IADS Exclusive – Macy’s: from the world’s largest store to a leaner future

Macy’s story is that of an American institution. From a single store in 1858 to a nationwide banner, it became not only a retail powerhouse but a cultural symbol woven into American life. Unique in terms of national coverage and multi-banner operations, the scale that once secured its dominance is now put to the test.

In FY2024, Macy’s Inc. spanned 680 stores, including Macy’s, Macy’s Backstage off-price outlets, Market by Macy’s small-format stores, but also Bloomingdale’s, Bloomingdale’s The Outlet, Bloomie’s (Bloomingdale’s small-format stores), its international stores in Dubai (UAE) and Kuwait under license, and beauty specialist Bluemercury. FY2024 closed with net sales of $22.293 billion (down 3.5% YoY). The company reported a 38.4% gross margin (flat YoY). Digital sales accounted for 33% of net sales (unchanged from 2022), indicating a stabilised omnichannel mix after pandemic-era gains.

Despite a glorious past, today’s Macy’s financial picture seems gloomy for a department store as tightly intertwined in the country’s commercial and cultural landscape as it is. Macy’s mirrors the evolution of retail itself in the 20th century: a story of pioneering and relentless innovation. The fight for relevance is the question it needs to address to fully belong in the 21st century.

The making of an American star

From 14th Street to Herald Square

In 1843, Rowland Hussey Macy opened several dry goods stores in Massachusetts. All failed. Learning from its mistakes, he opened R.H. Macy & Company on NYC’s 14th Street and Sixth Avenue in 1858. He adorned it with a star, which has remained Macy’s logo to this day. Innovative from its inception, the store changed the retail industry. It was the first to institute the one-price system, advertise its prices in newspapers, and promote a woman to an executive position. Margaret Getchell started as a cashier and rose to become a leader in the company. She developed many ideas, including using illuminated window displays to attract customers. Macy’s also pioneered the use of an in-store Santa Claus as early as 1861, embedding retail into cultural rituals.

Macy died in 1877. The company remained in the family until it was acquired in 1895 by Isidor and Nathan Straus, who had previously held a license to sell china at Macy’s. The decisive step came in 1902, when the store relocated to Herald Square. Initially a single building, the store expanded through new construction, eventually occupying almost the entire block bounded by Seventh Avenue, Broadway, 34th Street and 35th Street, creating what was then the world’s largest store. The store seemed so far away from its original ground that the company had to offer a steam wagonette service to transport customers from 14th Street to 34th Street. Macy’s became a publicly listed company in 1922. Two years later, Macy’s inaugurated the Thanksgiving Day Parade, which soon became a cultural event and a form of brand equity independent of its stores.

Macy’s goes national: growth and the making of a middle-class brand

The company opened their second location in the Bronx in 1941. The interwar period was marked by expansion beyond Manhattan, acquiring local department store chains across the country, including Lasalle & Koch (Toledo), Davison-Paxon-Stokes (Atlanta) and L. Bamberger & Co. (Newark). Post-World War II, acquisitions resumed with O’Connor Moffat & Company (San Francisco) and John Taylor Dry Goods Co. (Kansas City).

Then, Macy’s opened mall branches in Miami’s suburbs, Houston, New Orleans, Dallas, Atlanta, the Midwest, New Jersey, Philadelphia and Baltimore. From 1976 onwards, Macy’s cultural pull also included the 4th of July Fireworks over NYC’s East River and Hudson River.

Macy’s became an authority in bringing accessible style to the growing middle-class consumers, positioning itself between discount chains and luxury stores. It was neither elitist nor mass-market, but rather a “mass premium” brand long before the term existed. Soon enough, the flagship store functioned as both a commercial hub and a symbolic space for aspirational middle-class consumption.

From bankruptcy to a coast-to-coast powerhouse

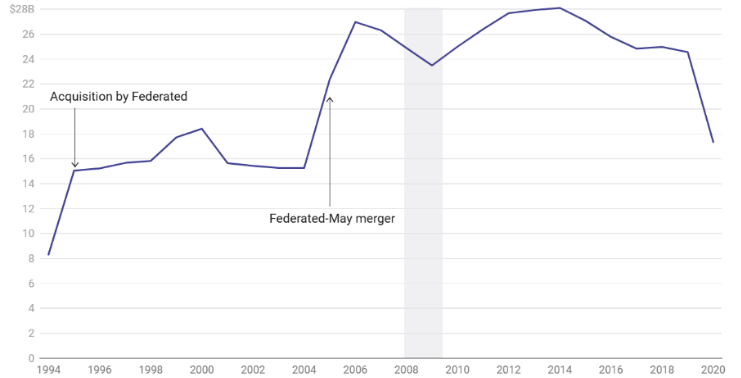

By the 1970s and 1980s, Macy’s continued acquiring regional department stores. However, aggressive expansion financed by debt led to instability, a pattern Saks Global is currently experiencing. In 1992, Macy’s filed for Chapter 11 bankruptcy, underscoring the fragility of even the most iconic retail institutions and challenging the ‘too big to fail’ economic assumption. The company emerged from bankruptcy in 1994, merging with Federated Department Stores, the owner of Bloomingdale’s, among other banners. This merger created the largest department store group in the U.S., providing Macy’s with capital, management expertise, and scale. In 1995, the group operated 355 department stores across 35 states, achieving $8.29 billion in sales.

Federated Department Stores’ strategy culminated in the $11 billion acquisition of May Department Stores in 2005 and the conversion of approximately 400 stores to the Macy’s nameplate in 2006. Indeed, Federated rebranded most of its regional banners, such as Marshall Field’s, under the Macy’s name. This controversial move erased long-standing local identities in favour of the Macy’s brand, totalling 853 stores, creating a truly coast-to-coast flag and a universal name recognition. The consolidation positioned the department store as the anchor in hundreds of malls nationwide. In practical terms, that nationalisation gave the company a distribution canvas that neither luxury-led peers nor remaining mid-market rivals match to this day.

Federated Department Stores re-named itself Macy’s, Inc. in 2007. Standing out among other U.S. department stores, Macy’s diversified its portfolio across price tiers and categories, including Bloomingdale’s in the upscale fashion segment and the 2015 acquisition of beauty retailer Bluemercury.

Reinventing the store: Macy’s between culture, localisation, and experience

When a store becomes a stage: Macy’s as a cultural institution

Macy’s emerged as a reference in American and global retail by pairing scale with cultural brand-building. The company treated the department store as a public theatre and then institutionalised spectacle through the Macy’s Thanksgiving Day Parade. The first Disney Mickey Mouse balloon entered the parade in 1934, paving the way for subsequent cultural collaborations with Sonic the Hedgehog, Barney the Dinosaur, Snoopy, the Pink Panther, and brands like M&M’s. The parade became known nationwide after WWII, as it was heavily featured in the 1947 film Miracle on 34th Street, which included footage of the 1946 festivities.

Also, Macy’s began the annual Independence Day show with the U.S. Bicentennial in 1976, the start of the modern Macy’s 4th of July Fireworks tradition. That event, broadcast nationally on WPIX and later by NBC (which also broadcasts the Macy’s Thanksgiving Day Parade), solidified the company as a household name and transformed a retail banner into an annual cultural tradition, reinforcing Macy’s “owned media” advantage at a national scale. This blend of retail and ritual helps differentiate Macy’s from peers whose brands are influential in their cities but may lack a countrywide cultural amplifier.

My Macy’s: central power, local touch

My Macy’s strategy was launched in 2008 under the leadership of CEO Terry Lundgren as a much-needed localisation programme, aiming to bring a more personalised flair to stores by moving day-to-day assortment and presentation decisions closer to the store. Macy’s expanded it nationwide in 2009 with a new structure of regional merchants and planners who tailored buys, sizes and presentations to local tastes, creating 1,200 new roles. Parallel to that, Macy’s consolidated regional divisions into a single national organisation for core functions (buying, marketing, finance, and HR) to reduce duplication, increase efficiency, and streamline decision-making.

The operating model consisted of 69 districts that could adjust roughly 10-15% of a store’s inventory mix to local demand, with national categories and seasonal statements still determined by central buying. Also, to make My Macy’s work, they automated customer tracking and segmentation, allowing for a clearer view of the consumer. Early results were positive as most of the top-performing markets in 2009 were My Macy’s districts.

By late 2011, Macy’s introduced “My Macy’s 2.0”, additional targeted, cross-functional initiatives designed to sharpen local relevance and tie it more tightly to the company’s emerging omnichannel model. Macy’s pushed more decision-making to district teams to fine-tune “by store,” not just by region. My Macy’s 2.0 was deployed alongside a ship-from-store/BOPIS scale-up strategy, with localised inventory serving digital orders nationwide. Tablets, tap-to-pay pilots and QR codes were rolled out to improve discovery and conversion. Finally, the “MAGIC Selling” training (Meet-Ask-Give-Inspire-Celebrate) was expanded to raise conversion and NPS.

My Macy’s improved sell-through and relevance while protecting scale. However, it fell short due to uneven, complex execution. Building and maintaining district-level merchant teams added organisational complexity, with outcomes varying by market and leadership depth. Localisation was necessary but insufficient to deliver the digital growth achieved by other platforms. Macy’s digital mix eventually stabilised around one-third of sales in the 2020s, requiring additional strategies beyond localisation.

That said, as a case of “localisation at scale,” My Macy’s was a smart hybrid of central scale and local empowerment. Its limits became apparent later: it could raise relevance, but it couldn’t fully overcome macro headwinds (mall traffic erosion, off-price, and online pressure) without broader reinvention in experience, merchandising authority, and digital. In Macy’s transformation arc, My Macy’s appears as the operational foundation that allowed subsequent strategies such as off-mall small formats, marketplace and fleet upgrades.

Moreover, My Macy’s illustrates a typical pattern: companies pursue centralisation and scale, then decentralisation in the name of localisation and personalisation, as neither strategy is 100% satisfactory. For example, Walmart, a champion of centralisation and standardisation, emphasised local tailoring via “Store of the Community” in 2001 with assortments adapted to local demographics, moving from a one-size-fits-all playbook toward more local customisation.

Turning stores into stories

In 2018, as retail was becoming less transactional, Macy’s invested in experiences to capture younger consumers, establishing a pop-up enterprise, dubbed The Market @ Macy’s, designed to emphasise in-store discovery of emerging brands and niche products. The ten pop-up stores were designed to offer customers a rotating selection of apparel, accessories, beauty, entertainment, experiences, decoration, stationery, technology, and gifts. The retail-as-a-service concept was described as a solution for brands looking to break into brick-and-mortar retail. Unlike traditional concessions, Macy’s staff ran the pop-ups. Offering more flexible lease terms, brands were paying a fixed fee but pocketing all sales. Ultimately, Macy’s evaluated sales and traffic. The duration was flexible, although a one-month minimum commitment was required.

Later in 2018, Macy’s acquired Story, a quirky New York City retail store that has partnered with big and small retailers and brands. Story defined itself as a storytelling retail model, adopting a magazine’s perspective, evolving like a gallery, and selling items like a store. Macy’s even hired Story founder Rachel Shechtman as brand experience officer. Finally, that same year, Macy’s partnered with b8ta, a company providing the technology engine to enhance and scale The Market @ Macy’s. With b8ta’s software platform and business model, product makers could go from solely selling online to launching their products with Macy’s in a few clicks. However, execution was uneven, and Macy’s struggled to balance its vast legacy footprint with the agility needed for such formats. When COVID hit and Macy’s closed stores in March 2020, the pop-up programme was effectively discontinued and did not return thereafter.

In transition: the state of Macy’s today

Why Macy’s lost its shine

In 2015, roughly 10 years after its massive expansion that led to a network of 853 stores, Macy’s told investors it would close 35 to 40 underperforming stores in 2016. In the meantime, analysts expressed confidence that Amazon would overtake Macy’s in apparel sales (even though Macy’s entered e-commerce early). In the years that followed, as Amazon grew its fashion business, Macy’s turnover decreased.

However, Amazon is not solely responsible for Macy’s downfall. The mid-century department store mall era’s promise to combine the best of the fashion world with the best of the discount world hardly works in the 21st century. As a mid-tier banner, Macy’s business was eroded by low-price retailers (as early as 1962 with the start of mass-market retailers such as Target) and discounters serving a shrinking middle class. By comparison, in 2006, Macy’s operated 853 department stores and a website, reaching $27 billion in sales, while Target operated nearly 1,500 stores and a website, notching $59.5 billion in sales.

In parallel, the department stores’ love story with malls came to an end. Macy’s, as a suburban mall anchor nationwide, didn’t react quickly enough as suburbanites grew pessimistic and anxious about the future, increasingly buying cheaper products at off-price stores outside traditional malls. Malls and their department store anchors were stuck together, but were no longer hangout locations for kids and teens. Meanwhile, speciality retailers such as Sephora in beauty or Best Buy in electronics took market share from department stores. In turn, unable to compete with these speciality retailers, Macy’s (and others) closed or reduced store sections, filling them only with apparel (in free fall anyway) and making the stores less and less relevant and attractive. Finally, as the U.S. middle class shrinks, the mid-price market is disappearing, leading Macy’s to compete with off-price retailers.

From Polaris to A Bold New Chapter: Macy’s strategic reset

Learning from the My Macy’s and Market @ Macy’s initiatives, the company launched the three-year turnaround Polaris strategy, announced in February 2020 by CEO Jeff Gennette. Meant to stabilise profitability and position the company for growth, it was primarily built around:

- Optimising the fleet by closing roughly 125 lower-tier-mall stores while giving “growth treatment” to 100 stores and testing off-mall small formats, Market by Macy’s.

- Accelerating digital/omnichannel (ship-from-store, BOPIS, marketplace).

- Simplifying the organisation with a net 9% reduction in its corporate function headcount (approximately 2,000 positions) and one corporate HQ.

In practice, parts of Polaris worked. Macy’s built a balanced omnichannel mix, resulting in digital stabilising at ~33% of net sales by FY2024, while the marketplace expanded. However, some elements of the strategy stalled: the original 125-store closure cadence was disrupted by the pandemic and later re-scoped. Several pre-Polaris experiments (The Market @ Macy’s and the Story shop-in-shop) were wound down and not scaled post-2020.

Announced four years after the Polaris strategy, A Bold New Chapter plan, led by new CEO Tony Spring, builds on and accelerates Macy’s Polaris portfolio reset. The plan includes closing ~150 underproductive Macy’s locations by 2026 and investing in ~350 “go-forward” stores via remodels, service and presentation upgrades, while scaling small-format/off-mall concepts. In January 2025, Macy’s confirmed the first 66 closures as an initial wave, consistent with the multi-year target. Also part of A Bold New Chapter, Macy’s created the “First 50” cohort, the first wave of upgraded stores. 2024 third-quarter results highlighted that these locations delivered their third consecutive quarter of comparable sales growth, up 1.9%. However, Macy’s First 50 locations, Bloomingdale’s and Bluemercury’s posted growth is more or less offset by softness in non-first-50 Macy’s doors. In the coming semesters, the plan’s credibility will rely on the pace of closures and the performance of upgraded doors. Overall, the plan acknowledges and builds on Macy’s reality: its strongest stores still outperform, but the weakest ones drag down the brand.

Macy’s next moves

So far, structural headwinds have outpaced wins. As a result, Macy’s has many challenges ahead to secure its future as a mid-tier department store:

- Rebuild its fashion authority despite the sector squeeze. With the U.S. mid-market pressured by off-price, fast fashion, and platforms, Macy’s needs clearer category leadership (especially in women’s categories, its most prominent family) and a sharper brand image, less reliance on promotions, and more on curation and experience so that the remaining fleet feels “worth the trip.” This is still a question mark, as previous attempts have failed.

- Grow e-commerce beyond 33% of the business without eroding contribution margins.

- Finish the store fleet reset at pace and with proof, as the strategy only delivers if the upgraded doors consistently outperform the fleet.

- While Macy’s credit card is an additional revenue stream, it fell to $537m in FY2024 as card income is sensitive to credit cycles.

- In 2019, “retail prophet” Doug Stephens defined the company’s struggle: “Macy’s has two things, space and audience, and they’re not leveraging that space and that audience to find new ways of making money beyond selling apparel and linens, ways to monetise experiences within that space that are richer for the consumer.” It’s not entirely true anymore, as Macy’s has built Macy’s Media Network to monetise Macy’s audience and data through brand advertising on owned and partner surfaces. This additional source of revenue generated $176 million in FY2024 (+13.5% YoY).

- Accelerate Bloomingdale’s and Bluemercury growth, the best way to de-risk Macy’s overexposure to the mid-tier.

- Keep control of the real-estate narrative. Macy’s must show that its own plan has more value than aggressive sale-leasebacks would, as suggested by activist investor pressure from Arkhouse Management and Brigade Capital, which launched an unsolicited acquisition bid in 2023 to take the company private. They would have used every means to extract cash from stores while keeping them open under leases. They likely would have done a portfolio-by-portfolio review, selling some stores and leasing them back, placing secured debt on flagship or high-quality sites and pursuing mixed-use redevelopments on under-utilised parcels. Macy’s board ended talks in July 2024, saying the proposal lacked value and financing certainty.

Macy’s today is a scaled mass-premium platform with owned media assets, a coast-to-coast store network and diversified banners that many U.S. peers cannot replicate. The fleet reset, store closures and investments are designed to concentrate capital and talent where the unit economics justify it. The primary risks remain the mid-tier squeeze from off-price, fast fashion and e-commerce platforms, and the credit income risk. Conversely, the 33% digital mix, the traction at First 50 locations and the ongoing strength at Bloomingdale’s and Bluemercury point to levers Macy’s can scale as the transformation progresses.

Macy’s future relies on turning a smaller, better fleet and a balanced profit mix, with merchandise from its various banners, credit and retail media revenue, into sustained growth and margin, while advancing the digital business to make the company less exposed to the structural headwinds of the legacy mall model. The company itself sets the targets: the next 6-18 months are about proving them in the numbers. A question remains: what to do with Macy’s most significant symbol —the Herald Square flagship store, which increasingly seems irrelevant at the light of today’s consumer habits.

Credits: IADS (Christine Montard)

Related posts

IADS Exclusive - How department stores are playing the 2026 FIFA World Cup

IADS Exclusive - How department stores are playing the 2026 FIFA World Cup

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Agentic AI turns every team into its own transformation engine

Agentic AI turns every team into its own transformation engine

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript