Articles & Reports

6 ways to reduce DEI programs’ legal risk

6 ways to reduce DEI programs’ legal risk

What: Companies are changing DEI language, structure, and practices to address new legal challenges while maintaining inclusive workplaces in the US.

Why it is important: Adapting DEI programs in response to legal pressures ensures companies can continue to support diverse workplaces within the boundaries of US law.

As the legal environment for diversity, equity, and inclusion programs in the US becomes more complex, organizations are making significant adjustments to reduce litigation risk while preserving inclusive cultures. Recent changes include broadening access to employee resource groups, reframing DEI-related training to focus on universally accepted topics like antiharassment and antidiscrimination, and ensuring that development and hiring opportunities are merit-based and open to all. Companies are also moving away from demographic quotas and diverse slate mandates, instead adopting sourcing strategies that cast wider nets and using objective interview processes. Regular privileged audits and ongoing evaluation of DEI programs are now considered best practices, helping organizations identify and address potential legal vulnerabilities. These shifts reflect a broader trend of adapting language and structure to align with evolving federal guidance and court decisions, ensuring that DEI efforts remain both effective and compliant. By focusing on fairness, transparency, and legal soundness, US companies aim to maintain their commitment to inclusion in a challenging regulatory landscape.

IADS Notes: The current evolution of DEI strategies in the US reflects a broader industry response to heightened legal and regulatory scrutiny, as detailed by Reuters in January 2026, which reported that intensified federal oversight has led major employers to alter or scale back their DEI initiatives, often with significant operational and financial implications for those failing to adapt. HR Dive’s October 2025 analysis underscores how organizations are reframing DEI language and structures, shifting from explicit references to equity toward broader concepts like inclusion and belonging to better navigate legal risks. This trend is further supported by Time in January 2026, which emphasizes the importance of trust-based leadership and practical, ongoing evaluation to ensure DEI programs remain resilient. ESG Dive’s May 2025 and May 2026 coverage reveals that while most companies intend to preserve DEI efforts, concerns about litigation have nearly doubled, prompting strategic adaptation of program methods and increased use of regular privileged audits. Harvard Business Review in February 2026 and Seramount in January 2026 highlight the move toward universal access and transparency in development and training opportunities, reinforcing the need for measurable outcomes and compliance-driven inclusion. Collectively, these sources confirm that US organizations are prioritizing fairness, transparency, and legal soundness to sustain inclusive workplaces amid a rapidly changing regulatory environmen

Research: traditional marketing doesn’t work on AI shopping agents

Research: traditional marketing doesn’t work on AI shopping agents

What: The rise of AI shopping agents is disrupting established online marketing methods by prioritizing data quality and ratings over classic persuasion cues.

Why it is important: The disruption of classic marketing tactics by AI agents highlights the urgent need for retailers to adapt their digital infrastructure for algorithm-first commerce.

AI shopping agents are rapidly transforming the dynamics of online retail by fundamentally altering how purchase decisions are made. Traditional marketing tactics such as scarcity cues, countdown timers, and strike-through pricing, which have long been effective with human shoppers, are proving largely ineffective or even counterproductive when targeting AI agents. Recent research demonstrates that only product ratings and competitive pricing consistently influence AI-driven choices, while other promotional mechanisms yield inconsistent or negative results depending on the AI model and product category. This shift compels retailers to rethink their approach, treating each AI model as a distinct market segment and focusing on the fundamentals of transparent data and authentic reviews. As AI agents become more prevalent and sophisticated, retailers must invest in dynamic, real-time adaptation and robust testing infrastructures to keep pace with rapidly evolving agent behaviours. The future of retail success will depend on the ability to optimise for algorithmic decision-makers rather than relying on traditional human-centric persuasion.

IADS Notes: The rapid ascent of AI shopping agents is fundamentally altering the retail landscape, as confirmed by multiple recent industry analyses. In April 2026, Liontree highlighted that AI-driven shopping has become mainstream, especially among younger and affluent consumers, shifting the basis of brand visibility from traditional recognition to the quality and transparency of product data. Emerge, also in April 2026, reported an extraordinary 393% surge in AI-driven retail traffic, with agentic shoppers now outspending and outperforming human consumers, underscoring the urgency for retailers to prioritise machine-readable content and AI visibility. Journal du Net’s March 2026 coverage described how agent-based commerce is compelling retailers to overhaul their operational and technological strategies, invest in agent-ready systems, and focus on hyper-personalisation to meet evolving consumer expectations. Inside Retail in November 2025 emphasised that AI-powered agents are transforming e-commerce by automating shopping decisions and making data integrity and real-time information critical for success. Finally, Journal du Net in September 2025 documented how AI agents are now mediating and automating e-commerce transactions, redefining the relationships between brands, retailers, and consumers, and requiring urgent adaptation for machine readability and algorithmic mediation.

Research: traditional marketing doesn’t work on AI shopping agents

Consumers are shaping a new age of optimisation in beauty

Consumers are shaping a new age of optimisation in beauty

What: According to BCG and WWD’s May 2026 findings, beauty’s next wave is defined by digital-savvy optimisers, AI-powered personalisation, and the convergence of aesthetics, wellness, and technology.

Why it is important: This shift highlights how digital innovation, inclusivity, and wellness are now central to beauty retail’s competitiveness and consumer loyalty.

The May 2026 BCG and WWD report identifies a new era in beauty, driven by the rise of “optimiser” consumers who blend traditional routines with aesthetic procedures, wellness, and longevity treatments. These consumers are highly informed, results-oriented, and increasingly reliant on AI for product research and personalised routines, with 75% using AI and a quarter making it their primary source. The optimiser segment, though only 6% of US adults, is responsible for significant incremental spending, signalling a broader market opportunity if this group expands. The definition of beauty is evolving, with mental and physical well-being now as important as appearance, prompting brands to rethink engagement and product development. Trust in beauty discovery is shifting away from social media toward efficacy, scientific validation, and medical professionals, while inclusivity and authenticity are becoming essential for brand loyalty. As consumers layer solutions across categories, brands and retailers must adapt to meet the demand for personalisation, transparency, and holistic wellbeing, positioning themselves for growth in a rapidly changing landscape.

IADS Notes: The findings of the BCG and WWD report are reinforced by recent industry sources. In May 2026, BCG and WWD highlighted the optimiser segment’s impact on market structure and spending, while The Economist in January 2026 detailed the expansion of beauty into wellness and medical-grade services. The centrality of AI in beauty routines is underscored by BCG in July 2025 and Forbes in April 2026, with Sephora’s March 2026 launch of an AI-powered app within ChatGPT exemplifying the sector’s digital transformation. Monocle in December 2025 and Retail News in September 2025 further illustrate the normalisation of cosmetic procedures and the rise of experiential, service-driven retail. The evolving landscape of trust, inclusivity, and efficacy is shaping brand strategies, compelling the industry to prioritise digital innovation and holistic consumer engagement.

Consumers are shaping a new age of optimisation in beauty - Article

Consumers are shaping a new age of optimisation in beauty - Full report

AI isn’t failing. Your organisation is absorbing it wrong.

AI isn’t failing. Your organisation is absorbing it wrong.

What: The uneven absorption of AI across organisations highlights persistent gaps between technological investment and organisational readiness.

Why it is important: Persistent gaps between investment and readiness signal that technological change alone is insufficient without cultural and managerial adaptation.

The article examines why organisations are struggling to translate rapid AI adoption into measurable productivity gains, despite soaring global investment and mounting pressure to demonstrate progress. While AI can accelerate individual tasks, the anticipated return on investment remains elusive because organisations often overlook the need to redesign workflows and human systems. The author argues that the real challenge lies not in AI itself, but in the way organisations absorb and integrate it—particularly when it comes to developing leadership pipelines, equipping managers, and maintaining trust. Automation risks eroding early-career learning opportunities, which are crucial for building future leaders, while uneven managerial support and fragile trust further complicate successful transformation. Employees’ scepticism and inconsistent guidance from managers can stall adoption and create execution risks. The article calls for a more deliberate approach, emphasising the importance of governance, clear decision rights, and intentional sequencing of AI initiatives. Ultimately, the piece argues that sustainable value from AI will emerge only when organisations balance technological innovation with robust human judgment and cultural adaptation.

