IADS Exclusive Articles

IADS Exclusive - All you need to know about Buy Now Pay Later

IADS Exclusive - All you need to know about Buy Now Pay Later

Buy Now Pay Later (BNPL) financing solution is not new, and retailers already know for years such interest-free instalment plans. While basically being a loan, it is nowadays marketed as a convenient payment option and has steadily and quietly developed over the 2010’s. Covid-19 only accelerated its growth as both retailers and consumers found great interest in such a payment method.

According to Affirm fintech, BNPL is expected to triple over the next two years. Stating BNPL is rapidly growing is an understatement. According to

r6872_9_article_1_-_buy_now_pay_later_platforms_-_coherent_market_insights.pdf

published in July 2020, the global market was valued at USD 7 320 million in 2019 and should reach USD 33 638 million by 2027. North America is currently the biggest market by volume and revenue and Asia Pacific is expected to be the fastest growing region in the future.

That said, what does BNPL have to offer? Should retailers bet on it and why? Should customers trust such a payment method? Is it a sustainable model or will it change in the future?

BNPL and retailers: a match made in heaven?

First, let’s see how it works from a financial point of view. Like most payment solutions, BNPL firms are paying full purchase amounts upfront while charging fees to retailers: they are usually coming as a flat fee along with a commission, both taken on each transaction. Depending on the countries and whether it’s Afterpay, Klarna or Affirm (some of the largest BNPL companies), fintechs charge retailers a flat fee of USD 0.3 to 1 (for processing the payment) and a commission of 3% to 6% depending on the purchase amount. These rates are higher than debit card (accounting for 0.5 to 1% per sale) or credit card ones representing up to 2% per transaction.

Retailers’ margins have been dramatically challenged over the past years. Discount periods and rates have only been rising, sometimes representing up to 10 months a year, especially in fashion, a crucial part of the business for most department stores, and for BNPL users. Acceleration in e-commerce has also been affecting margins with supply chain investments and customers’ expectations for free and fast deliveries. In this environment, BNPL solutions are efficient but they surely represent additional costs for retailers. Last, it’s worth knowing that, as Klarna states on its website, BNPL technology allows customers to set price alerts on saved items for them to “never pay full price again”. Not really a message merchants want to hear…

On the bright side now, numbers claimed by BNPL companies are like winning the lottery as the benefits in volume and recurring spending seem to be worth the high fees. Retailers, by offering a BNPL option, are creating a relationship with consumers that are keen to purchase. According to BNPL companies, shopping carts increase up to 30%, abandonment at checkout decreases up to 25%, repeat customers increase up to 20%, and return rate reduces. Affirm, Afterpay, and Klarna see average basket value rise 85%, 30%, and 45% respectively.

The magic in BNPL solutions also stands in their younger customer base. Afterpay claims that 73% of their shoppers are Millennials and Gen Z consumers. And merchants say that 30% or more of Afterpay customers are new to their brand. Macy’s (partnering with Klarna), said that 40% of shoppers using BNPL are new shoppers and 45% are under 40 years old. Only 25% of Macy’s existing customers are under 40.

Considering the challenges retailers are currently facing, proposing a BNPL payment option is worth it: sales volume will increase, customer base will grow and merchants might start long-term relationships with younger consumers they would not have been able to reach otherwise. Retailers will also benefit from additional and unprecedented visibility thanks to BNPL apps, designed to display brands and products in a seductive way. These new shopping apps are a complementary channel for retailers, and an important one as they are targeting younger generations.

Many younger customers are considering themselves as being part of a community. This is why word of mouth explains a fair part of the BNPL success, recommendations from friends or influencers working their magic. In 2020 in the U.S.,

r6873_9_article_2_-_buy_now_pay_later_services_growing_quickly_among_u.s._consumers_-_the_ascent.pdf

shows 27% of BNPL users heard about it on social media and 18% through friends and family. In this environment, BNPL is appealing to younger generations facing difficulties in accessing credit cards or simply considering them old-school or untrustworthy.

Furthermore, BNPL is about data. Becoming shopping destinations, BNPL apps are connecting customers to merchants thanks to an algorithm personalising brands, products and deals for each user. Needless to say, fintechs are gathering a huge number of information on shoppers while remaining very silent about the ownership of such data. Because of that, it’s hard to believe that ownership would go to retailers. So the question is key when entering a deal with a fintech. But retailers might learn a lot about their new customers anyhow, as they are collecting all information about the purchase itself.

IADS members have already embarked on BNPL business. Interestingly, The SM Store in Philippines has developed a partnership with 13 banks, not with a BNPL fintech. Started in January 2021, the department store offers to pay any item in 3, 6 or 12 interest-free instalments, depending on the purchase amount. Though they are not called BNPL, IADS members are offering -and have been offering for a while- instalment plans through their credit cards.

Pay later, but pay up

Whether it’s through Netflix or Amazon Prime, we are all living a part of our lives through subscriptions. Watching a movie at home has become a seamless experience as well as its payment thanks to monthly instalments. As a result, consumers are more and more used to frictionless and contactless payments solutions and Covid-19 has accelerated this trend.

When it comes to customers, BNPL promise is double. First, convenience. As applying for a classic instalment through a retailer’s credit card requires much information and sometimes frictions and delay, the BNPL registration process is supposed to be seamless and fast. The approval, relying on the shopper’s debit card, is occurring in real time and not affecting applicant’s credit score (assuming they pay on time).

The payment part is easy: shoppers just have to confirm instalment terms (number of payments, amount of each one) and total cost of the purchase. Payments due in three or four instalments are interest-free, while the interest rate goes from 15% to 24% for payments from five to six instalments or more. If BNPL option is not offered by the retailer, fintechs can instantly create a virtual one-time card number to be added to Apple or Google wallets.

Convenience is also a factor in budget management. A Cornerstone survey shows that most BNPL millennial customers in the U.S. don’t really need to postpone payments as they earn more than USD 75 000 a year and hold credit cards, but rather prefer paying in instalments to help their budgeting.

Second part of the promise: providing essential financial service. Given the current economic environment, it’s true that flexible financial options have proved necessary to some people. To appeal to them, Affirm motto is reassuring: “Pay at your own pace. When you buy with Affirm, you always know exactly what you’ll owe and when you’ll be done paying. There are no hidden fees—not even late fees.” BNPL solutions usually cover payments from USD 50 to USD 17 500 so they are now also used to pay for small daily expenses, bills, or even tuition fees.

Trouble in paradise?

One of the main interests for merchants using BNPL solutions is to access to younger customers and engage in long-term relationship with them. But it might come at a risk. A BNPL study conducted by The Ascent shows that only about 1 in 5 of consumers who use BNPL apps actually understand how they work. To some immature customers, an item will seem more affordable than it is if its payment is split in multiple months. If they end up paying important additional fees, who will the shopper blame, the BNPL company or the retailer? One can guess that the retailer will be seen as guilty, putting the customer relationship at risk for the future.

Whether it’s splurging or just paying for commodities, these payment options are often stretching consumer financial capacities beyond their real means, leading some of them to fall into debt. And this is currently the major factor limiting an even bigger increase of BNPL, as complaints regarding the late fees are increasing. For instance, Afterpay charges USD 10 for each missed payment and USD 7 if the instalment remains unpaid after a week. Users missing all the instalments are charged a late fee of USD 68. Considering most of the payments made using BNPL are under USD 500, these fees are relatively high.

According to a survey conducted in the U.S. in November 2020 by Credit Karma, nearly 40% of consumers who used BNPL missed more than one payment. Nevertheless, Klarna, which has partnerships with over 250 000 retailers, said credit losses have fallen across all major markets. Afterpay, also said that late fees from consumers accounted for less than 9% of company’s income in the 2020 last quarter.

What’s next for BNPL?

While BNPL business surged with the pandemic, and given the nature of its customer base, the question of responsible lending policies arose in some countries. In the U.K. for instance, where the BNPL market represents USD 3.7 billion, consumer groups asked for regulation. As a result, the U.K. Treasury announced BNPL companies will have to conduct affordability checks before lending to customers.

