IADS Exclusive: Harrods points of differentiation

Few retailers conjure such immediate images of glamour, scale, and international cachet as Harrods. Yet behind the emerald-green awnings and gleaming marble halls lies a story of almost two centuries of reinvention. This single-site retailer has grown from a modest Victorian grocer’s shop into a global icon of luxury commerce. Harrods’ journey mirrors the evolution of modern retail itself: a chronicle of shrewd pivots and calculated risks, of disasters turned into opportunities, and of an unrelenting pursuit of the extraordinary in both product and experience.

We took the pretext of a member’s request on Harrods’ points of differentiation to proceed to an in-depth research about the iconic store. More than a department store, Harrods is a case study in how legacy can be leveraged, risks managed, and differentiation sharpened in a marketplace where change is the only constant. IADS CEOs were fortunate to have a behind-the-scenes visit in November 2023 during the General Assembly in London, with Mr G, a colourful character. We blend the notes taken during this visit with the results of thorough research to explore in more depth what Harrods represents today.

From “A small corner shop” in 1849…

Charles Henry Harrod opened his first venture in 1824, at the age of twenty-five: a drapery shop located in London’s South Bank, by then a district of taverns and inns. By 1834, having identified higher margins in the wholesale grocery trade, he pivoted towards selling pre-blended tea. He transferred to Cable Street, on the North Bank, and became recognised for his probity, as he insisted that only tea that he personally tasted could be sold in his premises.

However, the pivot took place in 1849, when Harrod identified an opportunity in Knightsbridge, which was then a semi-rural district adjacent to what would soon become the Crystal Palace grounds for the 1851 Great Exhibition. He leased a single-room shop at 105 Brompton Road to serve visitors to the exhibition, who discovered a merchant willing to dispatch hampers of preserves and teas to Glasgow, Calcutta, or Boston via the nascent railway and packet-boat networks. By 1855, it is said that Harrod employed 15 assistants and started annexing the neighbouring units.

Leadership passed to his son, Charles Digby Harrod, in 1861, who introduced new ideas, including dress fabrics, millinery, a perfumery counter, and, by 1870, a pharmacy. The introduction of fixed prices—still novel in Victorian England—liberated middle-class women from the chore of haggling and allowed them to shop unaccompanied, also accelerating turnover. Sales soared from an estimated £18,000 in 1861 to £118,000 by 1880 (equivalent to €19 million today). Technological innovations kept pace: gas-lit window displays extended trading hours, a lift expedited stock movement, and a pneumatic-tube network whisked cash to a central counting room.

On 6 December 1883, a fire destroyed the building on the eve of Christmas week. Overnight, Harrod rented a disused bakery, re-established departments and still posted a record profit, converting calamity into legend1. To finance reconstruction, he floated his company on the Stock Exchange in 1889, raising £120,000 and retiring days later.

The new board engaged architect Charles William Stephens, who erected today’s building in phases between 1894 and 1905. Innovation became a selling tool: in 1898, the store unveiled England’s first escalator (before the London Underground)—a leather‑belt “moving staircase” with staff waiting at the top with glasses of Cognac to comfort unnerved passengers. Electric lighting was the final touch, with 12,000 bulbs installed on the façade in 1906.

With the building complete, the company shifted focus from architecture to global reach. The Latin motto “Omnia Omnibus Ubique”—“All Things for All People, Everywhere”—was carved in 1908, coinciding with the launch of illustrated catalogues sent abroad. Orders arrived by telegram and, after 1911, by wireless. Export receipts accounted for an estimated 12‑15 % of turnover by the eve of the Great War.

The inter‑war decades burnished the store’s cultural cachet. Society diaries note lunching beneath the newly installed Art Nouveau stained‑glass dome of the first‑floor Georgian Restaurant (1913), where playwright Noël Coward reputedly purchased a baby alligator in the 1920s. Harrods also joined the International Association of Department Stores in 1928. Along with Filene’s from Boston and Printemps from Paris, to name a few, the then IADS members aimed to introduce modern management methods derived from the scientific management movement to their retail format.

During WWII, the Food Halls’ marble counters were sandbagged, and the basement converted into an air‑raid shelter. Despite rationing, the store maintained “Make‑Do‑and‑Mend” workshops and even a couture salon supplying utility clothing that met Ministry of Supply regulations but still permitted discreet elegance.