IADS Notes: The article’s analysis aligns with findings from The Economist (Feb 2026), which reported that most organisations struggle to achieve productivity gains from AI despite significant investment. Harvard Business Review (Mar and Apr 2026) highlights how automation threatens early-career talent development and exposes misalignment between executives and managers, slowing AI’s value realisation. ESG Dive (Dec 2025) documents employee concerns about trust and transparency, while Forbes (Oct 2025) emphasises the necessity of robust governance and workflow redesign to unlock AI’s full potential.

IADS Exclusive: Department Stores Spring windows 2026

IADS Exclusive: Department Stores Spring windows 2026

Spring 2026 is here, and department stores around the world are making their mark. IADS has brought together the season's standout window displays, in-store installations, and visual moments from members and beyond.

DEPARTMENT STORES WINDOWS, IN-STORE INSTALLATIONS, VISUALS & SOCIAL MEDIA SPOTS

CLICK HERE TO SEE THE 2026 SPRING WINDOWS REPORT

Credits: IADS Team

Declining fraud rates don’t mean declining fraud risk

Declining fraud rates don’t mean declining fraud risk

What: Retail payment fraud attack rates have declined, but chargebacks have surged as fraudsters shift to more targeted, sophisticated tactics like account takeover.

Why it is important: The changing fraud landscape demands that retailers recalibrate detection frameworks and prioritise longitudinal risk monitoring to sustain growth and protect brand reputation.

Recent fraud trend data reveals a paradox in retail security: while payment fraud attack rates and manual review volumes have dropped, chargeback rates have climbed sharply, rising 56% year over year. This shift reflects a move from high-volume, opportunistic attacks to more precise, high-value schemes such as account takeover and “good user gone bad” patterns, where fraudsters exploit trusted accounts and stored credentials for greater payoff. Automation and AI have improved operational efficiency, but speed-focused systems may miss these complex, delayed frauds, leading to increased losses and reputational risk. The impact is uneven across business models, with subscription and stored credential platforms facing heightened exposure. As over half of consumers say they would abandon a platform after experiencing fraud, the stakes for customer trust and lifetime value are higher than ever. To stay ahead, retailers must recalibrate their fraud detection frameworks, invest in longitudinal risk monitoring, and balance operational efficiency with robust, customer-centric prevention strategies.

IADS Notes: Recent IADS sources confirm that retail fraud is evolving rapidly, with a marked shift from high-volume, opportunistic attacks to more targeted, sophisticated schemes such as account takeover and “good user gone bad” patterns. The RH-ISAC Intelligence Trends Summary (Q4 2025) and the March 2026 CISO Benchmark Report both highlight the convergence of cybersecurity and fraud prevention as a defining challenge for the sector, with retailers investing in intelligence sharing, cross-functional collaboration, and integrated security strategies to protect customer trust and business continuity. Forrester’s 2026 payment industry predictions and BCG’s Global Payments Report (September 2025) underscore the rise of agentic AI and real-time payments, which, while improving efficiency, also introduce new fraud vectors and require robust, adaptive risk management. Journal du Net (January 2026) and The Robin Report (April 2026) document the surge in returns fraud and the operational and reputational costs of chargebacks, with leading retailers responding by tightening policies, leveraging AI for risk scoring, and personalizing fraud detection. RH-ISAC’s May 2025 analysis of account takeover incidents and the April 2025 Retail Bulletin report on cyberattacks at major retailers like M&S and Harrods further illustrate the sector’s vulnerability to credential theft and the need for layered defenses, proactive monitoring, and adaptive authentication. Collectively, these sources show that the most resilient retailers are those who move beyond headline fraud metrics, invest in longitudinal risk monitoring, and align operational efficiency with robust, customer-centric fraud prevention to sustain trust and growth in an increasingly digital retail environment.

Is AI going to take retail jobs? Maybe, but not the ones you expect

Is AI going to take retail jobs? Maybe, but not the ones you expect

What: AI-run stores are transforming retail jobs by automating routine tasks while highlighting the continued importance of human skills and customer service.

Why it is important: The rapid pace of AI-driven change in retail underscores the risks of neglecting talent development and the value of human-centric roles.

The emergence of AI-run stores such as Andon Market signals a profound shift in the retail workforce, as automation increasingly takes over routine and repetitive tasks. While these advancements promise greater operational efficiency and productivity, they also raise critical questions about the future of human employment in retail. Entry-level and support roles are particularly vulnerable, with job cuts at major retailers like Amazon and Target illustrating the sector-wide impact of automation. However, the most successful retailers are those that leverage AI to augment rather than replace their workforce, enabling employees to focus on higher-value, customer-facing activities. This transition demands a renewed emphasis on upskilling, adaptability, and the preservation of institutional knowledge, as only a minority of workers currently feel prepared for the changes brought by AI. The evolving landscape highlights the irreplaceable value of human skills in delivering personalised service and maintaining customer relationships, even as technology continues to redefine the boundaries of retail work.

IADS Notes: The rise of AI-run stores reflects a broader industry transformation, as highlighted by Harvard Business Review (March 2026) and BCG (January and September 2026), where automation is fundamentally redesigning retail roles and elevating responsibilities. Forbes (October 2025) documents the impact of automation-driven job cuts at Amazon and Target, while the Stanford Digital Economy Lab (September 2025) emphasises the importance of workforce augmentation over replacement. Despite these advances, only a minority of retail workers feel adequately prepared for AI-driven change, underscoring the urgent need for systematic upskilling and balanced integration of technology and human talent.

Is AI going to take retail jobs? Maybe, but not the ones you expect

The new rules of customer experience in the age of agents

The new rules of customer experience in the age of agents

What: Brands are using AI-driven agents and new store formats to improve customer engagement across all channels.

Why it is important: This shift shows that brands must focus on both digital tools and in-person experiences to meet evolving customer expectations.

The landscape of customer experience is rapidly evolving as brands integrate AI-driven agents and reimagine physical spaces to better engage consumers. With the mainstream adoption of AI-enabled shopping, particularly during the 2025 holiday season, brands are seeing a surge in AI-driven traffic and interactions. Consumers now expect seamless guidance and personalization, whether they are shopping online, in-store, or through social media. Physical stores are being revitalized as experiential destinations, blending digital features such as interactive mirrors and connected devices with traditional in-person service. At the same time, brands are challenged to maintain continuity and trust across every touchpoint, ensuring that customer interactions are remembered and data is handled transparently. The article emphasizes that brands must audit their presence in AI-powered discovery, invest in exclusive content and intuitive tools, and redefine the role of physical locations to provide expert consultation and immersive experiences. Success in this environment depends on a brand’s ability to connect digital and physical journeys, nurture trust, and deliver consistent, personalized engagement that meets the expectations of today’s consumers.

IADS Notes: Recent coverage from The Robin Report and Inside Retail in April 2026 highlights how AI-driven platforms are now central to customer engagement, requiring brands to adapt their strategies for visibility and relevance. Liontree’s April 2026 analysis confirms the growing influence of AI recommendations on consumer behavior, while Harvard Business Review and Forbes in early 2026 document the renewed importance of physical stores as experiential spaces. Journal du Net’s April 2026 report and John Ryan Newstores in December 2025 further illustrate the integration of digital infrastructure and design-driven concepts in physical retail. On the omnichannel front, Journal du Net’s November 2025 and January 2026 articles, along with Incisiv and Talkdesk’s September 2024 study, underscore the ongoing need for seamless, personalized experiences across all channels.

Responsible AI needs more than good intentions

Responsible AI needs more than good intentions

What: Companies are adopting responsible AI policies quickly, but often lack the technical depth and systematic oversight required for trustworthy and compliant AI.

Why it is important: The gap between policy and practice exposes companies to operational, legal, and reputational risks as AI adoption accelerates.