More responsibility could come through certification. Sezzle, a BNPL company has recently been “B Corp” certified. This certification concerns for-profit companies that are taking into account the community they are engaging with. In the case of Sezzle, “B Corp” certification has acknowledged a commitment to financial education and a support to young adults in their purchase needs.

But still, is BNPL a sustainable business model? Fintechs could be considered as an additional middle-person between consumers and retailers, a position usually only occupied by banks. This is where an interesting battle might happen. As a direct competition to banks, Affirm launched a debit card, showing BNPL companies are willing to gain on the banking industry. On the other hand,

r6874_9_article_3_-_how_banks_can_use_customer_data_to_compete_in_the_buy_now_pay_later_space_-_forbes.pdf

knowing they are ideally positioned to enter the market. They are able to tailor BNPL solutions through their own debit or credit cards, additionally taking advantage of all the data they own as well as their capacities in terms of security. In that case, banks could eventually eat BNPL firms alive.

***

What about retailers? Even though BNPL might only be a fleeting trend led by younger generations, offering a BNPL payment option to customers is as profitable as it is necessary to gain additional shoppers and new sources of revenue. At least for the time being, even if BNPL solutions are a competition to retailers’ credit cards.

For tomorrow, the goal could be to transform these shoppers into store-branded card holders by evolving the credit card solutions to include BNPL options. The example of Macy’s is really of some interest. Besides offering Klarna’s BNPL options to customers, the department store has invested in the fintech, showing a first step and possible path to fully include BNPL in its offer.

Credits: IADS (Christine Montard)

IADS Exclusive - What should we do with our stores? Close some and change others

IADS Exclusive - What should we do with our stores? Close some and change others

Many department store companies today are struggling with their physical store legacy. Stores may be too big, too many or unsuitable. Some big decisions are currently being considered in the light of the acceleration of trends provided by covid, the apparent disaffection of customers with stores and the declining profitability of the existing department store model. Some companies are closing stores, some are upgrading them, and others are considering different business models.

Stores vs online, and brand value

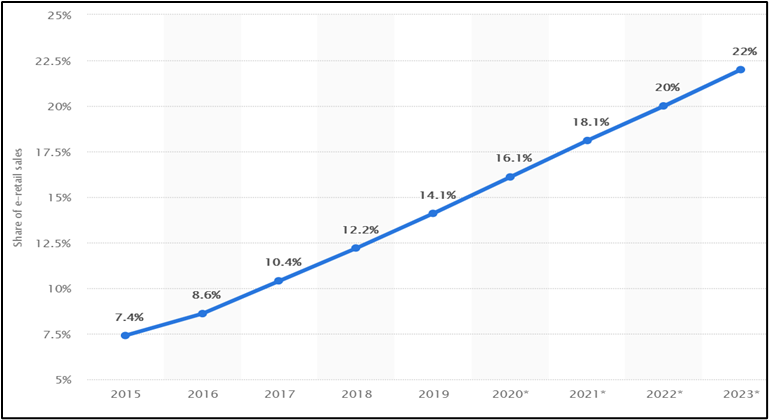

Figures from before the covid pandemic estimated the global share of online retail to be 18% in 2021. This is now probably a serious underestimate.

The true figure has certainly leapt in some countries due to lockdowns, in some companies who had been resisting online investments, and indeed in those companies who were most advanced in omnichannel retailing who saw a real possibility of making up for losses from stores through the online route.

As the graph shows, the increase in the share of online retail was a trend before covid. It has likely been accelerated over the past year, which means that it will not return to its previous level but will continue to grow more steeply.

The negative impact on physical stores is a clear example of businesses suffering more from their own actions than from those of competitors. Indeed, the discussions about overstoring have been going on for some time. Even companies which have been aggressively growing their online business have often simultaneously been multiplying or expanding stores.

Some believe the most important asset of retailers lies in their brand value. The recent case in the UK of Boohoo.com acquiring Debenhams and Arcadia brands without the stores, and Asos buying Topshop, again while closing all their outlets, are cases in point. Barneys, once a famous luxury department store operation in the US, is now owned by Authentic Brands Group and licensed to Saks. The selling off of the physical real estate, often initially with a lease-back deal, may be an early sign of the end of the traditional model. The latest case is that of Stockmann in Finland which has recently sold off its Helsinki, Tallinn and Riga stores.

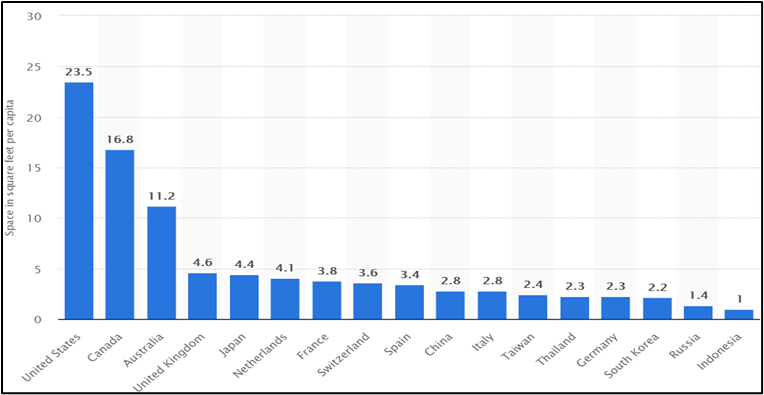

How does one determine whether a particular market has an excess of retail space?

According to Statista, the retail space per person in selected countries in 2018 was as follows:

Another trend which arguably started well before covid was the “unmalling” of America and traditional store closures in many other markets too. But according to Coresight, in the year so far in the US there have been 2548 store closures and 3199 openings. The positive balance of openings, however, are often on a very different basis. For a start they have different, shorter and more flexible lease conditions, the rents are lower and/or adapted, and the stores themselves are often quite different (not least, smaller footprints). One commentator has only half-jokingly described stores for the new generation of retailers as a customer acquisition cost. The chart above shows different retail space densities across countries, showing both excesses and potentials.

What’s the use of selling space?

So how have department stores been reacting to this situation?

a) Reducing or closing

As some department store companies have been failing, there has been something of a natural attrition of stores. This has been the case with Debenhams and BHS in the UK, for example. Some companies have been closing stores, starting with the least profitable ones such as Galeries Lafayette transferring part of its regional network to franchise operators, Macy’s or John Lewis. The John Lewis case is particularly interesting since it has long been expanding physical stores: between 2008 and 2016 (the last year it gave figures), it increased selling space by 40% at the same time that it was pushing online growth. It argued for the “halo effect” at the time, saying that £6 out of every £10 spent online was driven by the shops. That figure today is only £3. In the meantime, it is planning to reduce drastically its retail footprint in its Oxford Street store, converting the rest to offices. Something similar is being planned by Marks& Spencer at the Marble Arch end of Oxford Street which has applied to demolish the building and replace it with a smaller store topped with offices. Fenwick, an important store and real estate owner in New Bond Street is doing the same while simultaneously struggling to build an online presence.

b) Changing or transforming

The fact that John Lewis is closing 16 out of 50 stores will free up investment funds allowing it to give the remaining stores a fighting chance. But the remaining stores will have to be different. Not only is John Lewis thinking of a totally different use of space such as housing or entertainment, but it is also apparently looking at other forms of retail such as garden centres. Other companies which own or have use of their store buildings are converting them to offices like Filene’s in Boston, into “dark stores” like El Corte Ingles in Eibar, or thinking of the department store as a mixed-use complex including hotel, shopping and restaurants like the yet to be opened Samaritaine of the LVMH group in Paris. What is clear is that the traditional department store format will not cut it at the moment, if only because it is not sufficiently profitable as a model to survive in current numbers. Other models have come into existence such as Showfields or Neighborhood Goods which would appear to be better adapted to consumers’ expectations. Or going further still, Amazon and Walmart, from opposite directions, seem to be thinking of physical stores as “satellites” in the retail ecosystem.

c) Flagships plus local

While a number of smaller outlets are being reinvented as local stores with an emphasis on personalised service with agile and flexible structures adapted to the convenience of local customers (see IADS Exclusive on local), flagships are developing their USPs for the future and acting as brand carriers for their companies. Recently remodelled or even recently built stores will still have a significant role to play in the future as they stand as attractions in their city centres. Numerous examples prove this point such as Rinascente in Milan, El Corte Ingles in Madrid, Selfridges or Harrods in London and others. Most striking are those which have committed to major architectural creativity, starting with the 2003 Selfridges in Birmingham by System Design with Amanda Levete, and continuing in no specific order with the Galeries Lafayette Champs Elysées with BIG, their Foster designed Luxembourg store, the KaDeWe concept by India Mahdavi, the Breuninger Dusseldorf by Daniel Liebeskind, the Galleria Guanggyo, Korea, by OMA, the above mentioned Samaritaine by Sanaa of Japan, and many others. Architecture is not enough, however, and it will remain to be seen how successful these investments turn out to be in building the brand and attracting customers.