The 1950s brought optimism and a surge in interest. In 1959, House of Fraser outbid Debenhams to acquire Harrods for £7.6 million. The deal provided the flagship capital for mechanical goods-handling systems, while allowing operational autonomy—a “federal” model of ownership. During that period of ownership, the store was struck by an IRA car bomb, in which six were killed and ninety were injured[2].

House of Fraser sold Harrods (and itself[3]) to Egyptian‑born entrepreneur Mohamed Al‑Fayed for £615 million in 1985. Over the next quarter-century, Al-Fayed spent a reported £400 million on restorations that blurred the lines between commerce and spectacle: the themed Egyptian Hall with its gilded sarcophagi, the opaline-glass Egyptian Escalator, and marble memorials to Diana, Princess of Wales, and Dodi Al-Fayed. Footfall doubled from roughly 12 million in 1984 to 23 million by 1999, fueled by long-haul tourism and the weak sterling of the late-1990s Asian crisis. He pioneered experiential retail: celebrity book signings, Britain’s first in-store Ladurée tearoom in 2005, and the By Appointment personal-shopping suite introduced in 2006, which featured minimum-spend thresholds. Finally, Michael Ward was installed as managing director in 2005.

In May 2010, Qatar Holding, part of the Qatar Investment Authority (QIA), paid about £1.5 bn and invested in modernising the company:

- Harrods.com was launched in 2011, followed by a Mainland-China WeChat storefront in 2018,

- “Superbrands Hall”, a 3,716 sqm “store above the store”, opened in 2014 to monetise shop-in-shop tenancies from Chanel to Audemars Piguet,

- “The Residence”, unveiled in 2020, created a private-members’ enclave rumoured to require a £ 250,000 annual spend covenant.

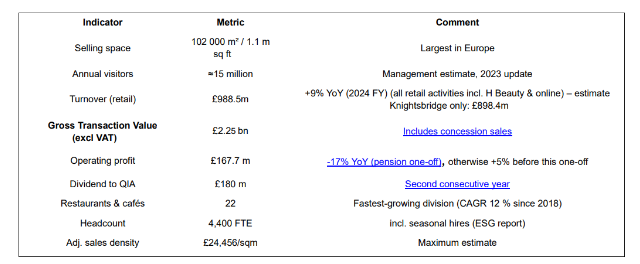

Today, the Knightsbridge store occupies 92,000 sqm of selling space across eight public floors and 330 departments, supported by 22 branded restaurants and bars. It sells a wide variety of luxury products, from €5,000 per kg rare tea, to yachts or gold ingots (since 2010). Approximately 70% of the floor space is operated on a concession or consignment basis. Following the men’s department transformation and the beauty section renewal with a VIP section unveiled in 2016 at a cost of £200 million, another £200 million rolling refurbishment (2023-26) is reshaping sales floors as “experiential precincts.” The 1,500 sqm lingerie and loungewear hall opened in June 2023 (for £60 million), featuring wellness pods, fitting salons, and a café run by Parisian pâtissier Pierre Hermé. The Dining Hall’s relaunch in autumn 2024 introduced a complete offer of 22 chef-counter concepts—most notably a 12-seat omakase bar by Masayoshi Takayama, which now has a nine-month waiting list, and four distinct food halls (including an on-site chocolate factory and bakery). Finally, the “By Appointment” private-shopping suites on the hidden fifth floor are said to account for roughly 11% of GMV, with an average transaction value exceeding £55,000.

Baseline footfall rebounded to its pre-pandemic base of roughly 15 million visits, with peaks of up to 300,000 daily visitors in the Christmas trading window and the loyalty programme is believed to house 2m members. Revenue density in Knightsbridge is estimated to reach € 29,000 per sqm[4]. Overseas customers generate 45% of sales[5], despite the UK’s abolition of VAT-free shopping. To make sure a specific part of this clientele (Chinese tourists) is properly served even when not in the UK, Harrods opened a private member club in Shanghai in 2024.

