions. It’s a calculated repositioning aimed at opening new revenue streams, for sure, but also deepening consumer engagement and embedding brands into broader lifestyle ecosystems. Whether through launching cosmetic lines, furnishing homes, associating with sports performances, staging cultural experiences or producing films, brands are reimagining their roles in consumers’ lives, moving from product providers to curators of aspirational living.

From that perspective, Louis Vuitton, a critical brand for any luxury department store, is probably the most striking example, ticking all the boxes of a brand that has transformed into a lifestyle ecosystem. While many other brands are expanding their territory, department stores need to adapt to welcome these new brand expressions.

Lipstick logic: When brands turn to beauty

The most usual way to expand brand territory is to venture into new product categories. At a time when the beauty and wellness industry has been booming, brands have recently ventured into the coloured cosmetics category. Hermès is a significant example in the luxury price bracket. While they first launched fragrances in 1950, the Perfume & Beauty ‘only’ represented 3.5% of the brand’s total revenue in 2024 (in comparison, Chanel’s beauty business is estimated to represent 35% of the total revenue in 2024). It took Hermès 70 years to initiate a careful foray into colour cosmetics in early 2020 during Covid, with disappointing results. Since then, the Perfume & Beauty division has built up, doubling from €263 million in 2020 to €535 million in 2024, growing 9.3% YoY. While it’s a very significant achievement, it represents limited growth compared to the rest of the business. In 2024, Hermès achieved a consolidated revenue of €15.2 billion, marking a 14.7% increase over the previous year.

On its side, Louis Vuitton began by relaunching its perfume division in 2016. This initiative marked a return to the brand’s historical roots, as Louis Vuitton had released its first perfume in 1927, though it was quickly discontinued. After fragrances, Louis Vuitton will debut colour cosmetics in fall 2025 with the British makeup artist Dame Pat McGrath as its creative director. The line, which will be called La Beauté Louis Vuitton, is the fashion house’s first foray into cosmetics since the 1920s, when it offered a range of powder compacts, brushes and mirrors.

The market is crowded with prestige and luxury brand new beauty lines: Prada, Celine, Rabanne and Dries Van Noten have all debuted cosmetics in the past years. But not only does luxury follow this trend. In 2023, Ecoalf’s founder, Javier Goyeneche (a guest speaker at one of the recent IADS CEO meetings), expanded into sustainable beauty products, seeking to bring its environmental ethos to everyday personal care with Ecoalf Wellness. Assuming customers would be seduced by the brand’s circular principles applied to skincare and hygiene, the brand eliminates single-use plastics and drastically reduces water-heavy formulations, delivering powder-based shampoos, deodorants, and more enclosed in reusable aluminium containers that can last over twenty years.

Not all ventures are successful, though. In 2019, Birkenstock launched a skincare line including eye cream, anti-wrinkle cream and more. While Birkenstock’s surprising move into the beauty sector could represent a natural yet bold progression from its DNA of wellbeing to a broader vision of self-care, these products didn’t sell because offering products such as eye cream was probably too far-fetched. Closer to its DNA and core business, Birkenstock ventured again into beauty in 2024 with Care Essentials, a short and focused foot care line that aligns more closely with the brand ethos. Overall, this transformation highlights a broader trend in which heritage labels utilise their domain expertise to expand into adjacent lifestyle categories, hoping to deepen consumer engagement and open new revenue streams.

Living the brand: How fashion brands furnish everyday life

Brands are not only venturing into beauty but also embracing home design. The first brand to truly venture into furniture, lighting, and home accessories is Armani, which introduced the Armani/Casa label in 2000. This strategy to integrate domestic life continues with the Louis Vuitton Objets Nomades collection, introduced in 2012. Initially conceived as a series of travel-inspired furniture pieces, the collection has since evolved into a substantial home design portfolio, featuring collaborations with recognised designers such as Patricia Urquiola, India Mahdavi, and the Campana Brothers. These limited-edition objects are presented as collectables, elevating Louis Vuitton from a fashion house to a purveyor of high-art domestic experience.

Fast fashion brands also account for successful forays in the home categories. Zara, H&M, and more recently Primark have each undertaken significant strategic expansions into home products to capture a rapidly growing homeware market shaped by post-pandemic lifestyles. Starting in 2003, Zara Home leveraged the same fashion calendar and just‑in‑time logistics that made apparel successful, but uses relatively low discounting compared to apparel, maintaining a premium feel. Financially, the division has matured into a significant revenue driver, with 2018 figures reaching approximately €830 million out of the €16.62 billion total revenue.