Department stores are dead, long live department stores

Department stores can be city landmarks where life and experiences are lived; they can also be convenient local places for shopping and picking up orders; and they have become the physical face of an omnichannel ecosystem which can take many forms. The nature of the stores themselves is shifting, as is the organisation structure behind them, and the profit model on which they are based. These shifts question the need for traditional store formats and organisation.

Many companies have reached a point where they appear to have too many physical stores and/or too much selling space. The examples above point to actions that have been taken by some companies faced with these problems. In some cases, they are surprising and reflect difficult choices. But they are also signs that department stores are resilient, adaptable and evolving. The need for innovation is greater than ever – and this means retail innovation. We need to remember that technology itself is only a tool (albeit a useful one) and not a substitute for new retail thinking.

Credits: IADS (Dr Christopher Knee)

IADS Exclusive - Retail Review #3: luxury concept stores

IADS Exclusive - Retail Review #3: luxury concept stores

Keeping markets under close watch, IADS collected innovative concepts related to key topics such as luxury experience, contemporary models, and reinvention.

Check out what luxury stores are thinking up to capture customers' attention in the third edition of the Retail Review.

Louis Vuitton, Tokyo

Inspired by reflections of water expressed through the building’s rippling exterior, the luxury retailer’s Tokyo flagship location has been completely transformed by Jun Aoki and Peter Marino. The store offers a full range of collections with upper levels dedicated to VIP clients.

Hermès, Tokyo

As Hermès reopened one of its Paris locations, it also opened a new flagship store in Tokyo inside one of Omotesando’s most notable buildings. Upon entering, customers can peruse silk, jewellery, beauty, perfume, leather, and equestrian collections for both men and women.

Hermès, Paris

Hermès’ beautiful flagship on Rue de Sèvres in Paris has undergone a year-long renovation with its central striking feature of three huts made from ash wood, which the VIP lounge overlooks. The store has been fully reorganized to house evolving product lines, including its recently launched colour cosmetics collection.

Browns, London

The London store is the newest manifestation of Farfetch’s Store of the Future, blending digital and physical experiences by using an app that connects with interactive mirrors to give recommendations and provide product details.

More on Browns’ new boutique in London

Kith, Paris

In Paris, visitors are presented with a restored Carrara marble staircase that falls under a chandelier-adorned ceiling crafted with resin-cast Nike Air Max 1s. The space presents Sadelle’s restaurant in the courtyard and a basement level used as a rotating gallery space.

Swarovski, Paris

Moving away from the accessibly-priced space, a crystal Willy Wonka factory concept appeals to a wider audience to showcase the brand’s shift into luxury. As customers sit on a sofa surrounded by walls of colourful jewellery, salespeople bring the products on trays for a personalised experience.

Diesel Hub, Shanghai

In an effort to converge living, dining, working, and shopping, Diesel has partnered with RTG Consulting and Muse Group to unveil a new concept for the brand called “Diesel Hub” in Shanghai. The 900 sqm retail space offers a Diesel Brave Bar that proposes food, beer, and specially developed spirits.

IADS Exclusive - Sustainability series #5: GOTS

IADS Exclusive - Sustainability series #5: GOTS

What: A certification with strict environmental and social criteria for operations along the entire textile supply chain.

Why is it important: The recognition of the GOTS certification across consumers and business channels has grown incrementally year over year and has a direct impact on purchasing and partnership decisions.

Textiles have proven to be an important good in the past year as COVID-19 has called upon many industries to shift their supply chains to answer the increasing demand for masks and medical supplies needed around the world. To continue the sustainability series, we will explore one specific certification that addresses organic textile production: the GOTS certification. As consumer interests in the transparency of the supply chain connected to their fashion brands continue to rise, department stores need to promote their GOTS products and partnerships and ensure that there are sufficient organic products available for these environmentally aware consumers.

What it is

The GOTS (Global Organic Textile Standard) is the world’s leading textile processing standard for organic fibers. The standards were developed by the certifying bodies IVN (International Association Natural Textile Industry), JOCA (Japan Organic Cotton Association), Soil Association, and OTA (Organic Trade Association). GOTS enables textile manufacturers to qualify their organic fabrics and garments with one certificate accepted in all major world markets. This is an important step towards the harmonization and transparency of textile labels.

A GOTS certification is an assurance that the product meets the global standards for the processing and manufacturing of organic textiles. The standard covers the entire post-harvest processing including spinning, knitting, weaving, dyeing, and manufacturing of apparel and home textiles made with certified organic cotton and wool and includes both social and environmental criteria. GOTS is a key certification to ensure the authenticity of organic fiber and its safety.

How it works

GOTS sets the standard by creating requirements for the production of organic textiles to make sure every step of the supply chain is covered from harvesting and sewing to packaging. The requirements are based on environmental and social criteria to guarantee that the textile is produced in an eco-friendly manner. It also certifies that laborers and workers are protected and treated with fair trade norms during the process.

Some of the key features of GOTS is that it prohibits the use of harmful chemicals in the production of organic textiles, it covers the entire production process from plant growth to packaging materials, and the textile must have 70% organic fiber at minimum. If chemicals are used, they must adhere to strict environmental and toxicological guidelines. All textiles must meet a certain level of criteria and quality to be certified and the product is tested and appraised at every stage of the process by an experienced certifier. All processors and textile manufacturers are expected to meet strict social criteria to ensure fair trade practices and safe working environments. Yearly audits and surprise checks are conducted to verify that there is a continuance of correct practices.

GOTS is not the only standard that exists in the cotton and textile space. The OCS (Organic Content Standard) is used to verify organically grown raw materials from farms to the final product to increase organic agriculture production. OCS has seen record growth with a 48% increase of certified facilities in 2019. Another noteworthy certification is Oeko-Tex which qualifies that textiles are free of harmful chemicals and safe for human use. While GOTS only covers organic textiles, Oeko-Tex includes certifications associated with organic and non-organic textiles.

Why is it important

Until 2003, the sale of organic cotton items in the United States relied predominantly on e-commerce, mail order catalogues, natural and health food stores, and small specialized eco-textiles shops or boutiques. Today, department stores like Nordstrom and brand stores like American Apparel, Levi’s, Nike, and Timberland also have organic cotton items for sale.

The trend of using organic cotton has expanded a lot from the United States to Europe in the past few years. Typically, brands have found that outsourcing their eco-textile and organic cotton items to Turkey, China, India, and Pakistan can reduce costs and increase economic efficiency. American Apparel, on the other hand, uses GOTS-certified cotton to process sweatshop-free t-shirts made 100% in the United States in downtown Los Angeles. The company’s turnover has increased 50% per year since 2002 and the brand has expanded to Europe through its success.

In Europe, Germany and Switzerland are the top two markets for organic cotton textiles. The French market for fair trade products is also growing rapidly. With the involvement of large brands and retailers, the number of points of sale for organic cotton and GOTS-certified items has exponentially increased and can be found in regular sale channels like department stores and supermarkets.