Beyond Knightsbridge, the group operates six standalone H Beauty stores, a format of 2,000–2,800 sqm aimed at Millennial and Gen-Z luxury beauty shoppers. A seventh unit, in Chester, is under construction for 2025, followed by Leeds in 2026.

Harrods employs 4,550 FTEs, who follow a rigorous line of conduct to convey the excellence the store aims to represent. However, labour relations remain tricky, as shown by the strike mandate covering 176 shop-floor, hospitality and cleaning employees for the peak Christmas week of 2024 in a dispute over bonuses, service-charge distribution and pay indexation.

…to a diversified powerhouse in 2025

The Knightsbridge store operations, harrods.com, and the adjacent subsidiaries (including other stores, airlines, and real estate) sit within Harrods Ltd, a holding company. It is unclear where the Chinese club operations are located[6].

Full-year 2024 group results show gross transaction value up 6% (£2,25 bn), group turnover up 9% to £988.5, and store turnover up 8% to £898.4 m (+8% vs. LY), the highest in the store’s history. Operating profit edged up to £162.9 million, delivering an 18 % margin, while a one-off £46m pension buy-in trimmed pre-tax profit to £111.5 million. Despite that hit, Qatar Holding, the owner, took a £180m dividend for the second year running. Net cash closed at just over £50 million after capital expenditure of roughly £95m on store refurbishment and digital projects. Measured over four post-pandemic years, sales have compounded at a 27% annual rate and operating profit at a 33% yearly rate, outstripping every Western department-store peer in both metrics. Even after normalising for one-offs, its 18% operating margin dwarfs Western department-store averages (5-10%).

Online sales on harrods.com are estimated to have reached £230 million during FY2024, equivalent to 26% of retail turnover, with mobile devices accounting for 72% of sessions. A smart, RFID-enabled distribution centre at West Thurrock is set to go online in H2 2025, aiming to reduce click-to-ship times to below 90 minutes and eliminate 99% of picking errors. Also, in November 2024, Harrods adopted Global-e’s cross-border platform, localising pricing, payments, and duty prepayment for more than 200 markets. February 2025 marked the launch of an AI marketing partnership with Incubeta; its Seamless Search engine reallocates paid media spend in real-time across PPC, SEO, and social in the UK, US, GCC, and Asia hubs. Loyalty penetration has climbed to 87 % of transactions since the introduction of a new Platinum tier (annual spend threshold £50,000) within the five-level Harrods Rewards scheme. Repeat-purchase frequency averages 3.2 times per year across the Rewards base and 6.8 times for Black-tier members.

Regarding other activities, the aviation cluster—Harrods Aviation (FBO/MRO at Luton and Stansted) and Air Harrods helicopter charter—generated £78.8m of turnover in 2024 and employs 275 staff, feeding ultra-high-net-worth clients back to the retail and property arms. Harrods Estates, the prime-property brokerage, leverages Rewards-tier data but keeps its financials private.

Finally, as of FY2023, the board has incorporated explicit ESG and customer-experience key performance indicators into the audit and risk committee’s remit, aligning management remuneration with decarbonisation and service-quality milestones. Harrods’ inaugural ESG report logged a 2.4% absolute carbon reduction against the 2022 baseline and reiterated the 90% cut goal for 2030. Eighty per cent of lights are now LED, and trigeneration supplies a growing share of on-site energy. Major projects include a £60 million façade and HVAC retrofit—Phase I was completed in Q4 2024—which underpins the pledge to cut Scope 1–2 emissions by 90% by 2030.

What are Harrod’s points of differentiation?

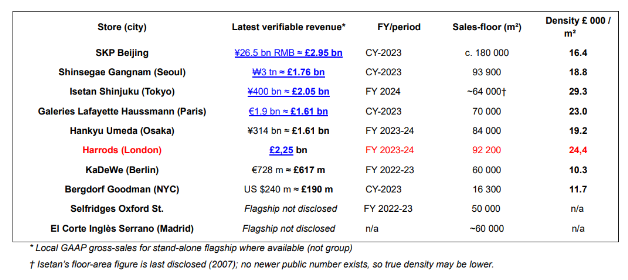

While being unique in the world, Harrods competes in the same league as Selfridges, KaDeWe, Galeries Lafayette Haussmann, Saks Fifth Avenue, Isetan Shinjuku, SKP Beijing, Bergdorf Goodman, Hankyu Umeda, Shinsegae and El Corte Inglés Serrano Madrid. For this reason, we review how the store differentiates from this array of peers from a selection of criteria: real estate ownership, revenue density, the nature of the concession ecosystem, the private client culture, the approach to service and experience, and the loyalty and omnichannel approach.