H&M adopted a similar but later strategy, first entering the home arena in 2008. Initially sold online and later in stores, the business rationale for H&M Home followed a clear logic: leverage a trusted mass-market retail infrastructure to capture lifestyle spend while maintaining price accessibility, mirroring its “fashion for the many” ethos. In doing so, H&M strengthened its omnichannel ecosystem, using home products to increase basket size and frequency of visits.

Finally, Primark’s entrance into homeware has taken a different trajectory, rooted in physical retail dominance. The retailer began testing its homeware range alongside clothing before making a decisive strategic shift in 2025. The retailer opened its first dedicated Primark Home store in Belfast, showcasing small furniture, bedding, ceramics, and travel essentials in a standalone environment.

Temporary territories: When department stores catch the zeitgeist

There is also an agile way to catch customers’ attention and a share of their wallets. Selfridges and Le Bon Marché offer vivid examples of how department stores have opportunistically tapped into lifestyle trends by temporarily expanding their product ranges to capture additional revenue streams. Following Covid, Selfridges identified an unexpected yet powerful consumer behaviour toward nature, gardening and wellbeing. By mid-2021, its London, Manchester, and Birmingham stores had introduced pop-up garden centres offering a variety of plants and tools, compost, and related apparel. The effort helped Selfridges capture a surge in “green-fingered” spending, translating consumer leisure budgets into in-store impulse purchases on plants and horticultural expert consultations. While Le Bon Marché had the same initiative, this pivot exemplifies how a temporary trend can be monetised through short-term, high-impact product ventures. These initiatives were also incredibly smart in attracting more local consumers, especially at a time when tourism was halted.

Le Bon Marché took an agile approach to pet products in early 2025 by transforming its permanent pop-up spaces into a canine playground under the exhibition banner “Je t’aime comme un chien!”. The initiative mixed dog-centric products, from designer collars, bowls, bespoke toys, treats, spa and grooming services, to a café, workshops, personalisation and photo booths, with immersive visual installations such as big prop bones throughout the store. This thematic takeover capitalised on a widely observed surge in pet spending. Generating high traffic and engagement, Le Bon Marché found the right way to bring dogs and their owners into the shopping journey, strategically steering discretionary spending toward products that align with a momentary yet powerful cultural obsession.

These initiatives are less about permanent transformation and more about momentary alchemy. Selfridges’ plant pop-ups and Le Bon Marché’s dog-themed extravaganza both illustrate a modern department store strategy: not just selling things, but staging culturally resonant experiences that trigger new purchasing behaviours. By reading the zeitgeist and moving fast, with highly curated inventory and thematic environments, these stores created agile revenue plays that capitalised on emergent consumer trends at just the right moment.

Gold, speed, and symbolism: Luxury meets global sports events

Brands venturing into sports is nothing new. Yet Louis Vuitton’s involvement in Formula 1 and the 2024 Olympic Games reflects an increasingly assertive strategy to position the brand at the centre of contemporary cultural spectacle. Over the last decade, Louis Vuitton has steadily moved into the realm of global prestige events, not as a traditional sponsor, but as a supplier of symbolism. In 2021, the brand unveiled a bespoke monogrammed trophy trunk for the Formula 1 World Championship. Its repeated presence on the podium reinforced the brand’s authority and symbol of positive rituals and victory. The move into Formula 1 coincided with a generational shift in the sport’s audience, the sport’s blending of technology, drama, and internationalism offering the brand a stage that mirrored its own values: precision, control, spectacle, and heritage. In early 2025, Louis Vuitton announced a new 10-year significant partnership with Formula 1, beginning with the title sponsorship of the March 2025 Australian Grand Prix. This initiative capitalises on Formula 1’s growing popularity, which attracted six million race attendees and 1.5 billion TV viewers last year, with particularly strong growth among women and youth demographics. The partnership will enable Louis Vuitton to offer unique hospitality experiences for top clients while reaching new audiences. It’s a compelling example of the brand’s broader transformation from a traditional luxury retailer to a cultural powerhouse.

But Louis Vuitton’s ambitions in the sports ecosystem are not isolated. In 2024, the brand expanded its reach further by becoming an official partner of the Paris Olympic and Paralympic Games, joining LVMH’s broader role as a premium sponsor of the event. As part of this engagement, Louis Vuitton designed and produced custom-made trunks for the Games medals. Similar to Formula 1, this foray signals a brand strategy anchored in recruiting new middle-class consumers. In both cases, the brand builds the physical artefacts through which these moments are staged. By embedding itself within the most visible and emotionally charged moments in sport, Louis Vuitton has redefined the boundaries of luxury participation. No longer solely anchored to the runway or its store network, the brand now lives elsewhere, and (already) everywhere.

Beyond commerce: Art as identity

Over the past three decades, luxury groups have moved far beyond fashion and retail to establish a lasting presence in contemporary art and culture. Similar to sports, this shift is not simply an act of sponsoring but a repositioning of luxury as a global cultural force. LVMH, Kering, and Richemont have each established cultural ecosystems to give their brands artistic legitimacy. For LVMH, this began with the 1990 creation of the Prix LVMH des Jeunes Créateurs, followed by the launch of the Fondation Louis Vuitton in 2014, which has become a cultural landmark in Paris. The Fondation has hosted major exhibitions drawing over a million visitors annually and positioning LVMH not just as a backer of the arts, but as a producer of major cultural events on par with the world’s leading institutions.

On its side, the Pinault Collection, distinct from the Kering group, represents one of the most ambitious private interventions in the contemporary art world. Long before the 2021 opening of the Bourse de Commerce in Paris, Pinault had already established two major cultural outposts in Venice, marking a sustained engagement with art. The Bourse de Commerce not only embodies a private collector’s vision but also illustrates how the resources of the luxury sector can be redirected to create enduring cultural institutions that have a lasting impact far beyond fashion.

Richemont has taken a more classical route, yet no less ambitious. The Fondation Cartier pour l’Art Contemporain, established in 1984, predates most other luxury group initiatives and stands out for its consistent, long-term engagement with artists across disciplines. Located in Paris, it recently announced plans to move to a larger site near the Louvre, underlining its institutional ambitions.

The logic here is not transactional but foundational: art and culture are not marketing vehicles but narrative extensions of what luxury is presumed to be: timeless, intellectual, emotional, and transformative. In embedding themselves into art, luxury groups are not just financing creativity, they are quietly recasting themselves as cultural institutions in their own right. This repositioning elevates their brands beyond fashion cycles, resonating long after a runway show ends.

Fashion cinematic turn: there’s no business like show business

As the boundaries between fashion and entertainment continue to dissolve, a growing number of luxury houses are entering the film industry not as sponsors or costume collaborators, but as producers and curators. Louis Vuitton, Saint Laurent, and AMI Paris have each taken distinct yet strategically aligned steps into the film industry, using cinema as both a storytelling device and a cultural amplifier. In 2023, Louis Vuitton launched 22 Montaigne Entertainment, a dedicated production entity. Unlike earlier iterations of fashion-film collaborations, which often blurred into extended commercials, 22 Montaigne Entertainment aims to finance and develop projects. In partnership with Superconnector Studios, this division will be responsible for identifying opportunities for LVMH brands to collaborate with entertainment entities to co-develop and co-produce entertainment properties across film, television, and audio. However, it is likely that LVMH also has an eye toward producing larger, more mass-entertainment offerings, such as The House of Gucci movie, which grossed $166 million worldwide at the box office.

Saint Laurent, by contrast, has made the most direct and structurally ambitious move into filmmaking. In 2023, the house launched Saint Laurent Productions, becoming the first luxury brand to create a registered film production company. Its debut collaborations with auteurs such as Pedro Almodóvar and David Cronenberg made immediate headlines at major festivals including Cannes and Venice. Jacques Audiard’s Emilia Perez movie was a particularly striking example: it co-produced the entire feature, collaborating closely with the other movie-producing companies. The result is not mere branding, but active, creative authorship, with Anthony Vaccarello, Saint Laurent’s creative director, serving as a credited producer on the project.

AMI Paris’s entrance into the cinematic world took a more institutional turn in 2024 with the creation of the Grand Prix AMI Paris de la Semaine de la Critique, an award presented during the Cannes Film Festival that celebrates emerging filmmakers. Founded by AMI Paris’s founder and creative director Alexandre Mattiussi, the prize is designed to support the kind of filmmaking that aligns with AMI’s cultural positioning.

Together, these three brands represent different yet converging models for how fashion intersects with cinema. Louis Vuitton approaches it as a narrative architecture surrounding the brand’s universe, Saint Laurent treats it as a parallel industry in which to operate and AMI Paris uses it to enhance the brand’s emotional temperature. Each strategy points to the same conclusion. In a saturated visual economy, luxury no longer communicates through clothing alone. With its emotional depth, films offer a medium through which to project identity, build mythology.