The concept of organic cotton is successfully being marketed to brands and retailers in the fashion industry as being part of their policies for CSR (corporate social responsibility). The involvement of large fashion brands and retailers that are using organic cotton has generated a lot of attention from other parts of the textile industry, from designers and the media. This has further strengthened the interest of consumers in organic cotton textiles and clothing as well as their willingness to purchase.

Limits and Criticism

In 2019, 40,645 metric tons of organic cotton were sourced from Xinjiang, China, a province with allegations of forced labor, prison labor, child labor, and serious human rights infringements. The region produces one-sixth of the world’s global organic cotton. Credible reports of forced labor involving the Uyghur and the Kazakh ethnic groups in China have caused some countries, such as the United States, to ban the import of both raw cotton and goods containing cotton from the province.

There are eight GOTS-certified facilities in Xinjiang, yet GOTS has failed to comment on the implications or impacts of this revelation of harsh labor environments on the future of these facilities or their certification. GOTS’ silence around the issue is a bit alarming as China has the fifth-largest amount of GOTS-certified facilities in the world.

As the region produces such a large portion of the world’s cotton, the traceability of the cotton from Xinjiang can become easily blurred as it moves through various supply chains and gets mixed with other textiles around the world. Traceability can be a difficult topic, but GOTS was ranked best in the “Traceability of Clothing with Textile Seals” by the German consumer product testing organization Stiftung Warentest. They concluded that GOTS offered full transparency and traceability while complying with strict social and ecological criteria through all stages of production.

GOTS: The latest fashion trend

GOTS-certified textiles have created quite the buzz in the fashion industry from consumer demands. The Organic Industry Survey conducted by Organic Report reveals that savvy customers seek out companies of integrity through the achievement of GOTS certification. It seems to have become the standard that the market expects on a global scale. In 2019 alone, the number of GOTS-certified facilities grew globally by 35% from 5,760 to 7,765 located in 70 different countries. The growth has been seen in both production and consuming regions.

Retailers do not need to be GOTS certified unless they are involved with a business-to-business trade activity where they sell to other retailers or they repack and relabel the GOTS products. The benefits of certification include streamlined processes when adding a product to the certification or getting label approvals throughout the year, a license number that will help keep trade secrets confidential, and access and membership to the GOTS public database which receives over 2,000 hits a week in the United States.

Though retailers and department stores do not need to be GOTS certified, it is important that they are transparent about their affiliation, if claimed. While the GOTS logo can be used on websites or labeling, retailers need to make sure not to give the impression that all products are GOTS certified. If the GOTS logo is used in general to show that GOTS goods are sold among others, each GOTS product must show the logo with its license number, label grade, and certifier reference. The GOTS organization audits and investigates any unauthorized or misleading use of the trademark and will take legal or public action if needed to safeguard the credibility of the program and labeling system.

With COVID-19 increasing the demand for masks and medical gowns to be manufactured, being GOTS certified has helped some United States companies win state and federal contracts because of their proven traceability systems. This raises a few interesting questions to think about. Does this mean that GOTS certification can bring a competitive advantage not only with consumers but also in the business-to-business world? Can affiliation with GOTS certification open doors to other business opportunities? On the consumer side, should department stores ensure that there is a certain percentage of GOTS-certified merchandise offered to meet the rising customer demands?

Credits: IADS (Mary Jane Shea)

Read Also: Textile Exchange Organic Cotton Market Report 2020

Read Also: GOTS label guidelines

IADS Exclusive - Department stores selling books and culture

IADS Exclusive - Department stores selling books and culture

Department stores today rarely offer books, music, films and other “cultural” goods. These have reverted to specialists, chains and online retailers. However, the chains have consolidated and are doing less well; and the digital retailers appear to have peaked, while smaller, local booksellers are gaining in popularity. Is it possible that department stores could once again find a place for these goods in their local offer which has gained in popularity during the covid pandemic?

In the beginning was the word

One of the earliest US department stores, Marshall Field’s in Chicago, was famous for its customer service (“give the lady what she wants”), its revolving credit and for the use of escalators. But in terms of assortment, it was notable among other things for its legendary book department which introduced the idea of “book signing”. Its book department is now long gone (the store trades as Macy’s) as indeed book departments in so many department stores have disappeared.

These book departments were often paired with music (vinyls, cassettes, CDs) and films (VHS, DVDs) which have undergone such a revolution, both technological and commercial, that they quickly became the exclusive domain of specialist retailers which have now more or less completely gone digital.

But what happened to books? Department stores were the victims first of the growth of specialised

r6675_9_booksellers_that_have_closed_for_good_across_the_years_business_insider.pdf

. These included in the US, Bookstop (1982) acquired by Barnes and Noble; Borders Books (1971) taken over by Kmart and eventually liquidated in 2011; Crown Books (1977) liquidated in 2001; Waldenbooks (1962) merged by Kmart with Borders and liquidated in 2011; B Dalton founded by Dayton Hudson department stores (1966) acquired by Barnes and Noble in 1987 and operated until liquidation of the last 50 stores in 2109.

In the UK, a similar growth and consolidation movement was taking place with Dillon’s, Ottakar’s, Books Etc (part of Borders), and the 115-year-old Foyles gradually becoming part of Waterstone’s.

“You’ve got mail”

This growth of book chains was portrayed in the 1998 movie You’ve got Mail about the giant book chain threatening the local bookstore business. According to Experian, the number of UK bookshops fell between 2005 and 2012 from 4000 to 1878.

However, neither of the two book giants Barnes and Noble nor Waterstones is currently finding life easy, not least because of the entry onto the market of Amazon, starting slowly in 1994 to digitise the book business first through online selling of paper books, then through digital book sales.

While the sale of e-books was growing, that of physical books continued to fall, for example from from

r6677_9_rise_of_e-books_results_in_50_of_bookshops_closing_down___the_drum.pdf

. However, others claim that the decline of bookshops has now significantly slowed, and furthermore, that the number of independent bookshops grew by 35%

https://www.iads.org/files/pmedia/public/r6676_9_why_the_number_of_independent_bookstore...pdf

r6676_9_why_the_number_of_independent_bookstore...pdf

. E-book sales have recently been fairly static and subscription services modelled on Netflix or Pandora have struggled while the resilience of paper books have proved a boon to independent booksellers

https://www.iads.org/files/pmedia/public/r6678_9_the_plot_twist__e-book_sales_slip_and_...pdf

r6678_9_the_plot_twist__e-book_sales_slip_and_...pdf

. E-book titles have been declining generally, including for example Italy where they fell by 5.4% in 2019 after falls of 17.2% and 15.9% the two previous years.

The rebirth of independents

Waterstones, which appeared to be in deep trouble ten years ago, is reinventing itself under James Daunt of the ex-independent bookshop on Marylebone High Street in London, Daunt’s bookshop (now part of Waterstones). Elliott Management, Waterstone’s owner, agreed in 2019 to buy US Barnes and Noble in a $ 683 m deal. James Daunt will move to New York and attempt to work his magic on the 627 US stores at the same time as continuing to lead Waterstones. He claims that in the book trade, Amazon has probably reached the peak of its influence and that there are limits to the online experience.

One of his strategies at Waterstones’ 280 shops has been to devolve power to local managers particularly over purchasing. This contributes to a more efficient management of stock, reducing the costs and time involved in handling returns, books bulk ordered by head office with little regard for differences in regional reading habits.

One of the competitors which Barnes and Noble will be facing is, of course, Amazon itself whose 20 or so shops around the country are benefitting from the data that Amazon collects on the market. Publishers on their side are suffering under the brutal negotiating techniques of Amazon which is threatening publishing as it has already music and films. On the other hand, of course Amazon has opened the world of books and enabled publishers to reach a wider market.

The local offer for the local department store

Notable bookshops around the world include Daunt’s in London or Lello in Porto representing an almost caricatural but striking model of traditional bookshop architecture; The Strand in New York with its reported “18 miles of books” and its passion for everything written including banned books; Shakespeare and Co in Paris, the archetypal writers bookshop with its rich history of famous patrons (which is suffering badly during the current pandemic); Livreria Cultura in Sao Paolo serving as a spacious and comfortable meeting place in modern design style; Starfield in Seoul with its truly breath-taking height of bookshelves. All of these demonstrate the importance of branding, each one immediately recognisable in ways that the chains cannot match with their “cookie-cutter” formats, however innovative they may seem at first.