Harrods occupies a five-acre, Grade II* listed city-block[1] that it controls outright; the 92,000 sqm selling floor was purpose-built for the brand between 1894 and 1905 and has remained under single ownership ever since. This freehold status (acquired in 1921) allows Harrods to avoid rent inflation or landlord risk that has crippled rivals such as KaDeWe, whose 2024 insolvency filing cited “significantly rising index-linked rents” as the key trigger. By contrast, Selfridges’ Oxford Street flagship sits in a separate property vehicle whose £638 million write-down last year illustrates the balance-sheet drag of leasehold real estate.

While Saks Fifth Avenue and Bergdorf Goodman all operate on highly-leveraged trophy real estate (Saks’ flagship alone is mortgaged at a $3.6 bn appraisal), owning the land lets Harrods commit substantial horizons of capital (e.g., a self-funded £300 m restoration of its historic Food Halls, a £200 m womenswear revamp slated to 2026).

Even though some commentators tried to assess department stores’ productivity, often on partial data (which raises questions, see the 2019 Sybarite report), Harrods was often cited pre-pandemic as the most productive department store in the world, outpaced by SKP during the pandemic in 2020-2021.

However, when looking at the details, proceeding to a complete comparison of companies is difficult when it comes to productivity:

- Selfridges and El Corte Inglés do not publish verified single-store turnover, forcing extrapolations.

- No verified information has been published by Isetan Shinjuku since 2007 regarding its size,

- When it comes to the definition of selling space itself, some groups exclude restaurants or event space, others include them.

- Chinese and Korean department stores quote tax-inclusive transaction value; Western peers report net revenue. Density rankings, therefore, give a directional, not absolute, comparison.

- SKP, Bergdorf Goodman and Galeries Lafayette figures rely on management statements rather than statutory filings.

- In a similar manner, gross transaction value for 2024 for Harrods is only released at the group level, not the store level, which makes the comparison slightly incorrect.

The below chart is a tentative ranking, taking into account the limitations above. While Asian mega-stores and Galeries Lafayette compete with Harrods in terms of sheer turnover, and in sales density by others, Harrods punches above its size in productivity, thanks to ultra-high conversion rates in luxury categories and tourist spending.

Harrods remains the archetype of the concession-first model (estimated to represent 70% of turnover): brands control product, staffing, and visual merchandising, while the store takes a commission or minimum rent, guaranteeing near-zero gross-margin risk and securing the store’s time-bound exclusives. Retail commentators have long noted that, unlike Selfridges’ pop-up-heavy strategy, Harrods “has stuck with its traditional model of in-store luxury brand concessions” as the core of its offer. For instance, on the sixth floor, Harrods boasts the world’s largest Apple concession, uniquely operated by Harrods rather than Apple itself. Harrods is also said to have a model where it provides staff, whose gross salary is passed on to brands, either in full or proportionally, according to their contractual agreement. Similarly Harrods is the only location to house a Tom Ford women’s store outside of the brand’s DOS network.

While Isetan maintains a traditional mix, Selfridges has moved closer to a wholesale and consignment model hybrid to drive newness and curation. Selfridges mitigates its risks by imposing guaranteed sell-through to many wholesale brands, while Bergdorf still carries significant own-buy risk in seasonal fashion. SKP Beijing replicates Harrods’ concession logic. Hankyu and KaDeWe blend concessions with outright buy, leaving them more exposed to markdowns in weak cycles. Harrods is one of the few Western stores that uses the concession structure at the whole-store scale, enabling more than 330 brand-managed spaces, increasing (by delegation) refresh cycles and gross margin.

As put by Michael Ward, “our customers come back as friends. It is not just a question of sales, but relationships.”

In addition to a Chief Customer Officer appointed as early as 2018, Harrods fields more than 3,000 customer-facing staff and formalises elite service through two-tiered programs: By Appointment (fifth-floor personal shopping with a worldwide-known quality of service) and Private Shopping – The Penthouse (invitation-only suites on the sixth floor with separate entrance). Comparable offers exist, but with less spatial grandeur: Bergdorf Goodman’s seventh-floor “BG Salon” occupies less than 10,000 sq ft each, versus Harrods’ full-floor 35,000 sq ft client area. Saks Fifth Avenue club rooms remain a minority of sales. Selfridges offers personal shopping suites on the first and second floors. SKP and Shinsegae run powerful VIP clubs, but none monetises membership as visibly in-store through physical By Appointment suites overlooking Hyde Park. Exclusivity extends to customer engagement, with only 250 elite customers selected by directors, representing 10% of the business.

To cater for the ultra-wealthy, security and exclusivity are paramount at Harrods, with more police on duty within the store than in the surrounding borough, and even a dedicated police station onsite.

In addition, the Knightsbridge flagship is only one profit engine powering a full ecosystem. Harrods operates:

- Harrods Aviation – two London-area FBOs turning over £78.8 m in 2024.

- H Beauty – five suburban beauty-only stores, seeding the brand with younger customers.

- Harrods International – franchised airport units from Heathrow to Shanghai.

- A private member club in Shanghai, opened in 2024, including a tea room, bar and Gordon Ramsay restaurant.

None of the peers has such an integrated private-aviation, specialist beauty chain ecosystem, or overseas club. That allows to provide a very specific experiential ecosystem for the wealthy: in-store, food-to-fork gastronomy (22 restaurants after the Georgian Room relaunch) plus on-site spa, safe-deposit vaults. Granted, Bergdorf and Saks excel at curated fashion edits; Galeries Lafayette and El Corte Inglés leverage tourist tax-free shopping. However, Harrods goes beyond by also providing the ecosystem outside of the store. While Selfridges has flirted with hotel and property development but remains retail-centric, KaDeWe and Galeries Lafayette have few meaningful non-retail subsidiaries, Isetan’s side-lines are largely food halls and credit cards, Harrods layers on aviation, helicopter charter and prime-property brokerage (businesses that add profit streams and feed ultra-high-net-worth clients back to Knightsbridge), enlarging its share-of-wallet beyond a store visit.

Loyalty and omnichannel approach

Harrods’ four-tier Rewards programme—recently augmented by a Platinum layer for clients spending £50 k+ per annum—delivers SKU-level data on approximately 2.8 million active members, feeding dynamic CRM and increasing lifetime spend. Loyalty IDs are linked to 87 % of transactions. Selfridges and Galeries Lafayette have broader membership bases but lower spend thresholds, limiting luxury specificity.

When it comes to online, Harrods has historically resisted a full e-commerce push until it could replicate concession economics online, first with Farfetch. Its 2024 Global-e partnership instantly opened 200+ localised markets while letting brands keep price control—again, landlord logic extended to the cloud. Most continental peers still rely on cross-border marketplaces or border-free shipping intermediaries rather than direct localisation. Selfridges.com and Saks.com are further advanced in terms of volume, yet rely on marketplace inventory models that dilute margin and branding discipline.

As a corollary, the store does not envision promotional activities in a traditional way, but rather as a collection of “theatrical experiences” available at each floor. It is all about leveraging private relationships with customers and creating a feeling of closeness with the store, as the iconic Christmas market or Rihanna launching in person her brand Fenty in 2021 suggest. There are no sales campaign apart from the Harrods Winter and Summer sales which remain very elegant and far away from promotional sales seen in other department stores.

What are the potential risks faced by Harrods?

Harrods’ performance edge rests on a delicate macro-and-micro balance that can be fragile.:

Since January 2021 the UK has refused non-EU visitors a VAT rebate, a decision that has pulled high-spending tourists towards Paris and Milan and cost London’s West End retailers an estimated £220 million in lost sales in the first half of 2024 alone. Internal modelling shared in lobbying documents seen by Walpole suggests that Harrods itself lost roughly £80-90 million of Chinese and GCC spend in FY 2024[1]. As long as the Treasury resists reinstating tax-free shopping, the growth will depend on compensating volume from domestic and US consumers whose currency advantage is already eroding.