Despite a surge in responsible AI initiatives, most organizations remain at a surface level, prioritizing rapid deployment of basic policies and training over building comprehensive, technically robust frameworks. According to a recent global survey, while 85% of companies have implemented responsible AI programs, only a quarter have achieved full maturity, leaving many vulnerable to errors, biases, and regulatory noncompliance. The pressure to act—driven more by internal boards and customer feedback than by external regulation—often results in a focus on speed rather than substance. This approach can lead to significant risks, especially as generative and agentic AI systems introduce new complexities and unpredictability. Mature responsible AI requires systematic governance, thorough risk assessment, continuous monitoring, and integration of controls throughout the software development lifecycle. Without these elements, organisations risk missing out on the full benefits of AI while exposing themselves to financial, legal, and reputational harm. The article underscores that sustainable success in the AI era depends on moving beyond superficial measures to embed deep, adaptive frameworks that ensure trust, compliance, and resilience.

IADS Notes: Recent findings from RH-ISAC (April 2026) and INSEAD (January 2026) highlight the growing gap between rapid AI adoption and the depth of governance and security needed for resilience. The Economist (September 2025) confirms that only a minority of companies are realising the full benefits of AI, while NRF (May 2026) and Forbes (February and December 2025) detail the increasing regulatory pressures from laws like the EU AI Act and New York’s AI pricing law. RH-ISAC (March 2026) and The Robin Report (August 2025) document the risks of prioritising speed over substance, and Harvard Business Review (April 2026) and IAPP (December 2025) emphasise the need for robust governance and real-time monitoring. BCG and INSEAD (early 2026) further point to the importance of board-level accountability and leadership upskilling for effective AI oversight.

The “health hub economy”: new retail opportunities

The “health hub economy”: new retail opportunities

What: The “health hub economy” is emerging as a cross-sector ecosystem where platforms like Strava connect fitness, retail, wellness, insurance, and community, creating new opportunities for engagement and commerce.

Why it is important: As health and wellness become central to consumer identity, brands that innovate across categories and build connected ecosystems will lead in engagement, differentiation, and long-term growth.

The health hub economy is reshaping the landscape of retail and lifestyle by integrating fitness, wellness, technology, and community into a seamless, data-driven ecosystem. Platforms like Strava have evolved from simple activity trackers into central hubs where effort becomes identity, connecting users with brands, retailers, insurance, and even pet care. Gamification, social connectivity, and data-sharing are driving new forms of engagement, loyalty, and commerce, while the rise of wellness clubs, experiential gyms, and holistic “third spaces” reflects a broader shift toward immersive, community-driven experiences. Wearables and health data are now influencing insurance models and product recommendations, while partnerships between fitness, hospitality, and retail brands are creating new touchpoints for customer interaction. As health and wellness become defining aspects of consumer identity, brands that build connected, cross-sector ecosystems are best positioned to capture loyalty, differentiate their offerings, and drive sustainable growth in an increasingly post-sector world.

IADS Notes: BCG’s “Walk, lounge, sweat: How the generations are redefining activewear” (September 2025) highlights how generational shifts, especially Gen Z’s demand for personalization and digital-first journeys, are reshaping the activewear and wellness sectors, driving brands toward more agile, community-driven strategies. BoF in October 2025 documents the rapid expansion of wellness members clubs as luxury “third spaces,” blending social, fitness, and hospitality experiences for affluent urban consumers and signaling a broader shift in luxury retail toward experiential, community-driven platforms. Drapers in April 2026 details Gymshark’s launch of its first gym in Miami, reflecting the trend of digital-native brands expanding into experiential and physical spaces to deepen community engagement and brand immersion. WWD in May 2026 reports on Harvey Nichols’ wellness floor, exemplifying the integration of wellness, fitness, and holistic health into the luxury department store model, with leading retailers investing in experiential, service-driven hubs to drive footfall and differentiation. Inside Retail in September 2025 underscores how brands are investing in retreats, resorts, and residences to create holistic lifestyle platforms that blend retail, wellness, and community, setting new standards for customer experience and engagement. Collectively, these sources illustrate that the health hub economy is driving a convergence of retail, wellness, fitness, and community, with brands leveraging data, technology, and cross-sector partnerships to create immersive, lifestyle-driven ecosystems that capture a greater share of customer engagement and discretionary spend.

Will insurance protect your company in times of war?

Will insurance protect your company in times of war?

What: Insurance policies often exclude coverage for losses caused by war, leaving retail companies financially exposed during conflicts.

Why it is important: Understanding insurance gaps during wartime is vital for retailers to safeguard financial stability and adapt to the realities of global instability.

Retailers are increasingly vulnerable to the financial fallout of geopolitical conflicts, as most insurance policies exclude coverage for losses resulting from acts of war. This exclusion leaves companies exposed to significant risks, especially as recent conflicts in the Middle East have disrupted global supply chains, driven up costs, and forced store closures. The limitations of traditional insurance have become starkly apparent, prompting retailers to reassess their risk management frameworks and contingency planning. Without adequate coverage, companies must rely on robust scenario planning, agile leadership, and transparent communication to navigate operational challenges and maintain business continuity. The evolving landscape demands that retailers not only understand the scope of their insurance but also proactively address gaps through strategic resilience measures. As global instability persists, the ability to anticipate and mitigate uninsured losses is essential for protecting both financial health and long-term viability in the retail sector.

IADS Notes: The ongoing conflict in the Middle East has exposed the acute vulnerability of the retail sector to geopolitical shocks, as highlighted by Inside Retail and The Robin Report in March 2026. Retailers have faced unprecedented disruptions to energy and food supply chains, resulting in soaring costs, inventory shortages, and inflationary pressures that erode consumer purchasing power. The Iran conflict, in particular, has forced companies to rapidly adapt their sourcing and logistics strategies, close stores, and implement robust contingency planning to maintain operational continuity. Forbes (March 2026) underscores how these compounding crises have intensified the need for scenario planning and risk management, while Inside Retail emphasises the importance of agile leadership and transparent communication in navigating such volatility. Against this backdrop, the limitations of insurance coverage during wartime, as explored by Harvard Business Review in May 2026, reveal significant gaps in financial protection for retailers, making strategic risk assessment and resilience planning more critical than ever.

IADS Exclusive – DEI at a crossroads: US retail trajectory since Trump’s Executive Order

IADS Exclusive – DEI at a crossroads: US retail trajectory since Trump’s Executive Order

This is the second article in IADS's series expanding on themes from the January 2026 White Paper DEI at a crossroads in retail. After reviewing the Abercrombie & Fitch business case the focus shifts to the broader US retail landscape.

In 2020, following George Floyd's murder, U.S. retailers launched ambitious DEI programmes and made sweeping public commitments. By early 2026, many had eliminated or scaled back their initiatives, citing changing political realities and legal risks. Target ended its Racial Equity Action and Change initiative. Walmart wound down its racial equity centre. Nike became the first major retailer targeted by federal investigators over its diversity goals.

For U.S. retailers, the stakes extend beyond reputation to legal and financial exposure. Federal contractors face potential liability for maintaining programmes the Trump administration deems "illegal DEI." Yet enforcement remains inconsistent, with conflicting court rulings creating uncertainty about what's permissible. In late April 2026, that uncertainty sharpened. The U.S. Supreme Court's ruling in Louisiana v. Callais effectively ended sixty years of protections against racial discrimination in elections. The Trump administration's executive order barring DEI programmes among federal contractors remained in force despite legal challenges, carrying significant financial penalties for non-compliance.

The political pendulum: From 2020 to "We ended DEI”

On September 22nd, 2020, President Trump issued Executive Order 13950, curtailing federal diversity training. At the same time, America was reeling from nationwide protests over the murder of George Floyd on May 25th, 2020, prompting a wave of corporate DEI commitments. On January 20th, 2021, President Biden rescinded Trump's ban and issued Executive Order 13985 to advance racial equity. The reprieve was short-lived. On June 29th, 2023, the Supreme Court struck down affirmative action in college admissions, emboldening legal challenges to corporate diversity programmes. By the end of that year, eleven states had passed anti-DEI laws; by mid-2025, that number reached 28.

Trump had campaigned against 'woke' business practices, and his return to office brought immediate executive action. In January 2025, he signed two executive orders directing federal agencies to 'terminate any equity-related plans' and investigate private-sector DEI programmes. Executive Order 14173 required federal contractors to certify they don't operate "illegal DEI" programmes, exposing non-compliant contractors to potential treble damages. On February 24th, 2026, Trump declared victory in his State of the Union address: "We ended DEI in America." Yet between Trump's declaration and the reality on the ground lies a picture that is neither as decisive nor as uniform as his words suggested.

Corporate retreats: Target and Walmart lead the rollback

The political pressure of 2023–2025 translated quickly into corporate action. Among US retailers, the rollbacks were neither tentative nor incremental:

- Target: On January 24th, 2025, just four days after Trump's anti-DEI executive orders, Target announced it would end its three-year DEI goals and its Racial Equity Action and Change (REACH) initiative. The retailer stopped participating in diversity indices and renamed its "Supplier Diversity" team to "Supplier Engagement." Seven months later, CEO Brian Cornell stepped down and transitioned to executive chairman. Analysts disagreed on whether the DEI rollback or operational struggles drove his departure .

- Walmart: The nation's largest retailer rolled back several DEI programmes in November 2024, choosing not to renew its five-year racial equity centre and ending supplier diversity goals. Conservative activist Robby Starbuck hailed Walmart's retrenchment as "the biggest win yet. " in the movement to “end wokeness.”

Target's double bind: The ICE crisis

Target's January 2025 DEI rollback was intended to reduce the retailer's exposure to political controversy.

Operation Metro Surge

In December 2025, the Department of Homeland Security launched Operation Metro Surge, deploying 3,000 federal immigration agents to Minnesota. The Trump administration simultaneously announced a 120% increase in ICE's workforce, adding 12,000+ officers. On January 7, 2026, ICE fatally shot Renee Good, a US citizen. On January 8, ICE agents detained two Target employees—both US citizens—at the Richfield, Minnesota, store in a widely circulated video. Target issued no public statement. Bloomberg characterised Target's silence as "overcorrection," arguing that while Target may have believed silence broadcast neutrality, "to customers and employees, it more likely suggests cooperation or collusion.”

Employee activism and corporate fear

More than 300 Target employees signed an internal letter urging executives to deny ICE access to Target properties without a warrant. Workers at multiple stores called out sick, fearing for their safety. On January 24th, Alex Pretti, a US citizen, was shot and killed during a Minneapolis protest. The next day, more than 60 Minnesota CEOs (including Target's incoming CEO) issued a cautious letter calling for "de-escalation" but neither condemning the killings nor calling for concrete action. The New York Times reported the muted response reflected "corporate fear of retaliation from the administration.

For Target, the silence contrasted sharply with its vocal 2020 response to George Floyd's murder. The company's trajectory from DEI champion (2020) to DEI sceptic (January 2025) to silent bystander (January–February 2026) illustrated what some call a "double bind": the DEI rollback failed to insulate Target from conservative criticism while alienating progressive customers and employees.

Broader retail impact

Target's predicament was not unique. Federal immigration enforcement targeted retail stores nationwide—Home Depot parking lots became a focal point for ICE sweeps, while hotel chains faced similar pressure: at least one franchisee's decision to decline rooms to ICE agents triggered a public rebuke from the authorities and the severing of its franchise agreement. Consumers organised multi-front boycotts. The "Resist and Unsubscribe" campaign targeted Amazon, Apple, Google, and others for ICE-enabling contracts. Target faced boycotts from both progressives, angered by the DEI rollback, and community members outraged by its ICE silence. Foot traffic fell 2% in Q4 2025.

In Worthington, Minnesota, where one in three residents is an immigrant, businesses reported sales declines of 50–70%. Latino grocery stores remained open but with locked doors, requiring employees to visually confirm that customers were not federal agents. The ICE surge threatened economic viability in communities where immigrant entrepreneurs had revived downtowns hollowed out decades earlier.

Legal uncertainty: When courts and agencies contradict each other

By early 2026, the legal landscape became a patchwork of competing rulings. On February 21st, 2025, a U.S. District Judge blocked key provisions of both executive orders, finding them "facially unconstitutionally vague." Nearly a year later, the U.S. Circuit Court of Appeals delivered a contrasting ruling in a separate case, vacating a preliminary injunction, ruling that Trump could direct agencies to terminate equity-related funding based on policy priorities.

For retailers, uncertainty crystallised when the Equal Employment Opportunity Commission (EEOC) targeted Nike on February 4th, 2026, investigating alleged discrimination against white employees based on Nike's public commitment to fill 30% of director positions with racial minorities. Yet six days later, EEOC backed down from investigating 20 major law firms, acknowledging compliance was "voluntary."

Later that month, the EEOC sued Coca-Cola, alleging that a two-day employer-sponsored networking event violated Title VII because only female employees were invited, excused from work, and paid, while male employees were excluded. The case suggested that the new enforcement climate was not limited to race-conscious targets or hiring goals; it could also reach sex-specific leadership and networking initiatives framed as inclusion efforts.

Private litigation compounded the pressure. A conservative legal strategist filed lawsuits challenging diversity fellowships at major law firms; three subsequently changed their eligibility criteria to allow any applicant to apply. McDonald's settled a lawsuit by opening its scholarship programme to "any student who can demonstrate an impact on or commitment to the Latino community."

The message was contradictory: DEI programmes faced heightened scrutiny, yet government enforcement authority remained contested and inconsistently applied. Federal contractors operated under strict prohibitions while non-contractors navigated murky guidance.

Holding the line or letting go: How department stores responded

Retailers responded with varying strategies. Macy's and Nordstrom maintained DEI commitments and chief diversity officers. Kohl's took a middle-ground approach, rebranding its role to "Chief Inclusion & Belonging Officer" in March 2025 while continuing related efforts. TJ Maxx maintains that "inclusion and diversity have been an important part of who we are." Smaller retailers like Faherty and Mason Dixie Foods publicly doubled down, framing DEI as core to company identity. Costco continues to support DEI initiatives, citing brand value alignment.

For retailers seeking a middle path, the evidence points toward inclusive universalism. Research by NYU suggests that opening diversity initiatives to everyone can encourage allyship, reduce backlash, and engage all employees in an inclusive culture. However, employees from historically marginalised groups may lose spaces for frank peer conversation—requiring acknowledgement of "what's been lost" rather than "toxic positivity."

From rollback to redesign: New DEI frameworks for retail

The question facing retailers in 2026 is not whether to pursue inclusion, but how to do so in ways that are legally defensible, genuinely effective, and able to survive the next political shift.

Levelling vs. Lifting

NYU research distinguishes between "lifting" strategies (targeted programmes for specific marginalised groups) and "levelling" strategies (removing bias from systems so processes become fairer for everyone). While lifting strategies face mounting legal challenges, levelling initiatives—structured interviewing, anonymised résumés, clear evaluation rubrics—create fairer processes and carry less legal risk. "The Supreme Court is never going to say it's illegal for an organisation to level the playing field by removing unconscious bias," a researcher notes.

The FAIR Framework

Inclusion consultant Lily Zheng's FAIR approach (Fairness, Access, Inclusion, Representation) prioritises "outcomes over intentions, systems over self-help, coalitions over cliques, and win-win over zero-sum." Rather than heritage month celebrations, FAIR demands interventions that solve problems by changing systems. Zheng reframes representation itself—shifting from demographic boxes to measuring trust: leaders who, regardless of identity, "understand our needs" and "speak with true understanding of what I care about." This emphasises the development of skills: critical thinking, relationship-building, and handling disagreement.

Targeted universalism

The most powerful concept is targeted universalism, developed by UC Berkeley's Othering and Belonging Institute: acknowledge group disparities while using that understanding to fix shared environmental problems. Zheng illustrates with a company where men dominated leadership but reported the worst well-being, while women had better outcomes but were underrepresented. Rather than framing it as a gender battle, they discovered that the underlying problem was a culture of overwork designed around the assumption that employees had stay-at-home spouses and few responsibilities outside work. Addressing the broken system improved outcomes for both men and women.

This embodies the "curb-cut effect"—when designing for those with the worst experiences, improvements benefit everyone. For retailers: rather than "How do we get more women into store management?" ask "What systemic barriers prevent excellent employees from advancing—and how do those barriers disproportionately affect certain groups?" Solving scheduling inflexibility or childcare support may disproportionately help women and parents while creating stronger talent pipelines for everyone.

As Target's experience illustrates — from DEI champion to rollback to ICE silence — attempts to sidestep inclusion through "neutrality" can backfire spectacularly. Trump's February 2026 declaration that "we ended DEI in America" glossed over a complex reality: while many companies rolled back targeted programmes under legal and political pressure, the work of creating fair, inclusive workplaces continue under different frameworks.

As documented in IADS' 2026 White Paper: DEI at a crossroads in retail, the retailers that weathered this period most effectively shared a common approach: DEI embedded in operations rather than siloed to HR, visible CEO backing, transparent communication during setbacks, and systems redesigned for their most marginalised employees — creating improvements that benefited everyone. The frameworks offered by various researchers suggest a clear direction: not abandoning the goal of fair workplace creation but reshaping how that work gets done. Systems-level changes removing bias don't just survive legal challenges — they build workplaces where everyone can contribute and advance based on actual merit. For retail facing persistent labour challenges and shifting consumer expectations, that is not just ethically sound — it is strategically essential.

By mid-February 2026, as Operation Metro Surge wound down, Target was left rebuilding trust on multiple fronts: with employees who felt abandoned, with customers questioning the company's values, and with a hometown that watched the retailer retreat from civic leadership. The lesson resonates beyond Target: the retailers that emerged from 2025–2026 with both credibility and capability intact were

Credits: Maya Sankoh

Retail Innovations Report 2026

Retail Innovations Report 2026

What: The 2026 Retail Innovations report showcases the transformation of retail through digital innovation, operational agility, and purpose-driven strategies worldwide.

Why it is important: The findings confirm that operational agility and technology-driven strategies are essential for resilience and growth in today’s retail landscape.

Retail Innovations, compiled by McMillanDoolittle and the Ebeltoft Group, captures a pivotal moment in the global retail industry as it adapts to the challenges and opportunities of the post-pandemic era. The report highlights how leading retailers are embracing digital transformation, integrating advanced technologies such as AI and data analytics to enhance operational efficiency and customer engagement. Sustainability and purpose-driven strategies have become central, with brands prioritizing eco-friendly practices and social responsibility to meet evolving consumer expectations. The emergence of new business models, including omnichannel and experiential retail, reflects a shift toward balancing digital convenience with the tangible benefits of physical stores. Retailers are also responding to changing consumer behaviors by curating personalized experiences and fostering community engagement. This wave of innovation is not only redefining competitive advantage but also setting new standards for resilience and growth in an increasingly complex and dynamic market environment.

IADS Notes: The 2026 edition of Retail Innovations reflects a global industry in transformation, as retailers respond to post-pandemic challenges with agility and creativity. Harvard Business Review in March 2026 highlights the importance of operational innovation and technology-driven efficiency for resilience. BCG’s September 2025 analysis underscores the resurgence of experiential and hybrid retail models, while BCG’s April 2025 report on Asia-Pacific details how digital innovation and strategic risk-taking are redefining leadership. Bain & Company’s September 2025 Innovation Report demonstrates that scaling transformative ideas and leveraging AI are critical for outperforming peers, and The Robin Report in April 2026 identifies consumer power, trust, and technology as the driving forces behind new business models and operational agility.

CEOs and boards are aligned on AI in theory, but divided in practice

CEOs and boards are aligned on AI in theory, but divided in practice

What: CEOs and boards are misaligned on AI governance, pace, and accountability, creating barriers to effective transformation.

Why it is important: The growing demand for AI literacy at the board level signals a shift in leadership expectations and the need for continuous upskilling.

The BCG CEOs and Boards Survey reveals a nuanced divide between chief executives and their boards regarding the governance, implementation, and valuation of AI. While both groups outwardly agree on the importance of AI, closer examination uncovers significant gaps in understanding and expectations. CEOs express concern that board members are influenced by media-driven AI hype and often overestimate the technology’s capabilities, while boards believe CEOs should more effectively communicate their AI vision and strategy. This misalignment extends to the pace of AI adoption, with boards typically favoring rapid implementation and CEOs advocating for a more measured approach. The survey also highlights that CEOs feel a greater sense of accountability for AI outcomes in their performance evaluations than boards recognize. As AI literacy becomes a baseline requirement for board membership, organizations are compelled to ensure that both executives and directors possess the knowledge and skills necessary to guide responsible and effective AI transformation. These disconnects, if left unaddressed, risk undermining organizational agility and the realization of AI’s full potential.

IADS Notes: The findings of the BCG survey are reinforced by recent analyses from INSEAD (January 2026), which emphasize the need for robust human oversight in AI governance, and Harvard Business Review (April 2026), which highlights the urgency of board-level engagement as AI-driven innovation accelerates. BCG (January and February 2026) further notes that CEOs are increasingly responsible for AI strategy and upskilling, but only organizations with strong governance and leadership commitment are achieving substantial results. Inside Retail (September 2025) cautions against automation bias, underscoring the importance of human-centric leadership and continuous learning to bridge the gap between ambition and operational reality.

CEOs and boards are aligned on AI in theory, but divided in practice - Full a

Sixty-One percent of CEOs say their boards are rushing AI transformation - Press Release

In the US, AI tools are more likely to increase entry-level hiring

In the US, AI tools are more likely to increase entry-level hiring

What: Despite fears of automation, most employers expect AI to increase entry-level hiring in 2026, but the nature of these roles is changing, with greater emphasis on critical thinking, adaptability, and real-world experience.

Why it is important: As AI transforms job requirements, retailers must redesign entry-level roles to foster critical thinking, adaptability, and long-term workforce resilience.

The rapid rise of artificial intelligence is reshaping the landscape of entry-level retail jobs, but not in the way many predicted. According to a recent survey of nearly 1,500 executives and senior talent leaders, almost three times as many expect AI to increase rather than decrease entry-level hiring in 2026. Rather than eliminating jobs, AI is shifting responsibilities away from routine and administrative tasks toward more analytical, judgment-based, and complex work. Employers now value critical thinking, communication, and collaboration above AI literacy for entry-level hires, and work experience—especially internships and project-based learning—has become the most important indicator of career readiness. As a result, academic achievement alone is less persuasive to retail employers. These findings highlight the need for retailers, educators, and policymakers to adapt training, recruitment, and workforce development strategies to align with the evolving demands of entry-level roles in the AI era, ensuring that new hires are equipped for long-term success and resilience.

IADS Notes: Aggressive AI automation in entry-level retail positions threatens long-term business sustainability by undermining talent development, institutional knowledge, and customer relationships (Harvard Business Review, March 2026; ERE Media, June 2025; Stanford Digital Economy Lab, September 2025). Only 36% of retail workers feel prepared for AI-driven change, with foundational skills and adaptability now central to workforce resilience (BCG, September 2025). While leading retailers achieve productivity gains through AI integration, success depends on augmentation rather than replacement, as only 10% of companies have successfully scaled their AI applications (BCG, July and September 2025). The Economist (March 2026) and Journal du Net (February 2026) emphasize that automation is fundamentally redesigning roles, elevating responsibilities, and requiring robust upskilling and governance for sustainable growth. ERE Media (June 2025) and Seramount (June 2025) stress that early talent programs and entry-level roles are critical for building future leadership benches, operational continuity, and innovation. Forbes (May 2026) and HR Dive (December 2025) highlight the growing importance of soft skills, adaptability, and work experience over academic credentials, while BCG (September 2025) and the Stanford Digital Economy Lab (September 2025) confirm that generative AI is most disruptive for entry-level roles, making workforce augmentation and systematic upskilling essential for sustainable transformation. Collectively, these findings demonstrate that the future of retail work depends on balancing technological advancement with human capital investment, protecting entry-level jobs, and redesigning them to maximize both business value and human development.

In the US, AI tools are more likely to increase entry-level hiring

Shopping in the age of AI

Shopping in the age of AI

What: Agentic AI is reshaping consumer discovery and purchase behavior, prompting retailers to rethink store missions, technology investments, and customer experience strategies.

Why it is important: Agentic AI is forcing retailers to adapt store formats, data strategies, and operational models to remain visible and relevant as AI mediates the customer journey.

As agentic AI becomes a default entry point for product discovery and routine purchasing, retailers and real estate players are being compelled to redefine the mission and design of physical stores. The rise of AI-driven shopping means that store visits may become less frequent but more valuable, with consumers increasingly relying on AI agents for research, basket building, and automated replenishment. This shift is driving a bifurcation in store formats: convenience-oriented locations must prioritize speed, reliability, and seamless digital integration, while discovery-led stores focus on curated experiences, personalization, and social connection. Gen Z and millennials are leading this transformation, demanding frictionless payment, omnichannel engagement, and experiential retail environments. Technology investments—such as digital-twin simulations, AI-driven demand forecasting, and clienteling tools—are now essential for optimizing store operations and elevating service. For landlords and developers, the imperative is to curate vibrant shopping ecosystems that combine retail, dining, and experiences, using data and placemaking strategies to attract and retain visitors. In this new era, success will depend on the ability to balance technological innovation with human-centric service and to ensure brand visibility within AI-mediated consumer journeys

IADS Notes: AI and agentic commerce are fundamentally transforming the retail landscape, as confirmed by recent IADS sources. Retail Touchpoints in January 2026 highlights how leading retailers like Walmart and Sephora are leveraging smaller, smarter AI models to drive measurable gains in efficiency, customer experience, and revenue growth, with 71% of retail employees now using AI tools weekly. The Robin Report in April 2026 emphasizes that AI-driven platforms have become the primary interface between shoppers and products, making AI visibility and engagement strategies essential for brand discovery and competitiveness. Inside Retail in April 2026 and BCG’s April 2026 research both underscore the urgency for retailers to adapt their infrastructure and merchandising models for agentic commerce, where AI agents mediate transactions and shift product discoverability from consumer choice to autonomous recommendation. Liontree in April 2026 confirms that nearly half of consumers—especially Gen Z and affluent shoppers—now act on AI-driven recommendations, making data quality, transparency, and agent-ready systems critical for retail relevance. Collectively, these sources illustrate that the winners in the new era of retail will be those who proactively invest in AI integration, data governance, and operational agility, while balancing technological innovation with human-centric service and experience. The imperative is clear: retailers and real estate players must redefine store formats, curate shopping ecosystems, and ensure their brands are visible and desirable within AI-driven consumer journeys to secure their place in the future of shopping.

Built for all: Rethinking career advancement in retail & CPG

Built for all: Rethinking career advancement in retail & CPG

What: LEAD Network and Shape Talent’s study identifies persistent barriers to women’s career progression in retail and CPG, despite recent gains in executive representation.

Why it is important: This issue underscores the need for systemic, measurable inclusion strategies to ensure lasting progress in retail leadership diversity.

The LEAD Network, in partnership with Shape Talent, has conducted a comprehensive study to uncover the root causes hindering women’s advancement in the retail and CPG sectors. While recent years have seen a notable increase in the number of women occupying senior executive roles, the research reveals that progress remains inconsistent across different functions and organisational levels. Persistent structural and cultural barriers continue to impede women’s career progression, highlighting a disconnect between headline diversity figures and the lived experience of female professionals. The study emphasises that genuine advancement requires more than just meeting numerical targets; it demands a fundamental shift toward systemic, measurable inclusion strategies. These findings are particularly relevant as the industry faces heightened scrutiny and evolving expectations around equity, flexibility, and leadership development. The report calls for a holistic approach that integrates diversity and inclusion into core business practices, ensuring that gains in representation translate into meaningful opportunities for women at every stage of their careers.

IADS Notes: The study’s findings align closely with recent industry analyses. In October 2025, the Gender Diversity Scorecard reported that women held 39% of senior executive roles in European retail and CPG, though representation remains uneven. February 2026 saw a record number of new female leaders, yet only half of retailers met the 40% executive target. As legal and political pressures reshape DEI language, frameworks like FAIR are gaining traction, as noted in February and March 2026. BCG’s March 2026 report further highlights the urgent need for systematic upski

Built for all: Rethinking career advancement in retail & CPG

NRF Europe’s Retail Trends report

NRF Europe’s Retail Trends report

What: The NRF’s 2026 Retail Trends report reveals how AI adoption is fundamentally transforming European retail, driving operational efficiency, personalisation, and new business models amid evolving regulatory demands.

Why it is important: The convergence of AI, regulatory compliance, and new revenue models is creating a widening gap between digital leaders and laggards, confirming trends identified in the past year.

European retail is undergoing a profound transformation as AI moves from isolated experimentation to a central pillar of business strategy, according to the NRF’s 2026 Retail Trends report. Retailers are rapidly increasing their investment in AI, with a growing share of technology budgets dedicated to these tools and a clear shift toward enterprise-wide integration. The most successful organisations are leveraging AI to drive operational efficiency, enhance personalisation, and optimise demand forecasting, resulting in measurable productivity gains and revenue uplift. However, the complexity of the European regulatory landscape, shaped by GDPR and the EU AI Act, demands rigorous data governance and transparency, making compliance a non-negotiable foundation for AI deployment. Agentic AI is reshaping customer service and in-store operations, balancing automation with the need for human oversight to maintain brand trust and service quality. Simultaneously, new business models such as retail media, licensing, and influencer-driven marketing are emerging, enabled by AI’s ability to harness first-party data and deliver targeted, high-margin revenue streams. The retailers that treat AI as a holistic operating system, rather than a collection of point solutions, are set to build lasting competitive advantages in this rapidly evolving landscape.

IADS Notes: The transformation described in the NRF’s 2026 Retail Trends report is echoed by recent industry analyses. In January and February 2026, sources such as Forbes and BCG highlighted the sector’s accelerated AI adoption and the shift from pilots to full-scale integration, with measurable gains in efficiency and customer engagement. MBS and Retail Touchpoints in early 2026 documented the rise of agentic AI and hyper-personalisation, while Forbes and Deloitte in late 2025 underscored the increasing complexity of regulatory compliance and the importance of robust governance. The emergence of retail media and new business models, as detailed by MBS and BCG in mid-2025, further confirms that the industry’s leaders are those who integrate AI, data, and organisational change into a coherent strategy.

Global Asset Management Report 2026: An imperative for growth

Global Asset Management Report 2026: An imperative for growth

What: The 2026 Global Asset Management Report reveals that retail investors, digital transformation, and AI are fundamentally reshaping the economics, distribution, and competitive landscape of asset management.

Why it is important: The findings highlight the convergence of technology, evolving investor demographics, and new distribution models, reflecting trends seen in the retail sector over the past year.

The 2026 Global Asset Management Report outlines a profound transformation in the industry, driven by the growing dominance of retail investors, the rise of digital-native clients, and the integration of advanced technologies such as AI and tokenisation. Retail investors now account for the majority of global asset growth, shifting the focus of asset managers toward scalable, digitally enabled distribution models and personalised client engagement. The report details how the convergence of wealth and asset management is blurring traditional boundaries, with firms acquiring advisory capabilities and deepening their integration into client value chains. Technology is at the heart of this evolution, with AI enabling operational efficiency, mass customisation, and expanded client coverage, while also demanding a fundamental redesign of operating models and talent strategies. The shift from defined benefit to defined contribution retirement systems further increases the complexity and scale of retail client servicing. Across all chapters, the report emphasises that future growth and profitability will depend on the ability to adapt to these structural shifts, build robust digital infrastructure, and leverage AI as a core competitive differentiator.

IADS Notes: The report’s themes are strongly echoed in recent industry developments. Regulatory debates over retail investor access to complex products and the rapid expansion of digital-first platforms like Revolut (May 2025) illustrate the growing influence of retail clients and the demand for integrated digital experiences. The convergence of wealth and asset management, as highlighted in BCG’s analysis of new revenue streams (Jun 2025), is reshaping competitive dynamics, while AI-driven transformation is now central to operational efficiency and customer engagement (Feb 2026). The shift in retirement benefit structures, seen in John Lewis’s overhaul of staff perks (May 2025), further underscores the need for modernised, flexible solutions in retail financial services.

Global Asset Management Report 2026: An imperative for growth

What happens to the human: Three moves inclusion leaders need to make in the next phase of AI

What happens to the human: Three moves inclusion leaders need to make in the next phase of AI

What: The article argues that as AI adoption accelerates, inclusion leaders must redesign work to build trust, prioritise human judgment, and ensure equitable access to opportunity.

Why it is important: This approach addresses the risks of bias, talent loss, and eroded trust that can arise when AI is layered onto legacy work models without inclusive leadership.

As AI becomes more deeply embedded in the workplace, the article highlights the urgent need for inclusion leaders to proactively redesign work environments to foster trust, safeguard human judgment, and guarantee equitable access to opportunity. Rather than simply adding AI to existing workflows, organisations must rethink how power, sponsorship, and developmental roles are distributed, ensuring that the benefits of AI do not disproportionately favour those already in positions of privilege. The risks of perpetuating or amplifying systemic inequities are significant, particularly in retail, where AI-driven hiring and automation can reinforce bias and undermine talent pipelines. The article stresses that trust is not a technical variable but a product of transparent leadership, clear expectations, and visible guardrails. By embedding responsible AI practices and prioritising human oversight, inclusion leaders can mitigate harm, preserve institutional knowledge, and create more resilient, innovative organisations. Ultimately, the piece calls for a shift from damage control to creative problem-solving, urging leaders to use AI as a force for good by redesigning work with justice and equity at the centre.

IADS Notes: The recommendations in this article are echoed in several recent studies and reports. The Seramount article “3 ways inclusion leaders should shape AI in the workplace” (Feb 2026) urges leaders to embed fairness, transparency, and human-centric oversight into AI rollouts. The Stanford Digital Economy Lab’s report “Canaries in the coal mine? Six facts about the recent employment effects of artificial intelligence” (Sep 2025) finds that augmenting, rather than replacing, human talent is essential for sustainable productivity in retail. Harvard Business Review’s “The Perils of Using AI to Replace Entry-Level Jobs” (Mar 2026) warns that automating entry-level roles can erode talent pipelines and institutional knowledge. ERE Media’s “Biased by design: How AI reinforces hiring discrimination” (Jul 2025) documents how AI-driven hiring tools risk perpetuating discrimination without ethical oversight. Finally, ESG Dive’s “US workers report a ‘major AI trust gap’ that affects their view of companies” (Dec 2025) highlights that most employees prefer human involvement in hiring and performance decisions, underscoring the need for trust, transparency, and accountability as AI becomes more prevalent in retail workforce management.

What happens to the human: Three moves inclusion leaders need to make in the next phase of AI

IADS Exclusive: Harrods points of differentiation

IADS Exclusive: Harrods points of differentiation

Few retailers conjure such immediate images of glamour, scale, and international cachet as Harrods. Yet behind the emerald-green awnings and gleaming marble halls lies a story of almost two centuries of reinvention. This single-site retailer has grown from a modest Victorian grocer’s shop into a global icon of luxury commerce. Harrods’ journey mirrors the evolution of modern retail itself: a chronicle of shrewd pivots and calculated risks, of disasters turned into opportunities, and of an unrelenting pursuit of the extraordinary in both product and experience.

We took the pretext of a member’s request on Harrods’ points of differentiation to proceed to an in-depth research about the iconic store. More than a department store, Harrods is a case study in how legacy can be leveraged, risks managed, and differentiation sharpened in a marketplace where change is the only constant. IADS CEOs were fortunate to have a behind-the-scenes visit in November 2023 during the General Assembly in London, with Mr G, a colourful character. We blend the notes taken during this visit with the results of thorough research to explore in more depth what Harrods represents today.

From “A small corner shop” in 1849…

Charles Henry Harrod opened his first venture in 1824, at the age of twenty-five: a drapery shop located in London’s South Bank, by then a district of taverns and inns. By 1834, having identified higher margins in the wholesale grocery trade, he pivoted towards selling pre-blended tea. He transferred to Cable Street, on the North Bank, and became recognised for his probity, as he insisted that only tea that he personally tasted could be sold in his premises.

However, the pivot took place in 1849, when Harrod identified an opportunity in Knightsbridge, which was then a semi-rural district adjacent to what would soon become the Crystal Palace grounds for the 1851 Great Exhibition. He leased a single-room shop at 105 Brompton Road to serve visitors to the exhibition, who discovered a merchant willing to dispatch hampers of preserves and teas to Glasgow, Calcutta, or Boston via the nascent railway and packet-boat networks. By 1855, it is said that Harrod employed 15 assistants and started annexing the neighbouring units.

Leadership passed to his son, Charles Digby Harrod, in 1861, who introduced new ideas, including dress fabrics, millinery, a perfumery counter, and, by 1870, a pharmacy. The introduction of fixed prices—still novel in Victorian England—liberated middle-class women from the chore of haggling and allowed them to shop unaccompanied, also accelerating turnover. Sales soared from an estimated £18,000 in 1861 to £118,000 by 1880 (equivalent to €19 million today). Technological innovations kept pace: gas-lit window displays extended trading hours, a lift expedited stock movement, and a pneumatic-tube network whisked cash to a central counting room.

On 6 December 1883, a fire destroyed the building on the eve of Christmas week. Overnight, Harrod rented a disused bakery, re-established departments and still posted a record profit, converting calamity into legend1. To finance reconstruction, he floated his company on the Stock Exchange in 1889, raising £120,000 and retiring days later.

The new board engaged architect Charles William Stephens, who erected today’s building in phases between 1894 and 1905. Innovation became a selling tool: in 1898, the store unveiled England’s first escalator (before the London Underground)—a leather‑belt “moving staircase” with staff waiting at the top with glasses of Cognac to comfort unnerved passengers. Electric lighting was the final touch, with 12,000 bulbs installed on the façade in 1906.

With the building complete, the company shifted focus from architecture to global reach. The Latin motto “Omnia Omnibus Ubique”—“All Things for All People, Everywhere”—was carved in 1908, coinciding with the launch of illustrated catalogues sent abroad. Orders arrived by telegram and, after 1911, by wireless. Export receipts accounted for an estimated 12‑15 % of turnover by the eve of the Great War.

The inter‑war decades burnished the store’s cultural cachet. Society diaries note lunching beneath the newly installed Art Nouveau stained‑glass dome of the first‑floor Georgian Restaurant (1913), where playwright Noël Coward reputedly purchased a baby alligator in the 1920s. Harrods also joined the International Association of Department Stores in 1928. Along with Filene’s from Boston and Printemps from Paris, to name a few, the then IADS members aimed to introduce modern management methods derived from the scientific management movement to their retail format.

During WWII, the Food Halls’ marble counters were sandbagged, and the basement converted into an air‑raid shelter. Despite rationing, the store maintained “Make‑Do‑and‑Mend” workshops and even a couture salon supplying utility clothing that met Ministry of Supply regulations but still permitted discreet elegance.

The 1950s brought optimism and a surge in interest. In 1959, House of Fraser outbid Debenhams to acquire Harrods for £7.6 million. The deal provided the flagship capital for mechanical goods-handling systems, while allowing operational autonomy—a “federal” model of ownership. During that period of ownership, the store was struck by an IRA car bomb, in which six were killed and ninety were injured[2].

House of Fraser sold Harrods (and itself[3]) to Egyptian‑born entrepreneur Mohamed Al‑Fayed for £615 million in 1985. Over the next quarter-century, Al-Fayed spent a reported £400 million on restorations that blurred the lines between commerce and spectacle: the themed Egyptian Hall with its gilded sarcophagi, the opaline-glass Egyptian Escalator, and marble memorials to Diana, Princess of Wales, and Dodi Al-Fayed. Footfall doubled from roughly 12 million in 1984 to 23 million by 1999, fueled by long-haul tourism and the weak sterling of the late-1990s Asian crisis. He pioneered experiential retail: celebrity book signings, Britain’s first in-store Ladurée tearoom in 2005, and the By Appointment personal-shopping suite introduced in 2006, which featured minimum-spend thresholds. Finally, Michael Ward was installed as managing director in 2005.

In May 2010, Qatar Holding, part of the Qatar Investment Authority (QIA), paid about £1.5 bn and invested in modernising the company:

- Harrods.com was launched in 2011, followed by a Mainland-China WeChat storefront in 2018,

- “Superbrands Hall”, a 3,716 sqm “store above the store”, opened in 2014 to monetise shop-in-shop tenancies from Chanel to Audemars Piguet,

- “The Residence”, unveiled in 2020, created a private-members’ enclave rumoured to require a £ 250,000 annual spend covenant.

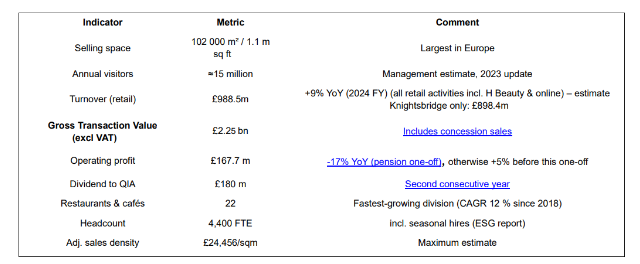

Today, the Knightsbridge store occupies 92,000 sqm of selling space across eight public floors and 330 departments, supported by 22 branded restaurants and bars. It sells a wide variety of luxury products, from €5,000 per kg rare tea, to yachts or gold ingots (since 2010). Approximately 70% of the floor space is operated on a concession or consignment basis. Following the men’s department transformation and the beauty section renewal with a VIP section unveiled in 2016 at a cost of £200 million, another £200 million rolling refurbishment (2023-26) is reshaping sales floors as “experiential precincts.” The 1,500 sqm lingerie and loungewear hall opened in June 2023 (for £60 million), featuring wellness pods, fitting salons, and a café run by Parisian pâtissier Pierre Hermé. The Dining Hall’s relaunch in autumn 2024 introduced a complete offer of 22 chef-counter concepts—most notably a 12-seat omakase bar by Masayoshi Takayama, which now has a nine-month waiting list, and four distinct food halls (including an on-site chocolate factory and bakery). Finally, the “By Appointment” private-shopping suites on the hidden fifth floor are said to account for roughly 11% of GMV, with an average transaction value exceeding £55,000.

Baseline footfall rebounded to its pre-pandemic base of roughly 15 million visits, with peaks of up to 300,000 daily visitors in the Christmas trading window and the loyalty programme is believed to house 2m members. Revenue density in Knightsbridge is estimated to reach € 29,000 per sqm[4]. Overseas customers generate 45% of sales[5], despite the UK’s abolition of VAT-free shopping. To make sure a specific part of this clientele (Chinese tourists) is properly served even when not in the UK, Harrods opened a private member club in Shanghai in 2024.

Beyond Knightsbridge, the group operates six standalone H Beauty stores, a format of 2,000–2,800 sqm aimed at Millennial and Gen-Z luxury beauty shoppers. A seventh unit, in Chester, is under construction for 2025, followed by Leeds in 2026.

Harrods employs 4,550 FTEs, who follow a rigorous line of conduct to convey the excellence the store aims to represent. However, labour relations remain tricky, as shown by the strike mandate covering 176 shop-floor, hospitality and cleaning employees for the peak Christmas week of 2024 in a dispute over bonuses, service-charge distribution and pay indexation.

…to a diversified powerhouse in 2025

The Knightsbridge store operations, harrods.com, and the adjacent subsidiaries (including other stores, airlines, and real estate) sit within Harrods Ltd, a holding company. It is unclear where the Chinese club operations are located[6].

Full-year 2024 group results show gross transaction value up 6% (£2,25 bn), group turnover up 9% to £988.5, and store turnover up 8% to £898.4 m (+8% vs. LY), the highest in the store’s history. Operating profit edged up to £162.9 million, delivering an 18 % margin, while a one-off £46m pension buy-in trimmed pre-tax profit to £111.5 million. Despite that hit, Qatar Holding, the owner, took a £180m dividend for the second year running. Net cash closed at just over £50 million after capital expenditure of roughly £95m on store refurbishment and digital projects. Measured over four post-pandemic years, sales have compounded at a 27% annual rate and operating profit at a 33% yearly rate, outstripping every Western department-store peer in both metrics. Even after normalising for one-offs, its 18% operating margin dwarfs Western department-store averages (5-10%).

Online sales on harrods.com are estimated to have reached £230 million during FY2024, equivalent to 26% of retail turnover, with mobile devices accounting for 72% of sessions. A smart, RFID-enabled distribution centre at West Thurrock is set to go online in H2 2025, aiming to reduce click-to-ship times to below 90 minutes and eliminate 99% of picking errors. Also, in November 2024, Harrods adopted Global-e’s cross-border platform, localising pricing, payments, and duty prepayment for more than 200 markets. February 2025 marked the launch of an AI marketing partnership with Incubeta; its Seamless Search engine reallocates paid media spend in real-time across PPC, SEO, and social in the UK, US, GCC, and Asia hubs. Loyalty penetration has climbed to 87 % of transactions since the introduction of a new Platinum tier (annual spend threshold £50,000) within the five-level Harrods Rewards scheme. Repeat-purchase frequency averages 3.2 times per year across the Rewards base and 6.8 times for Black-tier members.

Regarding other activities, the aviation cluster—Harrods Aviation (FBO/MRO at Luton and Stansted) and Air Harrods helicopter charter—generated £78.8m of turnover in 2024 and employs 275 staff, feeding ultra-high-net-worth clients back to the retail and property arms. Harrods Estates, the prime-property brokerage, leverages Rewards-tier data but keeps its financials private.

Finally, as of FY2023, the board has incorporated explicit ESG and customer-experience key performance indicators into the audit and risk committee’s remit, aligning management remuneration with decarbonisation and service-quality milestones. Harrods’ inaugural ESG report logged a 2.4% absolute carbon reduction against the 2022 baseline and reiterated the 90% cut goal for 2030. Eighty per cent of lights are now LED, and trigeneration supplies a growing share of on-site energy. Major projects include a £60 million façade and HVAC retrofit—Phase I was completed in Q4 2024—which underpins the pledge to cut Scope 1–2 emissions by 90% by 2030.

What are Harrod’s points of differentiation?

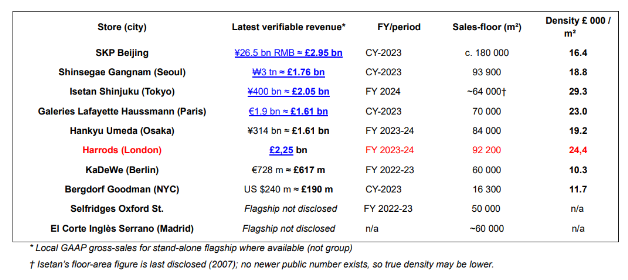

While being unique in the world, Harrods competes in the same league as Selfridges, KaDeWe, Galeries Lafayette Haussmann, Saks Fifth Avenue, Isetan Shinjuku, SKP Beijing, Bergdorf Goodman, Hankyu Umeda, Shinsegae and El Corte Inglés Serrano Madrid. For this reason, we review how the store differentiates from this array of peers from a selection of criteria: real estate ownership, revenue density, the nature of the concession ecosystem, the private client culture, the approach to service and experience, and the loyalty and omnichannel approach.