They also all know their customers and have made deliberate choices. A more recent version of this is the local focus of the kiosk formats emerging in Barcelona which cater to local customers and offer targeted press, magazines, coffee, and some seating.

Some department stores have not abandoned books. Indeed, Harrods entrusted its book department to Waterstones for 20 years until 2011 (when it switched to WHSmith). De Bijenkorf in Amsterdam has handed its book department over to AKO, part of Audex, in their words a partner who is able to target the Bijenkorf customer. In a similar vein, Manor in Switzerland has recently signed a partnership with French international Fnac group to provide books, audio, video and electronics. Fnac has the same deal in Andorra with Pyrenées department store. Printemps in Paris has a collaboration with the emblematic Gibert bookstore. The BHV store in Paris offers a book selection which is tailored to its customers, as does the Bon Marche. KaDeWe has a selection of books and art on the fifth floor, Selfridges offers a selection, while Ludwig Beck in Munich still offers books alongside its famous and very substantial music department.

Whether or not these examples are profitable, they may nevertheless constitute efforts at generating traffic, which department stores are sorely in need of currently. They might achieve this through the local appeal of their offer, through the theatrical experience they generate, and through the contribution to the value of the retail brand, just as the book department at Marshall Field did in its early days in Chicago.

So what about department stores

If, as seems to be the case, there is a continuing market for physical books (and perhaps other cultural goods), department stores might consider regenerating their offer to customers in some form or other.

The offer might be centred around convenience (guides, reference books, magazines…) which is what Harrods appears to be opting for with WHSmith rather than Waterstones; or it could consist of inviting a local notable shop to open a branch in the store just as so many have invited fashionable restaurant formats into the store.

This raises the question of whether the culture offer should be own-run, an arguably costly solution, or whether it could be entrusted to a specialist as has been the case in Bijenkorf.

Whatever is decided, a book or cultural goods offer opens the potential of a collateral offer of stationery, writing, cards which can all be personalised, and which potentially may be more profitable.

Some department stores see books and more as part of a “gift” offer such as the Galeries Lafayette “System Bookstore”, the design department at Rinascente, or local museum shops, for example. Some books are published quite explicitly as gifts or coffee-table books, and books in general as gifts are traditionally seen as less personal than jewellery, but they say more about the giver. Amazon has a category explicitly allowing purchasers to send books as gifts.

Finally, books and indeed other cultural goods need not be grouped in a specific department but may be scattered around the store to create a lifestyle feel, just as Selfridges may sell cookery books in one of its restaurants, or fashion books in various departments.

Credits: IADS (Dr Christopher Knee)

IADS Exclusive - Sustainability series #4: Amfori

IADS Exclusive - Sustainability series #4: Amfori

What: A global non-profit business association promoting open and sustainable trade.

Why is it important: The association empowers members with a network of producers and suppliers that are aware of the concerns department stores face and can simplify retail supply chain operations through audit standards.

In today’s world, organizations are held accountable not only by the government but even more so by consumers. It is becoming necessary for businesses, especially the fashion industry, to become transparent about the impacts that their supply chain has on workers and the environment and that they take responsibility for instances that happen in each part of the operation. Many businesses have turned to audits such as Amfori to create a channel of ethical transparency for all stakeholders.

What it is

Amfori was founded in 1977 as the Foreign Trade Association (FTA) to represent the foreign trade interests of European retailers, brands, and importers to European and international institutions.

Over the last 40 years, the company has rebranded and expanded its scope to social and environmental responsibilities to assure that goods sourced worldwide are coming from supply chains that respect workers and the environment. Amfori provides companies with a system to improve their social compliance within their supply chain on a global scale.

Amfori membership has grown in the past decade from 23 members in 2004 to over 2,451 in 2020. It has a combined annual turnover of over $1.5 trillion, making Amfori the largest social compliance initiative.

Vision 2030

In 2017, when Amfori celebrated its 40th anniversary, the association launched Vision 2030 which is a strategy to address the challenges that technological advancements and changes in political thinking could bring for sustainable trade. Vision 2030 is centered around 5 objectives: build the organization to be fit for the future, support the members through insight, expertise, and influence, inspire action around the world, grow high-performing people to become the leaders of a sustainable tomorrow, and prosper by contributing to the SDGs (Sustainable Development Goals) to increase human prosperity for all.

Through the guidance of the United Nations’ SDGs, the association hopes to make a social, environmental, and economic impact. Amfori promotes compliance and improvements within global supply chains leading to important discussions about social issues. The organization supports companies by increasing the supply chain visibility which helps address pressing environmental changes. Amfori’s objectives protect and improve international trade interests which is crucial to sustainable development, inclusive economic growth, and human prosperity.

How it works

The association offers three different products: Amfori BSCI, Amfori BEPI, and Amfori Advocacy. Through these product lines, Amfori hopes to enable businesses to succeed by providing world-class services and tools that allow them to trade openly and sustainably while helping shape the right policy environment for open and sustainable trade to flourish.

The Amfori BSCI (Business Social Compliance Initiative) platform provides a single place for all supply chain performance information which helps members make decisions about suppliers and measure improvements. It aims to improve social performance in the increasingly complex global supply chains. An audit to ensure compliance involves a thorough on-site assessment of supplier facilities by professional social auditors which are executed every two years. Though Amfori BSCI does not provide a formal certificate, the factory profiles and audit results are kept in a database that members can use to make decisions on which suppliers to use.

The Amfori BEPI (Business Environmental Performance Initiative) platform provides data on environmental performance in supplying factories and farms worldwide. BEPI provides a practical framework that can support all product sectors in all countries to reduce their environmental impact, business risks, and costs through improved environmental practices. While no certification is awarded, the BEPI process is designed to give members a fair representation of their international supply chain performance and allow producers to improve their performance. With the help of a professional environmental consultant, the producer is coached on the production areas that need to be improved.

The Amfori Advocacy offering helps members shape a political, legal, and social landscape where they can drive equitable trade and advance human prosperity. The advocacy team works with a range of stakeholders to ensure trade is responsible, sustainable, and benefits everyone involved. Advocacy helps members satisfy customers’ expectations while helping them maintain their competitive edge. The service provides members with a network of local representatives, country-specific information, political, social, and legal insights, and expertise to be able to make informed decisions.

Why is it important

Amfori provides department stores with a database of producers and suppliers that accept and assume principles of ethical commitment. When the supply chain for retail is coming from various countries with differing labor laws and operational regulations, it can be hard to perform the proper due diligence of each region while meeting the demands of the consumer. Through Amfori, department stores can feel at ease by choosing to partner with providers that are connected through the same responsible vision towards the future of retail.

Amfori is attempting to address the chaos and unnecessary duplication of auditing efforts by providing a common code of conduct and a single implementation system. This will enable all companies that source products from various regions to collectively solve complex labor problems in the retail supply chain. As Amfori compliance is recognized by all participants, manufacturers do not need to repeat the inspection thus reducing workload and management overhead.

Amfori has a better understanding of the issues that department stores face and has even backed the Fashion Industry Charter Communique. This initiative is focused on driving the fashion industry to net-zero Greenhouse Gas Emissions by 2050. The Communique calls for cross-sector collaboration within the fashion industry and focuses on the role policy environments play in accelerating climate action both in fashion production and consumption countries. Members recognize that current business models are insufficient and support the adoption of systematic changes to achieve the goals of the Paris Agreement. The members are trying to make the fashion industry a model for other sectors to follow. Any company that is professionally engaged in the fashion sector can sign the letter of commitment to join in on the initiative.

Limits and Criticism

In September 2019, the Clean Clothes Campaign criticized the social audit industry in a report alleging that it prioritizes brands’ reputations and profits and fails to meet its mission of protecting workers’ safety and improving working conditions in global garment supply chains. The organization claims that there were auditing failures in the deadly 2012 Ali Enterprises factory fire in Pakistan and the 2013 Rana Plaza factory collapse in Bangladesh. In both situations, there were Amfori audits done by the testing service provider, TÜV Rheinland, that deemed the facilities safe just weeks or months before the incidents. In the report, German retailer, Adler, confirms that Amfori BSCI members rely on the database to make supplier decisions and that Adler had accepted products from a factory in Rana Plaza because the factory was able to prove BSCI compliance.

Though TÜV Rheinland remains on the approved list of Amfori’s audit vendors, in Amfori’s 2020 Year in Review report, they announced the Audit Assurance Programme as a priority in 2021, which is meant to implement trust and quality back into the audits.

The best choice for European department stores

Amfori’s members come from 45 different countries with 89% of the members having their headquarters in Europe. The majority of the members are importers which represent 66% of the members, with brands and retailers following at 19% and 11% respectively. The two major sectors of members are general merchandising and garment and textiles. Therefore, Amfori can benefit department stores in Europe by sharing best practices and market knowledge around sustainability and social responsibility.

Amfori has also helped members navigate the global pandemic by releasing a report called “Responsible Purchasing Practices in times of COVID-19” to help guide its members through the tough situations that lie ahead.

Though the Amfori audit may not replace other certifications, it reduces the chaos associated with sustainability standards by connecting the garment industry. Through its various members, initiatives, and involvement, Amfori might be the best option for European department stores to focus their efforts concerning sustainability standards.

Credits: IADS (Mary Jane Shea)

IADS Exclusive - Business Case #5: Macy’s & Nordstrom abandon new concepts

IADS Exclusive - Business Case #5: Macy’s & Nordstrom abandon new concepts

Two significant US department store groups, Macy’s and Nordstrom, acquired small innovative formats, respectively Story and Jeffrey, and abandoned them in 2020, perhaps not entirely because of the Covid pandemic. What explains their failure to use these opportunities, and what lessons can be learnt by department stores searching for a new lease of life?

Even before the pandemic,

r6646_9_washington_post_macys_is_closing_125_stores_and_laying...pdf

involving substantial cost savings, the closing of over 125 stores and the cutting of up to 4000 jobs. CEO Jeff Genette said: “We know we will be a smaller company in the foreseeable future”. These measures went hand in hand with a new strategy called “new North Star” meant to turn around the country’s largest department store group. Among those leaving the company since the pandemic is

r6643_9_retail_dive_story_founder_rachel_shechtman_to_leave_macy_s___retail_dive.pdf

, who arrived when

r6641_9_retail_dive_is_macy_s_about_to_reinvent_the_department_store____retail_dive.pdf

in 2018 and created a post just for her called “brand experience officer”. At the time the move seemed to usher in an era of reinvention for the department store group, together with the investment in start-up b8ta.

The same year 2020 saw

r6642_9_retail_dive_nordstrom_closing_its_three_jeffrey_specialty_apparel_stores.pdf

, which Nordstrom had acquired in 2005. Jeffrey’s success, particularly in the Meatpacking District which contributed in no small part to the gentrification of that area of Manhattan, was seen at the time as an effort on the part of the upscale department store to renew itself and help modernise its fashion appeal. After the Nordstrom acquisition, Kalinsky worked in a variety of executive roles at the department store company while still running Jeffrey in New York, Atlanta and Palo Alto. It has now been announced that the stand-alone stores would also close (as well as 16 full-line department stores).

Two examples of well-established department stores acquiring successful and innovative concepts, as well as acquiring the founders’ expertise, in an avowed effort to rejuvenate the department store concept, then abandoning the project (admittedly in a covid year) with little to show for it. Why does it appear to be so difficult for a traditional department store to learn from a radically different but very successful retail format?

Who is Jeffrey?

The Nordstrom connection with Jeffrey is perhaps the least surprising of the two: indeed, department stores, especially higher-end ones, are expected to offer curated assortments, the latest in new fashion brands. This was exactly what Jeffrey Kalinsky had built his reputation on for many years before Nordstrom got interested. In a similar vein, the Maria Luisa space in the Printemps department store in Paris was intended to offer customers the same fashion know-how and selection that the boutique founded in the 1980s became known for. If viewed as a shop-in-shop offering a specific assortment, then Jeffrey and Maria Luisa could conceivably exist simply as another outlet for the concept alongside the boutiques. An example of such a strategy would be that of 10 Corso Como which was looking for expansion possibilities and trialled openings in department stores such as SKP or Lotte and is able to retain independence and flexibility.

However, this was clearly not the case with Jeffrey at Nordstrom since he joined the company and served in several roles, ostensibly to train or influence existing buyers to up the game of the company as a whole in terms of brands and assortment at the very least. He maintained his credibility not by opening a concept in the store but by continuing to operate the Jeffrey stores separately.

r6642_9_retail_dive_nordstrom_closing_its_three_jeffrey_specialty_apparel_stores.pdf

. For several years, this category has been underperforming in department stores. It was perhaps to strengthen this category that the store took on the Jeffrey fashion icon. It should be remembered also that Nordstrom had been planning to open in New York for some time, where Jeffrey had made such a splash among the fashionistas. The Jeffrey image could do no harm to the Nordstrom brand. It was the apparel offer in the full-line stores which needed attention, since the Nordstrom Rack outlets have been performing better.

A good Story

The Story connection with Macy’s is more recent since it was acquired in 2018. Story was a single store operation which attracted much media attention since its launch in 2011. The founder was frequently invited to explain the concept, a constantly changing store and offer according to the “story” of the moment like a gallery whose aim is just as much to sell experience as it is to sell products. The narrative-driven retail concept shop is intended to bring to life an editorial approach around themes such as colour, for example.

Here again, the image advantage derived from this acquisition by Macy’s placed the latter firmly in the camp of department stores seeking to “reinvent” themselves. It also invited founder Rachel Shechtman to join Macy’s as “brand experience officer” signalling its commitment to bringing a fresh perspective to the department store and to retail. Macy’s had been in need of a fresh approach for some time since its uniqueness had been diluted and indeed drowned by its size and standardised model. The promise of Story was expertise in experience; collaboration with a number of other brands; working with small businesses and authentic products with special stories; and running a dynamic event schedule. All more like a magazine editorial role than a classic retailer. Once again, this was touted not as a shop-in-shop, but as a starting point for a major overhaul.

Goodbye Jeffrey, it’s the end of the Story

Whether the formats in question were appropriate to carry the future hopes of large department store groups is, of course, debatable. What is clear is that both department stores were probably seduced by the dynamic impact Jeffrey and Story were having on customers, the media and indeed consultants and retail commentators. Small concepts, linked to strong personalities will behave in certain ways: they will be agile and flexible, they will have minimal organisation structure, they will be subject to the whim and creativity of the founders, they will test and make mistakes, and sometimes they will be totally unsuitable for growth.

Acquiring the founder with the concept does not solve the problem. In fact, the chance of a new concept founder fitting into a large classic organisation structure is arguably quite low. Start-up founders hired by department stores have often left, frustrated at the immobility and slowness of the department stores’ structure as well as their incapacity to cut across the internal siloes.

Scaling is also a significant obstacle to success. In both cases (Story operated one store, Jeffrey three) the shift from operating on a small scale, selecting the assortment or the theme, signing collaborations and managing marketing, to making a difference in very large structures, is an almost insurmountable challenge, unless the expected impact is very clearly articulated and organised. The influence of

r6645_9_vogue_another_retail_goodbye__jeffrey_stores_close_permanently___vogue.pdf

was diffuse, and

https://www.iads.org/files/pmedia/public/r6647_9_wwd_rachel_shechtman_out_at_macys__wwd.pdf

r6647_9_wwd_rachel_shechtman_out_at_macys__wwd.pdf

in large classical department stores.

To buy or not to buy…

As was discussed in the IADS Exclusive: Dealing with Disruption, a radical innovation in any business requires commitment and investment, sometimes at the expense of the established business. The onboarding of Jeffrey resulted apparently in no more than a star consultant let loose in the buying department; the ideals of Story were transformed into rather inadequate and sad gift shops. According to Doug Stephens who apparently had advised Macy’s to acquire Story, “Macy's squandered a golden opportunity to reinvent — not just the Macy's experience but the entire revenue model of department stores generally… but instead of taking a whole Macy's store and moving it over to the Story business model ... they chose instead to treat it as a bauble, a fanciful little concept inside the same horribly boring Macy's store”. Strong words indeed. It is certainly the case that

https://www.iads.org/files/pmedia/public/r6636_9_bof_macys_acquires_story.pdf

r6636_9_bof_macys_acquires_story.pdf

with these acquisitions but as one commentator has written, was it perhaps “

r6637_9_forbes_macy_s_acquires_story__game_changer_or_much_ado_about_nothing_.pdf

”.

These two cases raise an important question: how should department stores think about their revival and innovation in general? Acquisitions of small concepts or start-ups may help with the importing of skills and know-how. There is no doubt for example that the acquisition of the UK arm of buy.com helped John Lewis develop its own online business. But this was approached as a tool for the job and within a year, buy.com had been disbanded and totally absorbed into the mainstream business. Almost the same thing happened at Walmart when it acquired jet.com in 2016 for over $3bn and folded it into walmart.com to help it compete with Amazon. Current online Walmart development would appear to confirm the success of that move. On the other hand, with its acquisition of Bonobos, it was clear that Walmart was buying a brand alongside many others (Bonobos founder who joined Walmart has coincidentally left the company in 2020).

Department stores are not bad at innovation as the small Bloomies format or the Nordstrom Local shops testify. Even acquisitions can benefit a department store business as the

r6639_9_forbes_nordstrom_will_bring_trunk_club_to_stor...pdf

now being moved into Nordstrom stores illustrates. But this has not been taken on with the hope of transforming the business model of the company. For the moment, the two stores remain much as they were with

r6649_9_the_motley_fool_where_will_macy_s_be_in_5_years____the_motley_fool.pdf

probably assured after yet more cost savings, while

https://www.iads.org/files/pmedia/public/r6644_9_the_motley_fool_nordstrom_inventory.pdf

r6644_9_the_motley_fool_nordstrom_inventory.pdf

and relying increasingly on its off-price chain.

Perhaps with department stores, business model innovation or new formats need to be developed in-house. Otherwise, an acquisition should serve as a tool for a specific task.

Credits: IADS (Dr Christopher Knee)

IADS Exclusive - Business case #4: Debenhams and Topshop buyouts

IADS Exclusive - Business case #4: Debenhams and Topshop buyouts

Who doesn’t remember a trip to Oxford Street to check on the competition or just feel the consumption frenzy? Well, the Oxford Street and the high street we used to know will not be the same anymore. Debenhams and Topshop collapses are a brutal reminder of department stores and clothing chains struggle, private equity mismanagement, lack of strategy and then Covid-19 dramatically speeding up the process. Even though the brick-and-mortar shutdowns trend is global and rampant, we might find ourselves at a turning point, especially in the United Kingdom, with Boohoo and Asos buying bits of Debenhams and Topshop.

What has happened to the famous British retailers? What are Boohoo and Asos’s buying strategies aiming at? Are Debenhams and Topshop buyouts specific business cases? Is there a new pattern to be observed?

The high street fiasco

Debenhams and Topshop have been sharing history for a long time. They were both part of the Burton Group in the 1980s and 1990s. Their economic issues go back to before Covid-19 hit the world and the UK last year and they are collapsing at the exact same time.

Founded in 1778, Debenhams was once one of the largest retailers in the UK.

r6628_9_1-debenhams_the_rise_and_fall_of_a_british_retail_institution_the_guardian.pdf

when a private equity consortium (CVC, Texas Pacific and Merrill Lynch) acquired the department store for GBP 600 million. Three years later, the company returned to the stock market for GBP 1,2 billion. The consortium also took out more than GBP 1 billion from selling the company’s real estate and leasing it back. At that point, Debenhams was loaded with heavy debt and tied to very expensive leases. It was too late to remodel the strategy and there was not enough money left for investments such as the much-needed digital ones. Even recruiting Sergio Bucher coming from Amazon was no help. Reducing the store portfolio could also have been a smart, if not a lifesaving move: but while online shopping was expanding, Debenhams was still opening stores in 2017. Moving forward, it went from bad to worse until 1 December 2020, when Debenhams went into administration.

What about Topshop? When Debenhams exited the Burton Group, the remaining part of it became Arcadia Group and was acquired by Sir Philip Green’s family. Arcadia Group’s brand portfolio (Topshop, Topman, Miss Selfridge, HIIT, Dorothy Perkins, Evans and Burton) used to be led by Topshop for more than a decade, with years of thriving business, top models and billion dividends. At that time, there were still plenty of seats left at the digital table, but

r6629_9_2-the_rise_and_fall_of_philip_greens_arcadia_retail_empire_financial_times.pdf

to force Topshop into the online-shopping era and failed to position the brand as one of its leaders. The Nordstrom deal was also probably too little to allow Topshop to really break into the US market. In the meantime, Topshop product offer diluted as competition became fierce, with both brick-and-mortar retailers and online players. In 2018, Sir Philip was also caught up in abusive sexual behaviour scandals, adding more mistrust towards him. Finally, on 30 November 2020, the group entered administration, just 24 hours before Debenhams did.

Get a move on

Going deeper into Boohoo and Asos’ moves, what do we know so far? They are both wunderkind British-born e-tailers chasing Millennials and Gen Z consumers for more than 15 years. Boohoo was first to acquire companies with Karen Millen and Coast in August 2019, then with Oasis and Warehouse in June 2020. In January 2021,

r6630_9_3-why_digital_fashion_companies_are_buying_up_tired_brands_bof.pdf

for GBP 55 million (USD 75.4 million): website, private label brands and customer data. As of now, the website still attracts 300 million visitors a year. Boohoo also bought four fashion private labels that are appealing to the older generation (Maine, Mantaray, Principles and Faith). Thanks to Debenhams’ strong position on the cosmetics and perfume market, Boohoo is acquiring the 1.4 million Beauty Club members. The deal does not include the 130 brick-and-mortar stores and the 12 000 jobs involved. Premium locations such as Oxford Street, the ones that were fought for not that long ago, are not considered. A few days later, Boohoo acquired Burton, Dorothy Perkins and Wallis, all “mature brands” and the last remains of Arcadia Group. It’s a GBP 25.2 million (USD 34.7 million) deal and, once more, it does not include the 216 stores and the countless jobs involved. While only 10% of Debenhams’ customers are also buying from Boohoo, this demonstrates a strong will to grow outside of its existing 20-something business and to target new segments of the market such as cosmetics or older male and female clientele. The company said it’s a “significant opportunity to grow Boohoo's market share across a broader demographic”.

Asos, on a larger scale than Boohoo, aims to become the world’s number one destination for young fashion addicts thanks to its huge, varied and inclusive product offer. The company’s latest move will certainly serve that mission and will strengthen its strategy. As an existing wholesale partner to the brands,

r6631_9_4-asos_to_buy_topshop_and_other_arcadia_brands_for_265m_financial_times.pdf

and sister brands Topman, Miss Selfridge and HIIT for GBP 295 million (USD 411 million). In 2020, Asos increased its sales by 19%, growing from GBP 2.7 billion to GBP 3.17 billion and could count on 22.2 million active customers. Asos said in a statement: “The Board believes this would represent a compelling opportunity to acquire strong brands that resonate well with its customer base.” An Exane BNP Paribas survey states that 40% of Topshop’s shoppers are also buying from Asos. Like Boohoo, Asos does not include Topshop’s 168 stores and 13 000 retail jobs in the deal.

While Boohoo is moving into markets outside of its current core business, Asos is strengthening its position in order to take the lead in its segment. While these are different strategies, both companies will grow their online footprint in the very near future.

Is it to say that Topshop or Debenhams stores will all permanently disappear? It remains to be seen, but one can guess that these digital brands in the making will find themselves in need of a physical approach to the business at some point (as other e-tailers have done). Whether it’s to have a brand billboard, a service touchpoint, a community hub or offer immersive entertainment to customers, stores should remain a key part of the business. Asos’ CEO Nick Beighton hasn’t ruled out the idea of taking over Topshop’s Oxford Street crown jewel “if it becomes financially attractive and we can find a partner to work with on that, never say never”.

Are we all British?

Unfortunately, Brexit will have a major impact on such decisions. What will be the point of running stores when visitors from abroad might not consider UK as a shopping destination any longer? In fact, there is no more tax refund for foreign tourists from 1 January 2021. In 2019, they spent GBP 3 billion on fashion and luxury goods in the UK. “We are now the only country in Europe offering no VAT rebate, so why would tourists not go to Paris instead?” says Paul Barnes, the CEO of Association of International Retail.

Going further, is there a specific British pattern to be observed? What makes Debenhams and Arcadia bankruptcies and acquisitions specific? While the European economy was declining, it was no secret there were too many department stores and clothing chain options on the British high street. Besides and more importantly, British online consumption was increasing rapidly, thanks to (among others) Asos and Boohoo. According to an Office for National Statistics study, British online monthly consumption went from GBP 854 million in January 2016 to GBP 1.386 billion in January 2020. For the month of November 2020, just when both Debenhams and Arcadia were going into administration, ecommerce hit a record GBP 3.250 billion turnover, accounting for 36% of British total retail sales for the month. In this turmoil, winners are the ecommerce moguls for sure, but what is unprecedented is to witness their breaking and entering the British department stores scene.

While British retail and department stores might suffer more than others in the near future, we assume that the ones that are (and will be) surviving through numerous crises, are the ones adjusting to online demand, streamlining their operations and adapting their store portfolio.

One of the many learnings in Debenhams and Topshop’s disasters is also about differentiation, hence branding. Both -as brands- were once magnets to customers. They were attracting them thanks to the values, difference, uniqueness or zeitgeist they were claiming to carry. Whatever you name it, it has been lost at some point of the journey.

The branding question is more than ever a critical question for department stores. It will infuse all of the challenges ahead whether it’s about enhancing and transforming customer experience, growing digital capabilities or providing products appealing to an ever-evolving shopper.

Credits: IADS (Christine Montard)

IADS Exclusive - Remote working: what can department stores learn from the great RW experiment?

IADS Exclusive - Remote working: what can department stores learn from the great RW experiment?

Companies have been exploring the possibilities of remote working for many years. In fact, remote work has even, in some cases, been implemented then abandoned. Department stores have been forced into remote work by the current pandemic. Or at least some of the department store functions have been. Is this likely to become a permanent feature of our retail businesses? If so, what might it look like in more detail? Remote working has raised major issues for HR departments, as well as for management. If the practice becomes widespread, remote work will also have implications for city life and consumer spending more broadly, and therefore on department store customers.

A breath of clean air blowing through the cities

The silence and clean air of recent lockdowns in major cities have been partly due to a significant number of employees working from home.

With the coming of a (hopefully) viable vaccine, is it likely that remote work will continue? According to McKinsey international surveys of different jobs, some 20% of the workforce could work as effectively from home as from the office, 3 to 5 days a week. This would mean

https://www.iads.org/files/pmedia/public/r6491_9_mckinsey_gi-whats-next-for-remote-work-v3.pdf

r6491_9_mckinsey_gi-whats-next-for-remote-work-v3.pdf

. Research from S&P Global Market Intelligence claims that 80% of organisations have implemented or expanded work from home policies and 67% expected these measures to stay in place permanently or for the long term (Candezent, Covid-19 and the retail industry, December 2020).

The effect on urban economics, transport, and consumer spending would be significant. Before Covid, around 5-7% of the workforce worked from home. A shift to 20% would, for example, lower the number of commuters with consequences for transport, petrol/gas sales, auto sales, restaurants and retail. Figures for office vacancy in the US would shift from 16.8% currently to 19.4% in 2021 and 20.2% in 2022. As an example, the sports retailer REI has already decided to sell its new headquarters in Washington before even moving in. It has decided instead

r6571_9_washington_post_rei_plans_sale_of_brand-new_campus_as_i...pdf

across Seattle. (Washington Post) Some argue that

r6484_9_the_atlantic_the_workforce_is_about_to_change_dramatically.pdf

on politics also.

The battle for the office

There are two extreme views of office work:

a) It is a place of pressure, constant interruptions, sometimes harassment, and often low productivity; against which home working is seen as autonomous, happy and in many cases more productive.

b) The office is a place of human contact, creativity, cooperation, empathy and an equaliser. Home working in contrast is an unwelcome and unmanageable merger of public and private, to the detriment of both, added to which it has none of the facilities which make office work efficient.

Some companies have tried and rejected distance working. For example, Yahoo abandoned it in 2013, citing the damage to company culture. IBM abandoned it the same year. Facebook has recently signed a new lease on a big office in Manhattan; and Bloomberg is reportedly offering an extra £ 55 a day to get its workers back to its building in London.

On the other hand, like REI mentioned above, Pinterest has paid out $ 90 m to end a new lease obligation on office space in San Francisco to create "a more distributed workforce". (see The Economist articles:

r6494_9_the_economist_the_future_of_the_office_-_covid-19_has...pdf

and

r6495_9_the_economist_the_future_of_work_-_is_the_office_finished____leaders.pdf

).

The classic office is pretty much a relic of the 19th Century, designed for control and surveillance, and dominated by the clock and the time employees sell to their companies. Changes in the office have broadly been limited to a choice between separate offices or open space. And the choice has been largely dictated by economic and cost factors rather than by efficiency or effectiveness criteria. (The same can be said of "hot desking".) Whatever happens, it is clear that the "office" as it exists today is in need of serious reform; and this means more than just ping pong tables, bean bags and unlimited fruit juice. Arguably, even ApplePark and Googleplex, which are used to lure talent to their office worlds, are merely more sophisticated versions of the same thing (see for example, the novel The Circle by Dave Eggers, and the movie). The Vitra CEO illustrated this view at a conference attended by IADS last September, by opposing cost & control-focused companies (where the work environment is not that important) to creativity-focused companies (where she sees an opportunity for her design company to improve the workspace).

The great divide at work

r6485_9_mit_four_principles_to_ensure_hybrid_work_is_productive_work.pdf

(mixing both remote work and physical presence)**. It is the case not only that some industries are more suited to remote work than others, or that some companies have decided one way or another for strategic reasons, but that different functions may be able to adopt distant practices more easily than others within the same industry or company.

Amid a great deal of uncertainty and differences of opinion, it remains that within retail, and department stores in particular, there is clearly a face-to-face function involved in selling which has to remain mostly physical (even though an increasing number of sales jobs are being advertised as remote – see <https://www.flexjobs.com/jobs/telecommuting-jobs-at-neiman_marcus>) or Container Store (repeatedly voted one of the "best places to work"). The fact that many surveys consider retail to be one of the least likely industries to shift to remote work is undoubtedly because the figures are skewed by smaller independent retailers. Chains and indeed department stores

r6493_9_facttank_working_from_home_was_mostly_an_option_...pdf

.

Other jobs in retail that require physical presence may include fulfilment, and warehouse tasks. It was suggested by the last IADS Academy, that the finance function in department stores is probably the one that could most easily be carried out at a distance. In fact, according to

https://www.iads.org/files/pmedia/public/r6491_9_mckinsey_gi-whats-next-for-remote-work-v3.pdf

r6491_9_mckinsey_gi-whats-next-for-remote-work-v3.pdf

amenable to distance working, retail would include elements at both extremes such as handling data at the remote end of the continuum, and handling goods at the other end where physical presence is necessary. The

https://www.iads.org/files/pmedia/public/r6570_9_retail_week_retail_and_future_of_work_report_.pdf

r6570_9_retail_week_retail_and_future_of_work_report_.pdf

has been highlighted by the current pandemic. And the future of this group