Harrods’ ESG report discloses that just 4% of active shoppers account for 28% of revenue. A correction in luxury-equity valuations, further sanctions on Russian or Middle-Eastern elites, or geopolitical tension that curtails Gulf air routes could therefore reverberate disproportionately through top-line sales.

The Qatar Investment Authority has extracted consecutive £180 million dividends in the last two financial years, signalling a possible shift from long-duration capital stewardship to cash harvesting as the Gulf state funds other diversification projects. Should that preference harden, capex headroom for the ongoing £200 million Knightsbridge refurbishment could narrow, forcing trade-offs between experience upgrades and balance-sheet prudence.

Although Harrods has spent about £75 million updating its tech stack since 2018 and completed a 360-degree SAP/KPS customer-data rebuild in 2023, order-management and stock-ledger systems remain largely monolithic. By contrast, Selfridges moved to a micro-service architecture last year and now tasks multichannel teams with fulfilling most web orders inside 24 hours, a KPI advertised internally and in recruitment posts; Harrods’ average sits closer to two days. Lags of that magnitude can become visible to premium shoppers who benchmark their experiences against Farfetch‐style next-day standards.

SKP Beijing booked RMB 26.5 billion (£2.9 billion) in 2023, illustrating how purchasing power and brand exclusivity are clustering in Asia’s mega-malls. The same dynamic is visible in Shinsegae Gangnam and Isetan Shinjuku. If luxury brands choose to allocate limited-edition products on the basis of absolute volume, Harrods could cede pre-launch exclusives that have historically underpinned its differentiation. This is therefore interesting that they have opened a private member club in China, allowing them to leverage this presence to luxury brands and ask for ultra-exclusive collaborations or special editions.

The Knightsbridge block is Grade II*: every structural alteration requires listed-building consent under Westminster guidance, a process that local planning files show can extend beyond eight months for even minor plumbing or ductwork changes. Asset intensity thus stymies rapid re-configuration at a moment when luxury merchandising is shifting from static departments to theatrical, fast-turn “activations”.

The National Crime Agency’s unexplained-wealth-order pursuit of Zamira Hajiyeva, who spent more than £16 million at Harrods, spotlighted the store’s in-house bureau de change and its attraction for high-value cash clients; the case ended in a forced property forfeiture last August. The Financial Conduct Authority has since tightened monitoring of high-value dealers, meaning any lapse in anti-money-laundering controls could trigger fines or even suspension of the currency-exchange licence that lubricates tourist spending.

Conclusion: Harrods, a unique model?

Harrods’ differentiation is not a single attribute but a mutually reinforcing system: debt-free freehold real estate, global-class revenue density, a concession model that limits risk, a service culture scaled through data-rich loyalty, and lateral businesses—from aviation to H Beauty—that diversify earnings while feeding the core brand halo. Said in other words, and using Porter’s resource-based lens, Harrods converts location (Knightsbridge cluster of five-star hotels), hard assets (unencumbered freehold) and organisational heritage (175-year archives) into sustained differentiation. Among the expanded peer set, each competitor can match Harrods on one or two vectors (SKP on revenue, Bergdorf on architectural prestige, Shinsegae on turnover growth), but none combines all of them with the same depth.

Looking forward, management faces a triad of macro uncertainties—modulated Chinese tourism, geopolitical shocks and emergent regulation of high-end consumables—yet enjoys four built-in shock absorbers:

- Sovereign-wealth backing capable of counter-cyclical investment (which can also be a double-edged sword),

- A landlord-concession template that shifts inventory risk (but comes with its own constraints, too),

- A heritage narrative proven to restore confidence (unless, like in the Al Fayed sex scandal, some timebombs emerge),

- An ESG roadmap designed to meet stakeholder capitalism head-on.

Expansion is unlikely to resemble branch proliferation; instead, incremental monetisation of vertical space, deeper data-driven clienteling and selective brand residencies will probably continue to increase sales density.

Credits: IADS (Selvane Mohandas)

Related posts

AI in CPG and retail: how winners are pulling ahead

AI in CPG and retail: how winners are pulling ahead

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

IADS Exclusive - How department stores are playing the 2026 FIFA World Cup

IADS Exclusive - How department stores are playing the 2026 FIFA World Cup

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript